1031 Exchange Agreement Form For Uk In Los Angeles - Exchange Agreement for Real Estate

Description

Form popularity

FAQ

Section 1031 is part of federal law, so it applies to federal taxes, which are the same no matter what state you're in. You can perform a 1031 exchange between business or investment properties located anywhere in the United States, so long as they meet all other 1031 requirements.

While foreign property is not of a like kind with domestic property, foreign properties are considered like-kind with one another. You can perform a 1031 exchange with foreign properties, so long as your relinquished and replacement properties are both located outside the United States.

In California, taxpayers can use 1031 exchanges to defer capital gains taxes on the sale of a variety of investment properties including multifamily homes, single-family homes, and commercial real estate.

Section 1031 is part of federal law, so it applies to federal taxes, which are the same no matter what state you're in. You can perform a 1031 exchange between business or investment properties located anywhere in the United States, so long as they meet all other 1031 requirements.

Here are examples of properties ineligible for a 1031 exchange: Primary residences: A 1031 exchange is specifically intended for investment or business properties. Personal properties are not eligible. Vacation homes: Vacation homes generally do not qualify if used for personal reasons.

You can perform a 1031 exchange with foreign properties, so long as your relinquished and replacement properties are both located outside the United States.

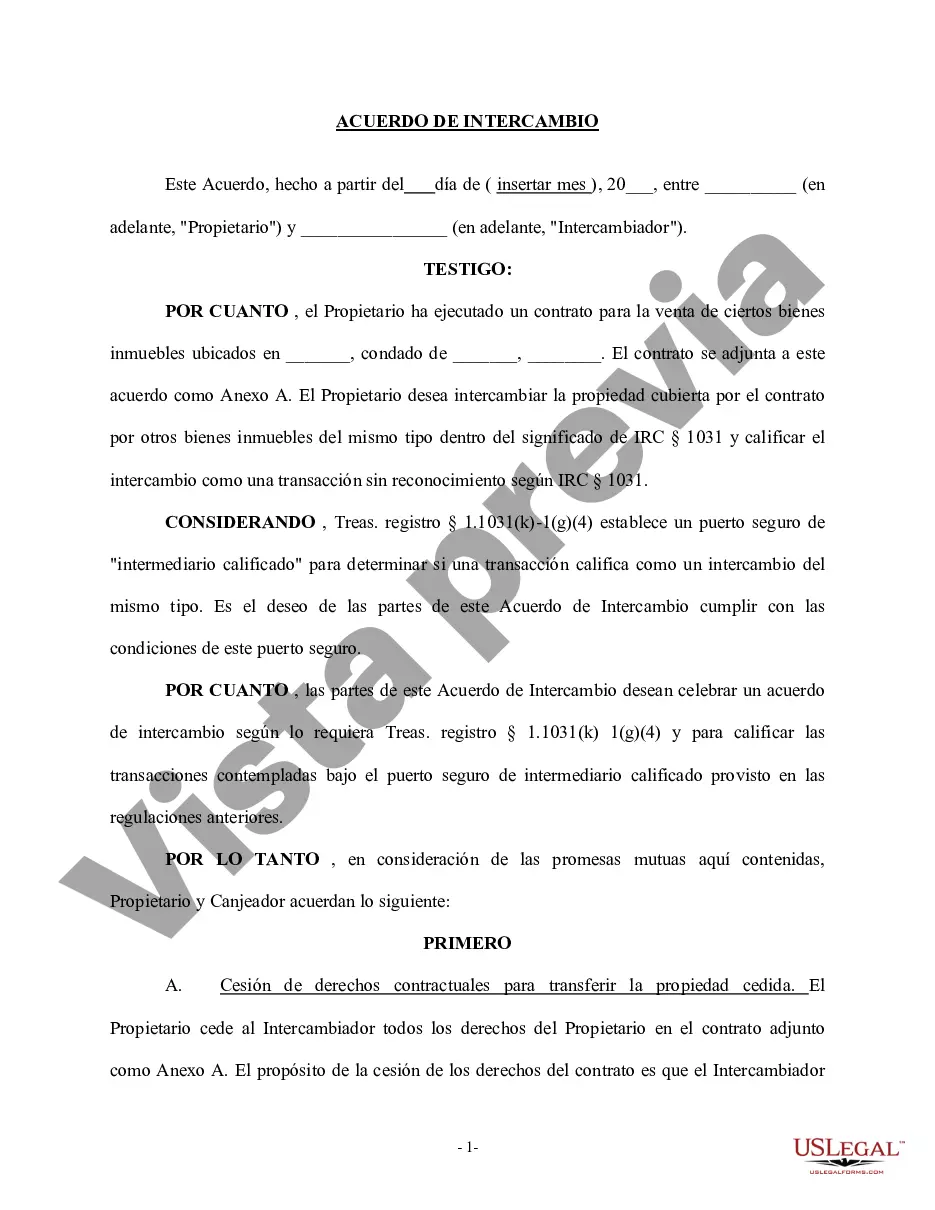

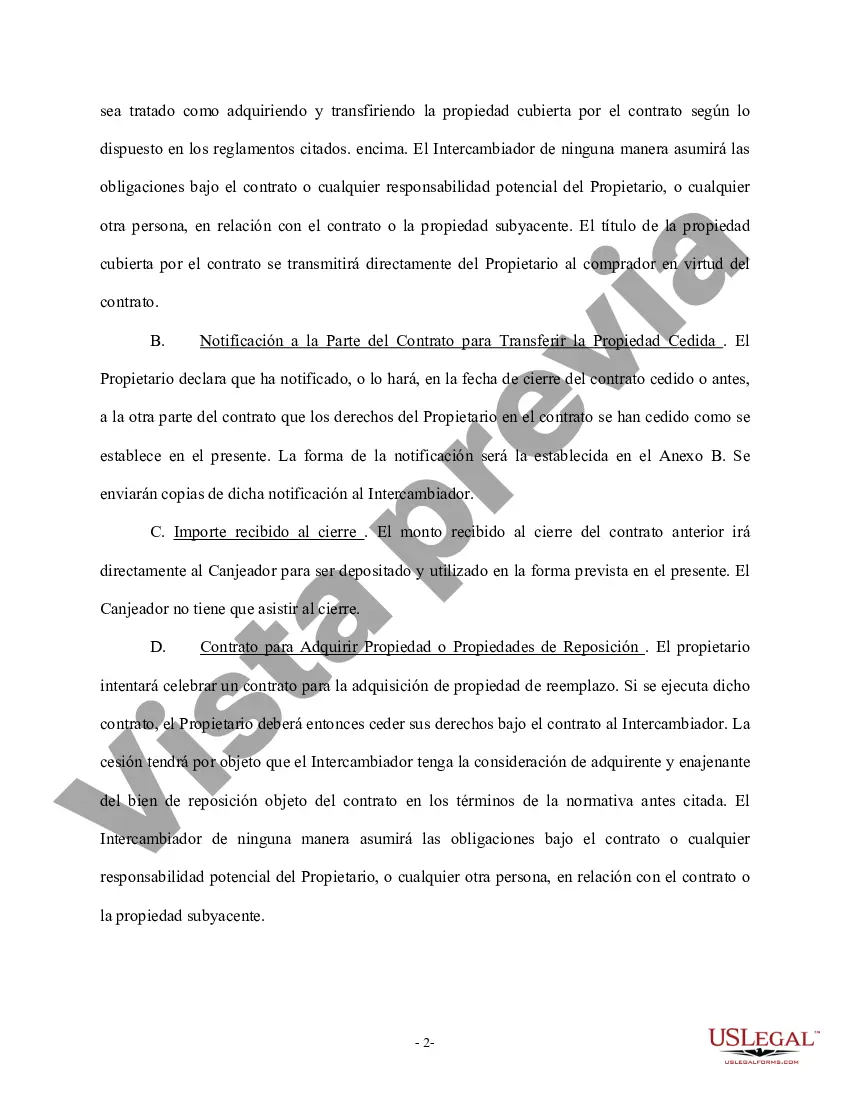

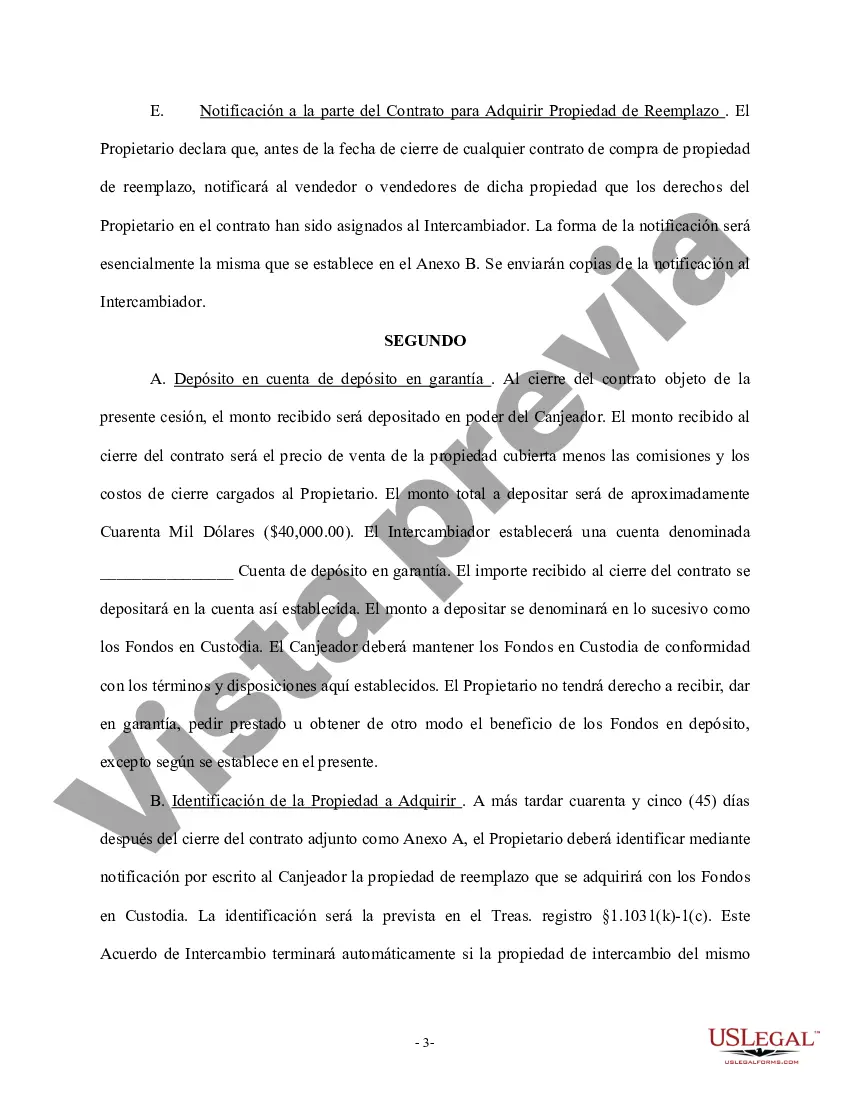

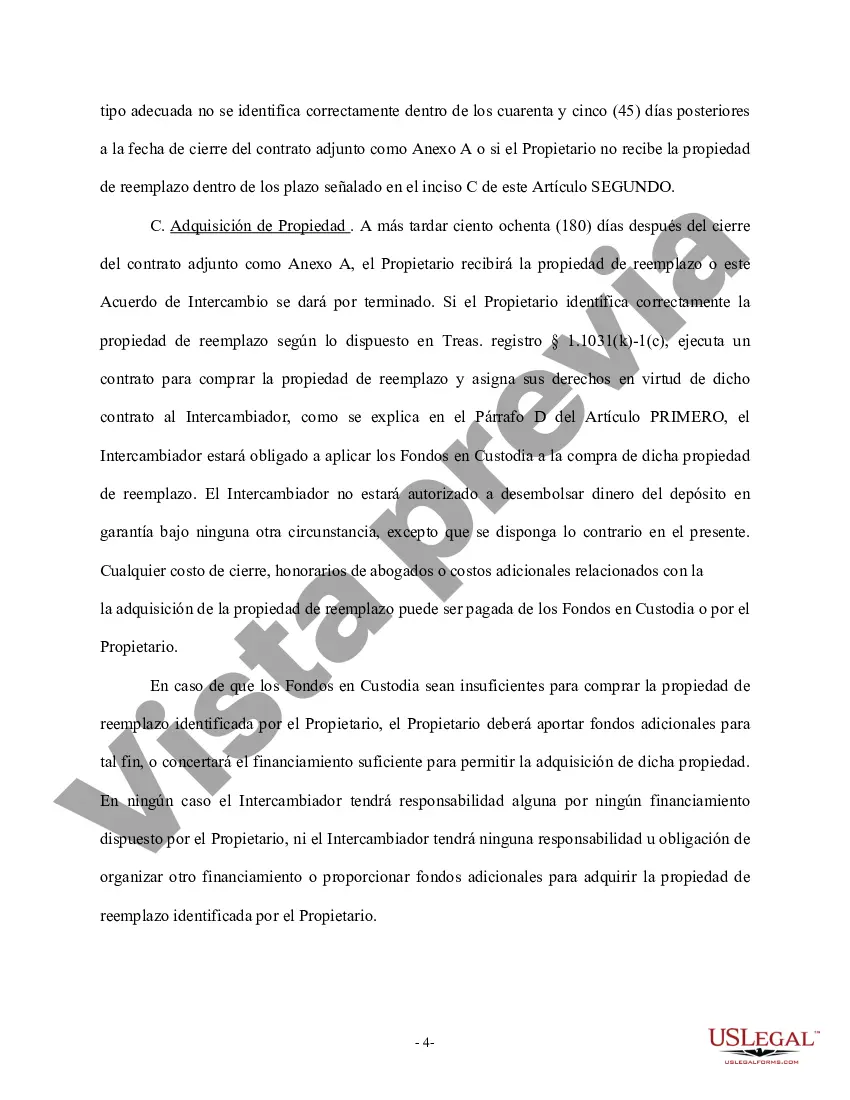

A Practice Note discussing Section 1031 like-kind exchanges of real estate, which is an important tax planning tool that allows real property owners to defer gains on the sale of real estate by investing the proceeds into replacement property.

You can perform a 1031 exchange with foreign properties, so long as your relinquished and replacement properties are both located outside the United States.

These transactions, known as like-kind exchanges (or 1031 exchanges), are a commonly used tax planning tool for business aircraft owners, as long as the aircraft being exchanged are held for productive use in a trade or business.

Section 1031 is part of federal law, so it applies to federal taxes, which are the same no matter what state you're in. You can perform a 1031 exchange between business or investment properties located anywhere in the United States, so long as they meet all other 1031 requirements.