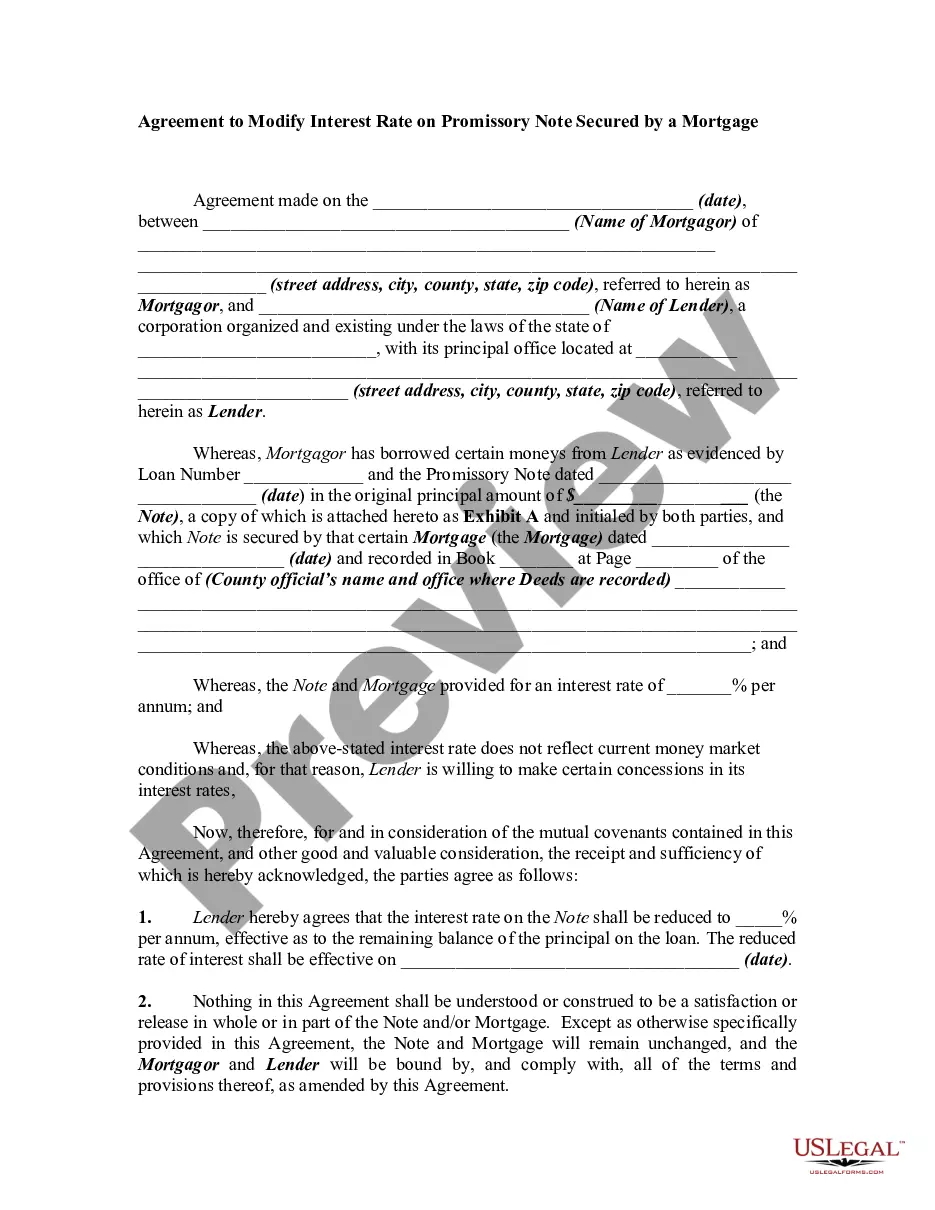

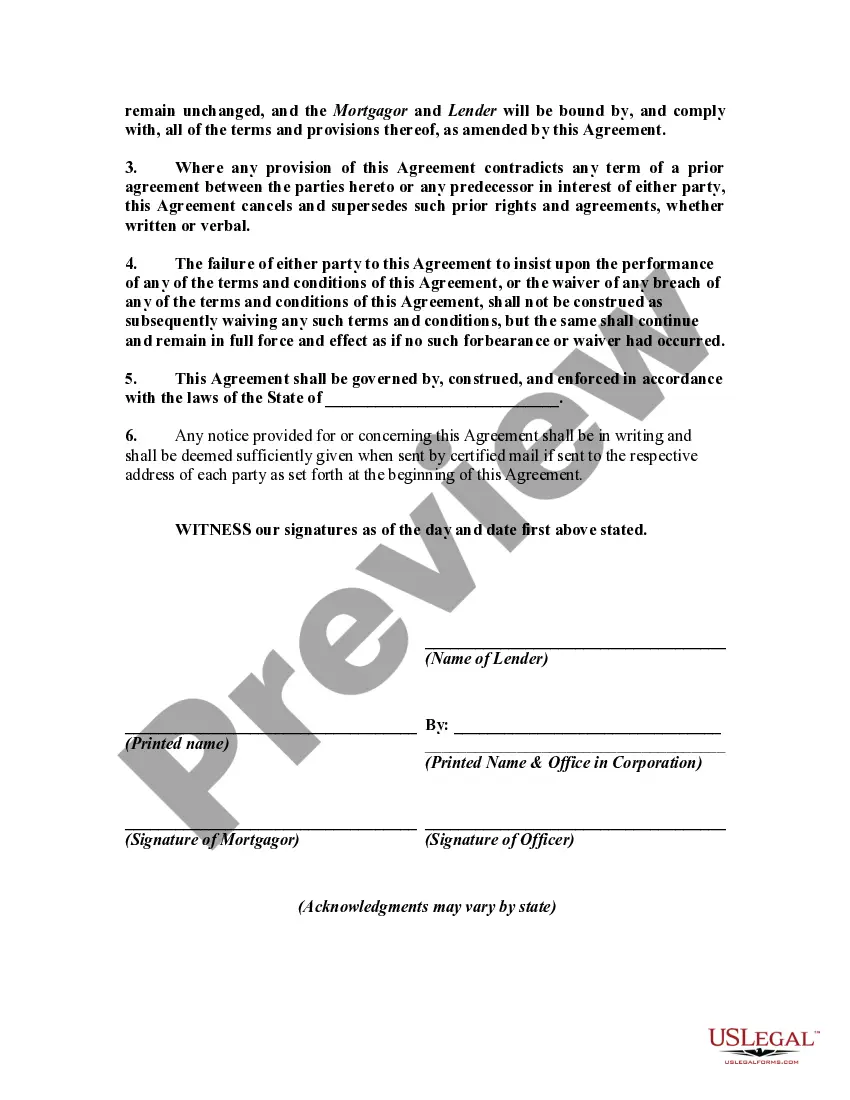

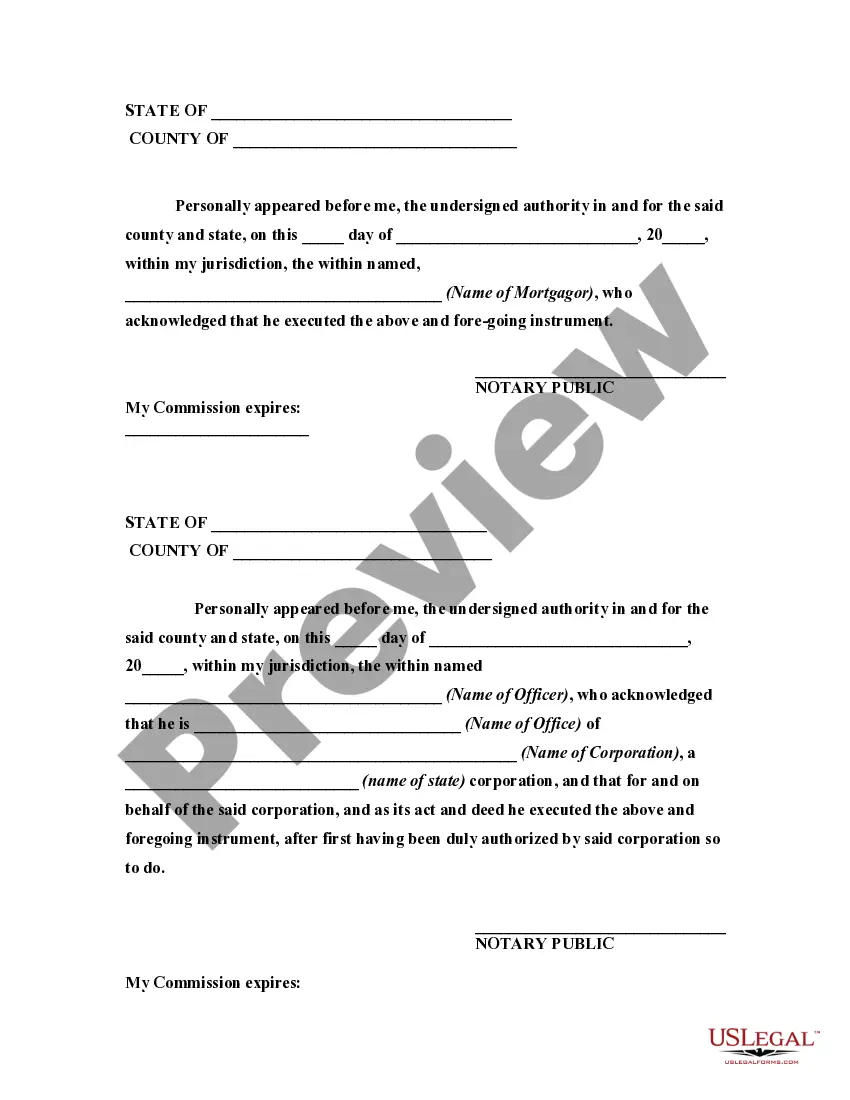

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A promissory note for an exam is a legally binding document that outlines a borrower's promise to repay a specific amount of money borrowed to the lender. It serves as a written agreement highlighting the terms and conditions of the loan, including the repayment schedule, interest rate, and any other relevant provisions. The promissory note for an exam is primarily used in educational institutions, where students may require financial assistance to cover their tuition fees, textbooks, or other educational expenses. It is usually considered an unsecured loan, as it doesn't require collateral from the borrower. Different types of promissory notes for exams include: 1. Student Promissory Note: This is the most common type, used by students