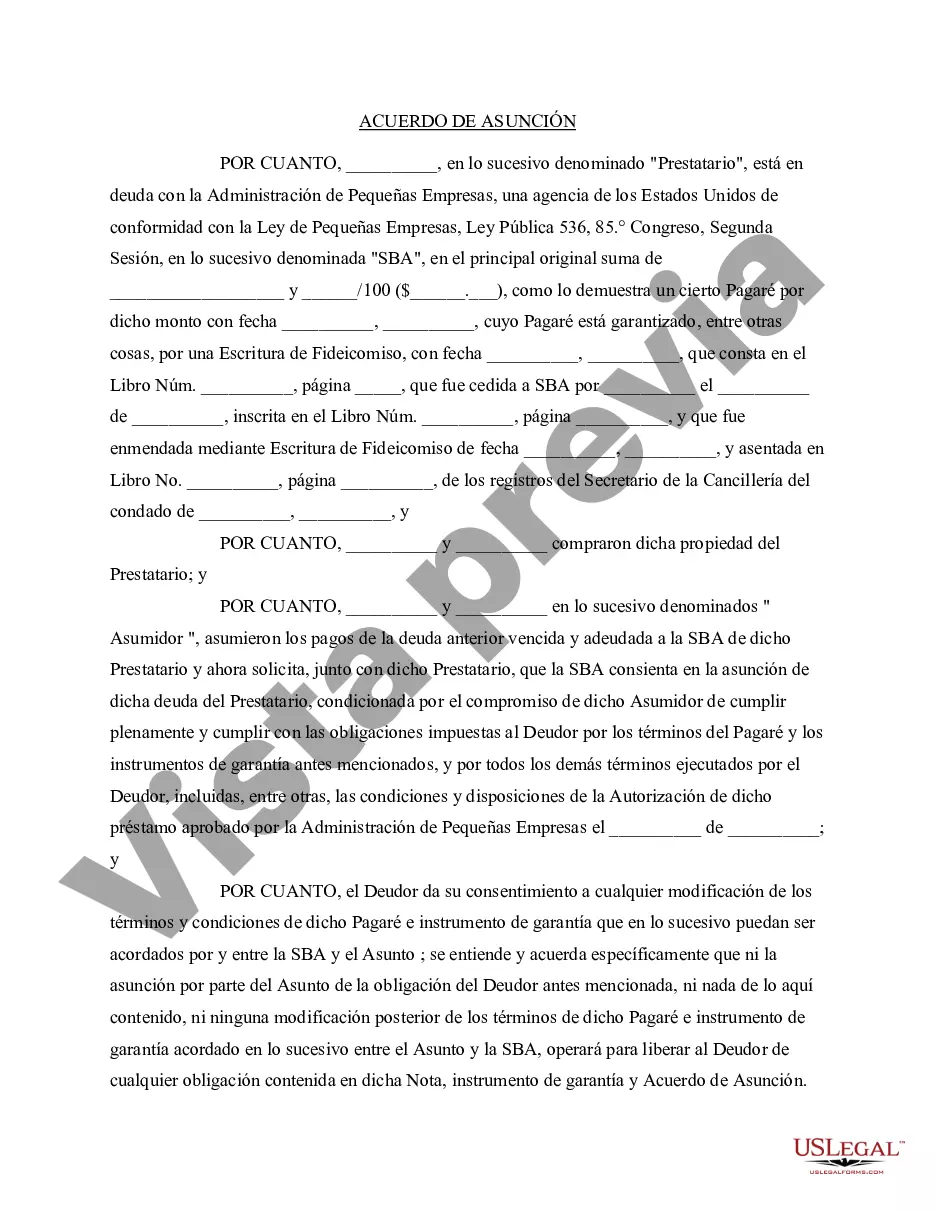

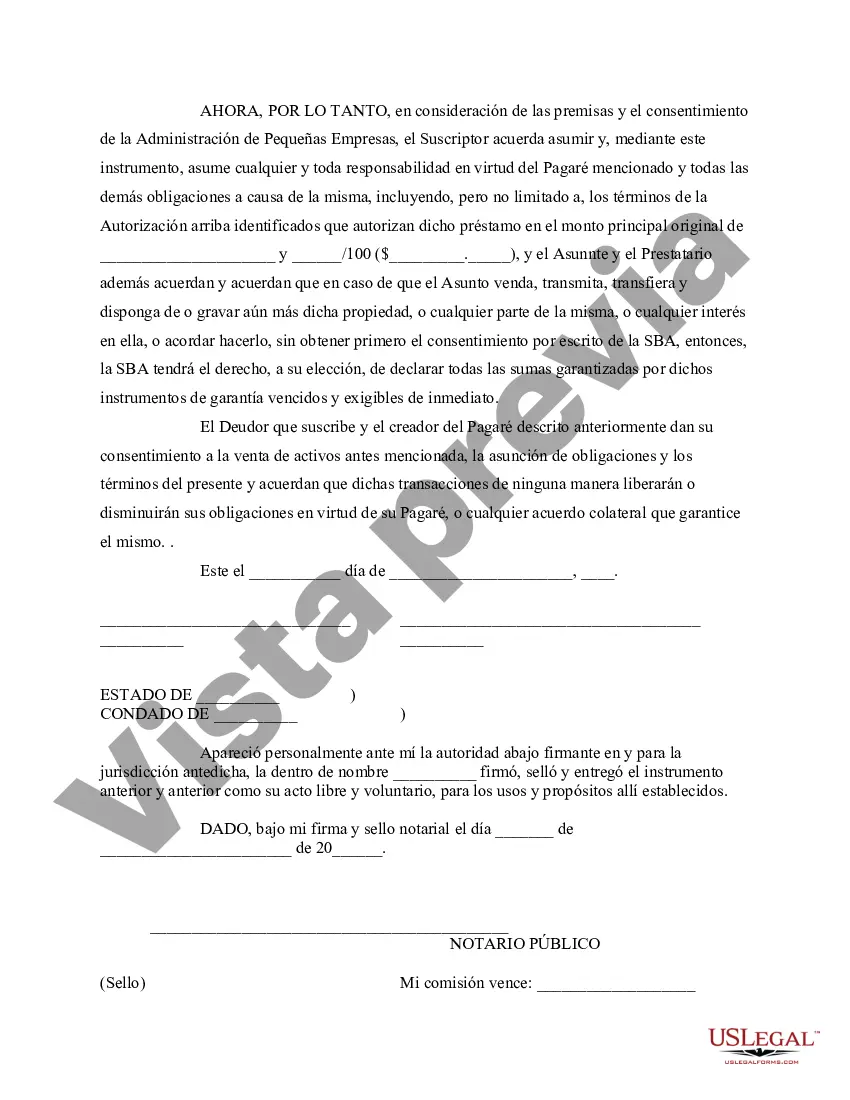

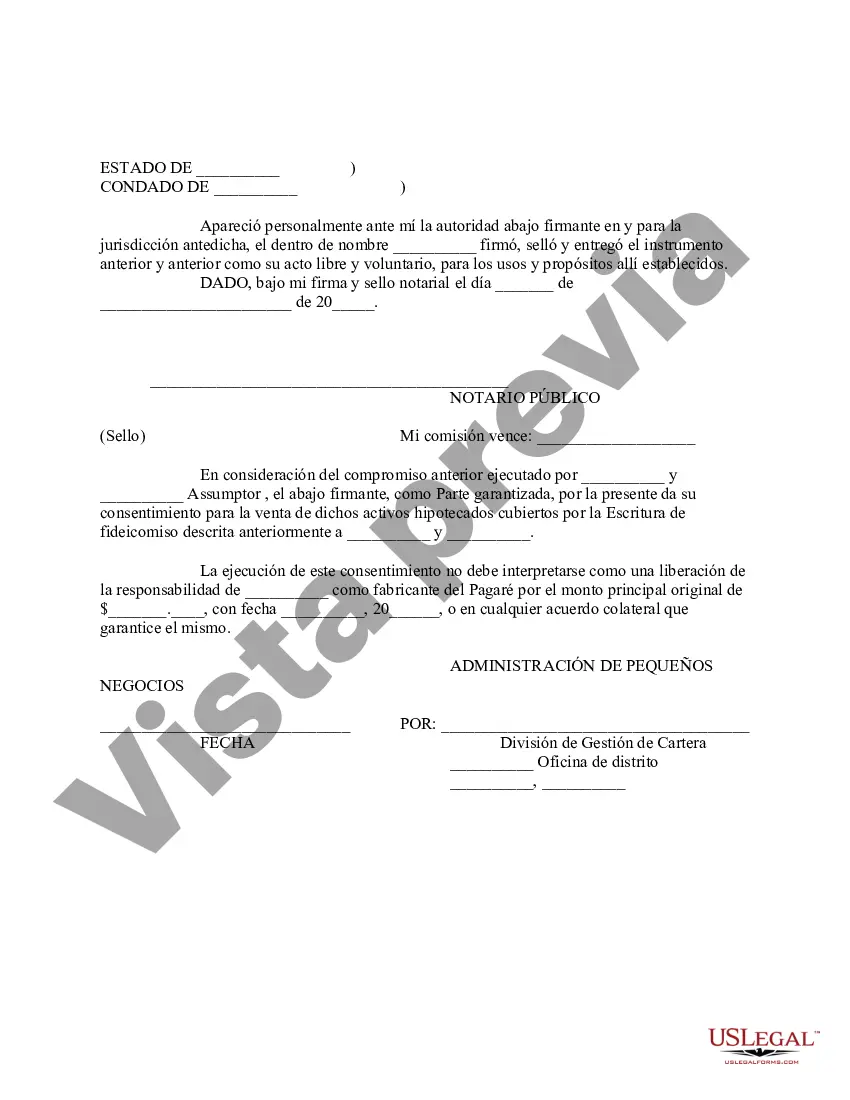

Sba Loan Assumption With A Mortgage In Maryland - Assumption Agreement of SBA Loan

Description

Form popularity

FAQ

The Drawbacks of Mortgage Assumption In a simple assumption, the seller remains liable for the outstanding mortgage debt. If the buyer defaults on payments, both parties' credit scores are affected. This shared risk can strain the relationship between buyer and seller and lead to financial repercussions for both.

The mortgage balance, interest rate, and repayment schedule all carry over to the buyer. However, only Federal Housing Administration (FHA) loans, U.S. Department of Agriculture (USDA) loans, and U.S. Department of Veterans Affairs (VA) loans can qualify. Conventional mortgages cannot be assumed.

How to request an SBA subordination Application for lien subordination. Letter stating reason for lien subordination with a list of collateral to be subordinated. Copy of the fully executed Factoring Agreement. Copy of your SBA Agreement. Copy of the SBA's lien search. Proof of Hazard Insurance.

You are legally obligated to make the monthly payments required by your mortgage (deed of trust) and promissory note. If you sell your home by letting a purchaser assume your mortgage, you are still liable for the mortgage debt unless you obtain a release from liability from your mortgagee.