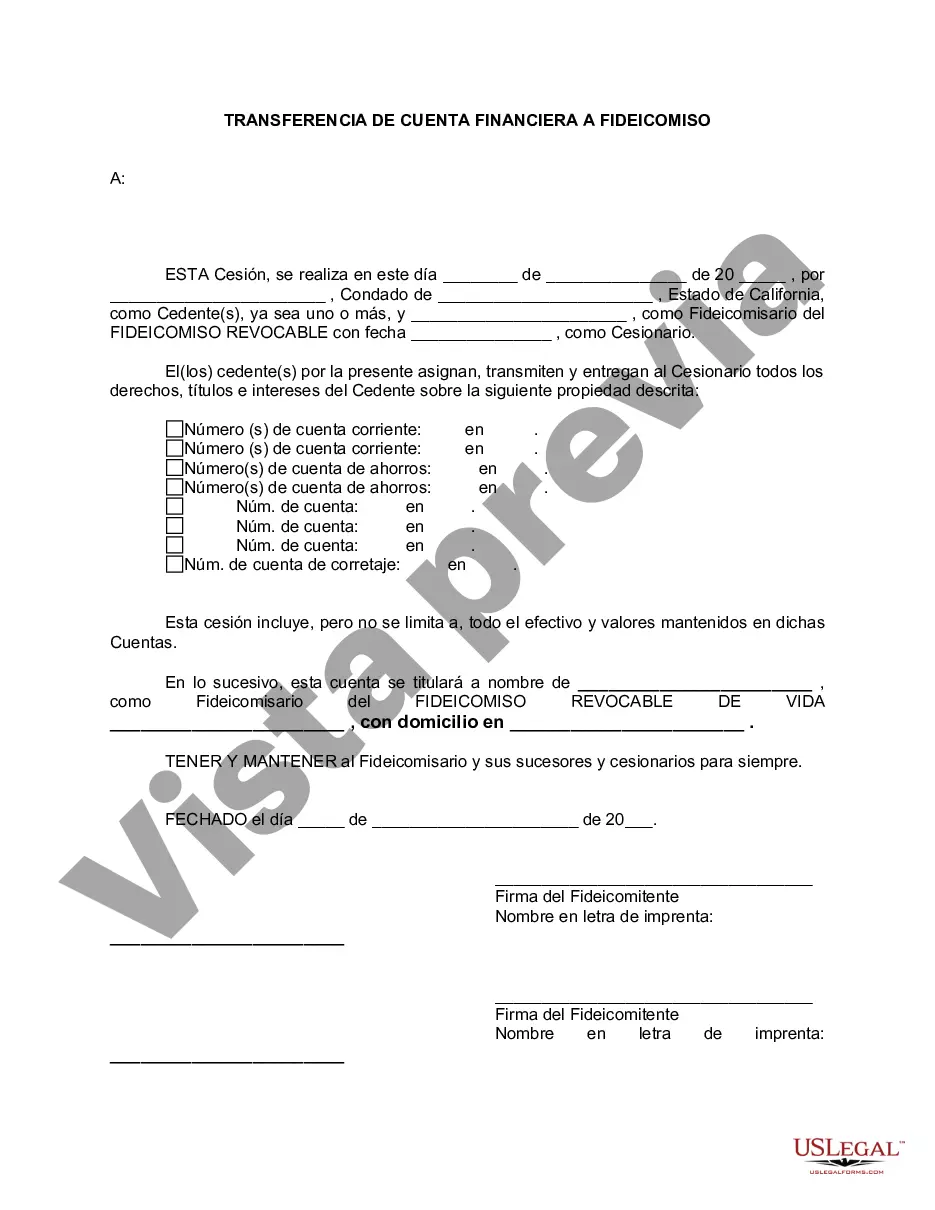

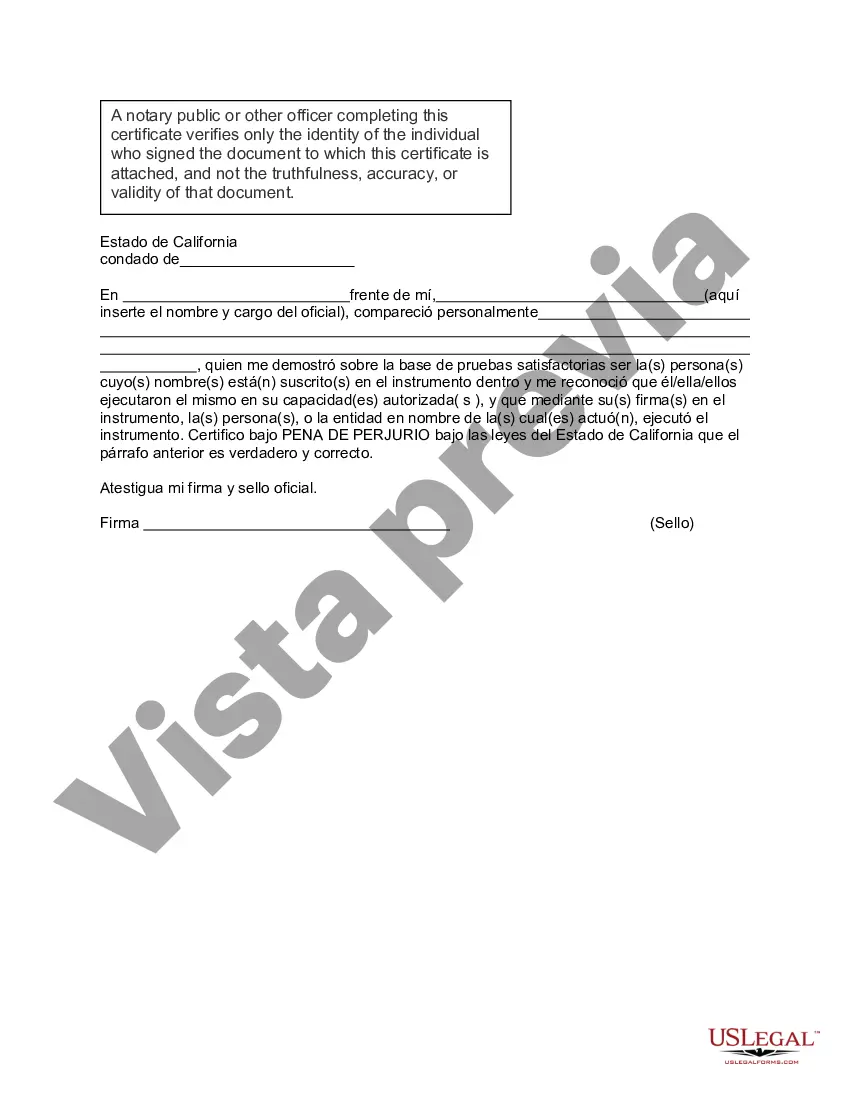

Trust Account With - California Financial Account Transfer to Living Trust

Description

Form popularity

FAQ

One downside of a family trust involves the complexity and ongoing management required. Beneficiaries might misunderstand the trust's purpose, leading to resentment or conflict. Therefore, it is crucial to clearly communicate the trust's intentions and consult with professionals who can help you create an effective trust account with clarity and purpose.

Setting up a trust can come with pitfalls if not done carefully. Misunderstanding the legal requirements can lead to improper funding or tax issues. It’s essential to work with legal experts who can guide you in establishing a compliant trust account with the right provisions to protect your interests.

While trust funds serve useful purposes, there are drawbacks to consider. The costs of setting up and maintaining a trust account with associated fees can add up over time. Additionally, some people may misuse or mishandle trust funds, leading to family disputes or unintentional financial burdens.

Having your parents place their assets in a trust can offer significant advantages, such as avoiding probate and ensuring a smooth transition of wealth. This strategy can protect assets from creditors and help manage tax implications. Ultimately, discussing their specific financial situations with a legal professional will clarify whether establishing a trust account with their assets is the right choice.