to finance their education. It outlines the loan amount, interest rate, repayment terms, and other conditions agreed upon between the student borrower and the educational institution or lender. 2. Private Promissory Note: These are promissory notes issued by private lenders, such as banks or financial institutions, to students who may not qualify for government-backed student loans. Private promissory notes often have different interest rates and repayment terms, depending on the lender's policies. 3. Federal Promissory Note: These promissory notes are used when students secure federal loans, such as Stafford loans or Perkins loans. The terms and conditions of federal promissory notes are governed by federal regulations, and they usually offer more flexible repayment options and lower interest rates compared to private loans. 4. Parent PLUS Promissory Note: This type of promissory note is used when parents take out loans to finance their child's education. Parent PLUS loans are federal loans, and the promissory note outlines the obligations and responsibilities of the parent borrower. 5. Consolidation Promissory Note: This note is used when a student or parent borrower decides to consolidate multiple educational loans into one. The consolidation promissory note combines the outstanding balances and terms of the original loans into a single loan, simplifying the repayment process. When preparing for an exam, it is essential to understand the implications of signing a promissory note. As it is a legally binding agreement, borrowers should carefully review the terms before signing to ensure they comprehend their responsibilities and the consequences of defaulting on the loan. Consulting with a financial advisor or loan counselor can provide further assistance in comprehending the terms and making informed decisions.