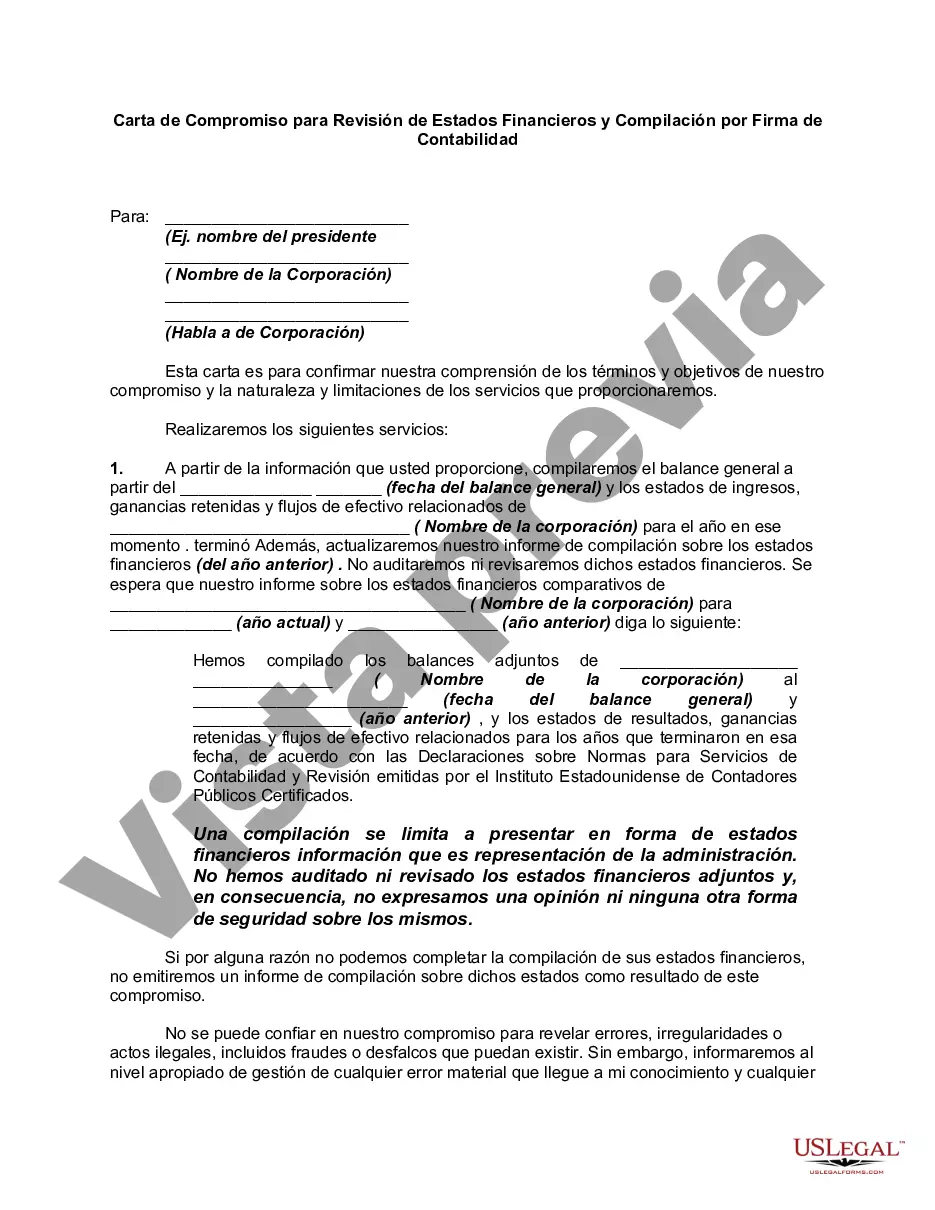

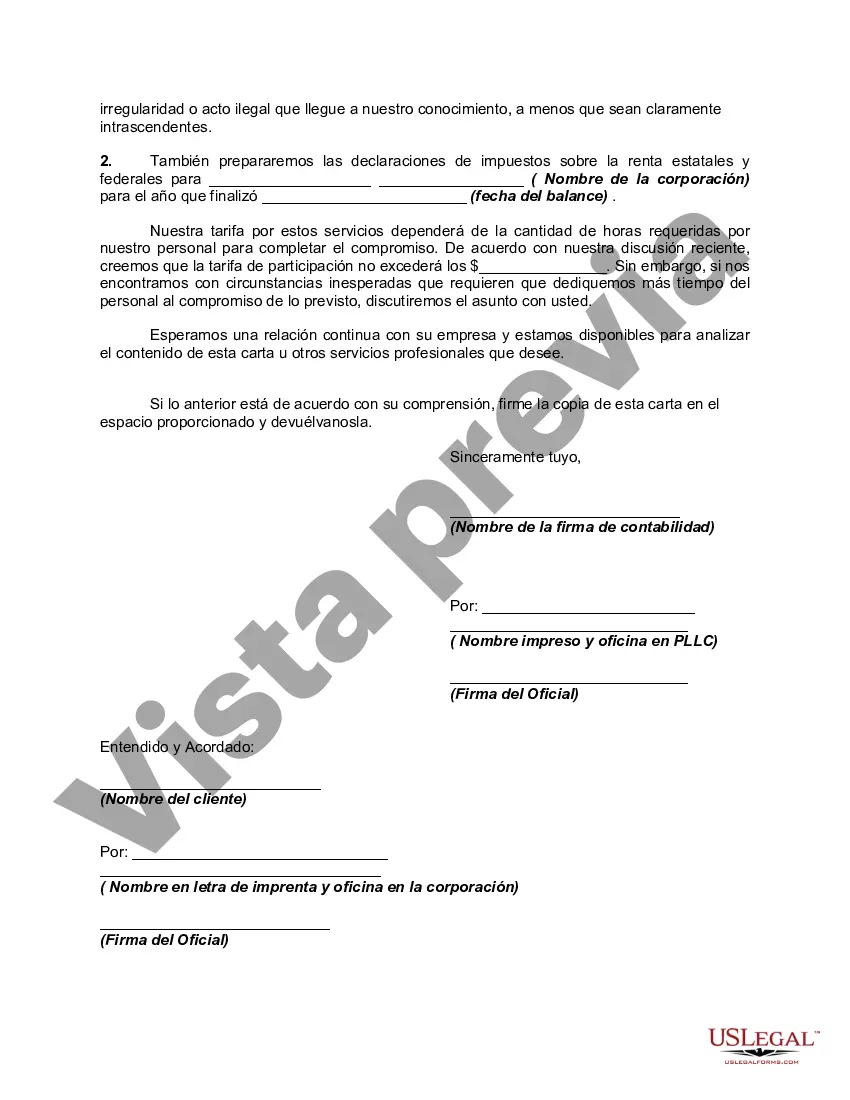

Compiled financial statements represent the most basic level of service that certified public accountants provide with respect to financial statements. In a compilation, the CPA must comply with certain basic requirements of professional standards, such as having a knowledge of the client's industry and applicable accounting principles, having a clear understanding with the client as to the services to be provided, and reading the financial statements to determine whether there are any obvious departures from generally accepted accounting principles (or, in some cases, another comprehensive basis of accounting used by the entity). It may be necessary for the CPA to perform "other accounting services" (such as creating a general ledger for the client, or assisting the client with adjusting entries for the books of the client (before the financial statements can be prepared). Upon completion, a report on the financial statements is issued that states a compilation was performed in accordance with AICPA professional standards, but no assurance is expressed that the statements are in conformity with generally accepted accounting principles. This is known as the expression of "no assurance." Compiled financial statements are often prepared for privately-held entities that do not need a higher level of assurance expressed by the CPA.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Engagement Letter For Internal Audit - Engagement Letter for Review of Financial Statements and Compilation by Accounting Firm

Description

How to fill out Engagement Letter For Internal Audit?