One of the biggest mistakes parents make when setting up a trust fund is not clearly defining their goals and terms. A lack of clarity can lead to confusion and potential disputes in the future. It’s important to have a well-organized trust account with specific guidelines to ensure your intentions are met.

Yes, a trust often needs to be filed with the IRS, especially if it has any taxable income. The filing process typically involves Form 1041, which details the income, deductions, and other pertinent information. Managing your trust account with this filing ensures compliance with federal laws.

Failing to file taxes on a trust can lead to significant penalties and interest charges. The IRS may impose fines for late or unfiled returns, which can accumulate over time. Proper management of a trust account with timely filings is essential to avoid these consequences.

To file a trust tax return, there isn’t a specific minimum income amount; rather, it depends on the type of trust and its income. Generally, if the trust account with income is over $600, you will likely need to file a return. Understanding the financial situation of the trust is critical in meeting IRS requirements.

The new IRS rule on trusts centers around transparency and tax compliance. Specifically, the IRS now requires certain trusts to share more information to avoid tax evasion. If you maintain a trust account with significant assets or income, staying informed about these updates is crucial.

Yes, you need to report a trust to the IRS if it meets certain criteria. Generally, a trust account with income may require you to file Form 1041, the U.S. Income Tax Return for Estates and Trusts. This filing helps ensure that the IRS is aware of the trust's financial activities and complies with tax regulations.