What is the most trustworthy service to acquire the Engagement Letter For Internal Audit and other up-to-date versions of legal paperwork? US Legal Forms is the answer! It's the greatest collection of legal documents for any use case. Every sample is appropriately drafted and verified for compliance with federal and local laws. They are collected by field and state of use, so locating the one you need is a no-brainer.

Experienced users of the platform only need to log in to the system, check if their subscription is valid, and click the Download key next to the Engagement Letter For Internal Audit to acquire it. Once saved, the sample remains available for further use within the My Forms tab of your profile. If you still don't have an account with our library, here are the steps that you need to take to get one:

- Form compliance verification. Before you acquire any template, you must check if it fulfills your use case terms and your state or county's regulations. Read the form description and take advantage of the Preview if available.

- Alternative document search. If there are any inconsistencies, use the search bar in the page header to locate a different sample. Click Buy Now to pick the right one.

- Signing up and subscription acquisition. Opt for the most appropriate pricing plan, log in or create your account, and pay for your subscription via PayPal or credit card.

- Downloading the paperwork. Choose the format you want to save the Engagement Letter For Internal Audit (PDF or DOCX) and click Download to obtain it.

US Legal Forms is a perfect solution for everyone who needs to deal with legal paperwork. Premium users can get even more as they fill out and approve the earlier saved papers electronically at any moment within the integrated PDF editing tool. Check it out today!