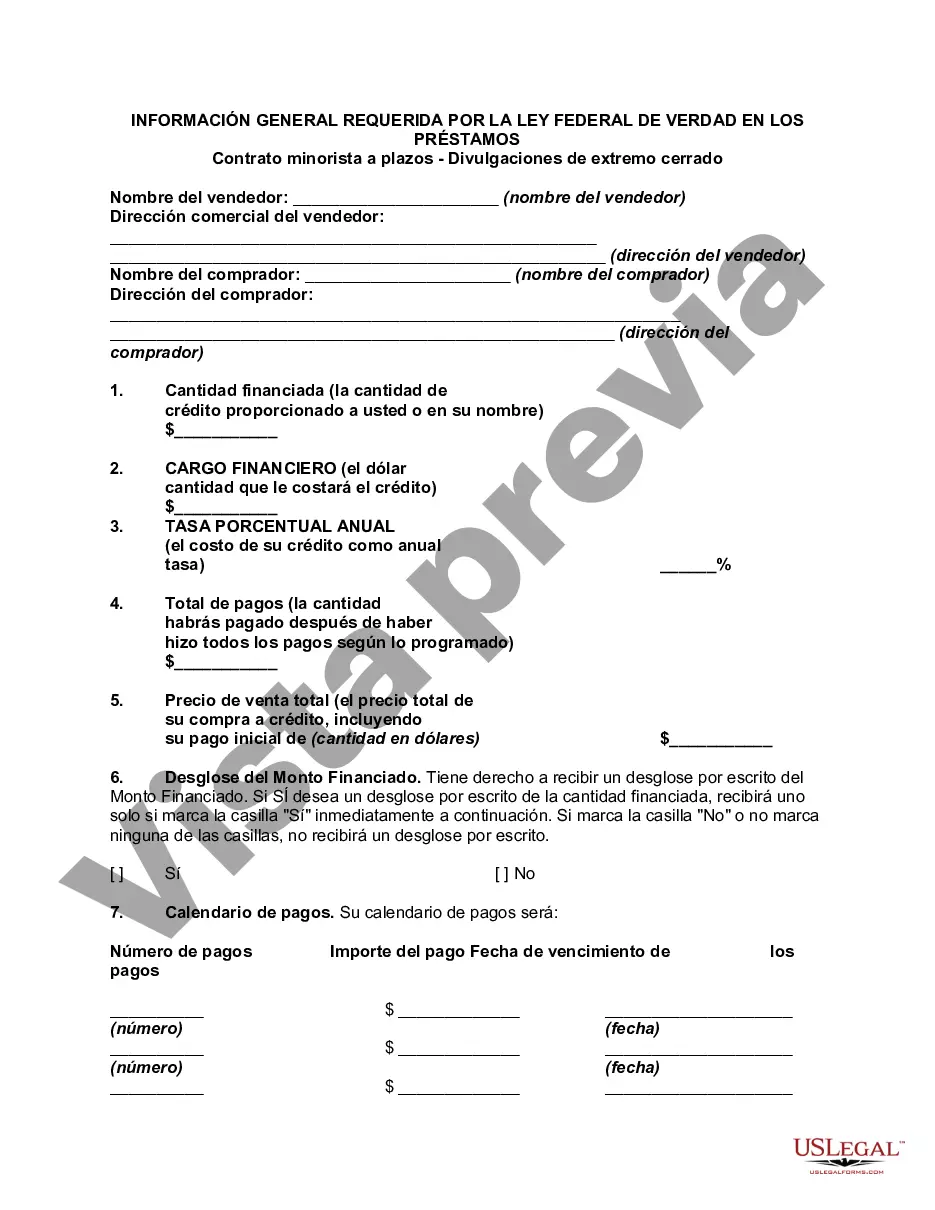

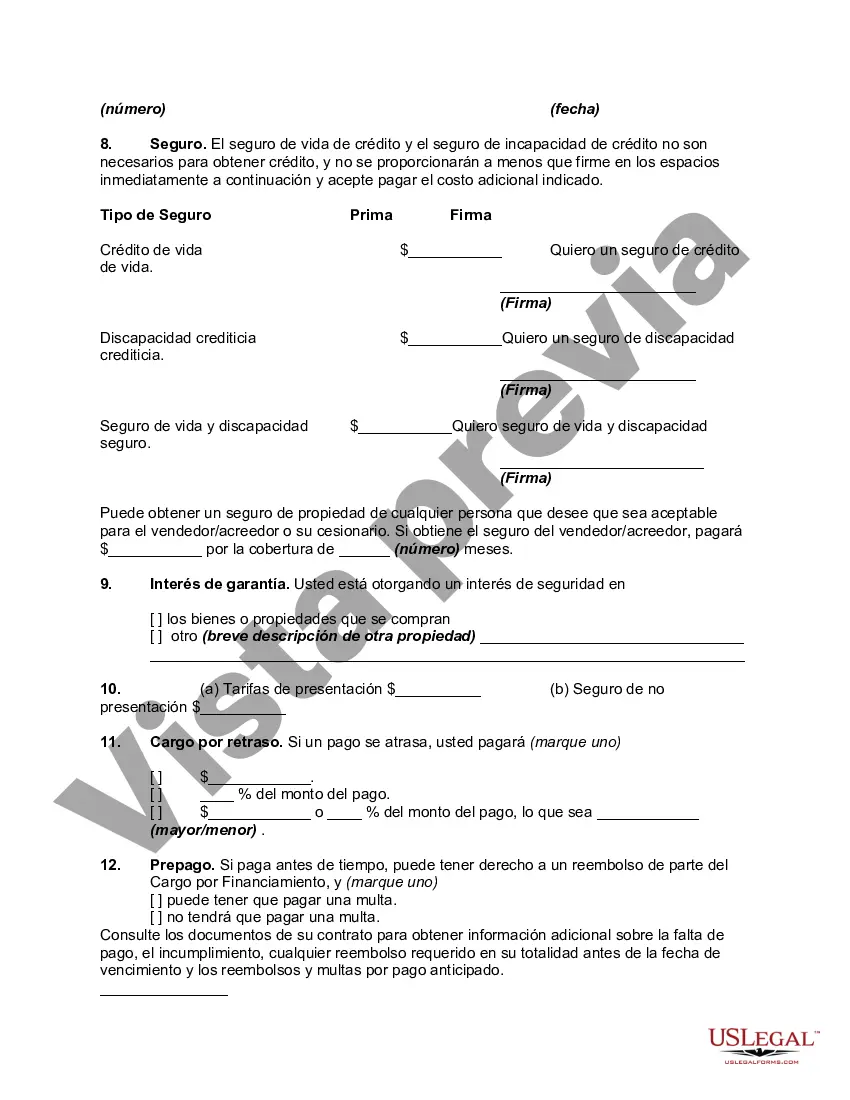

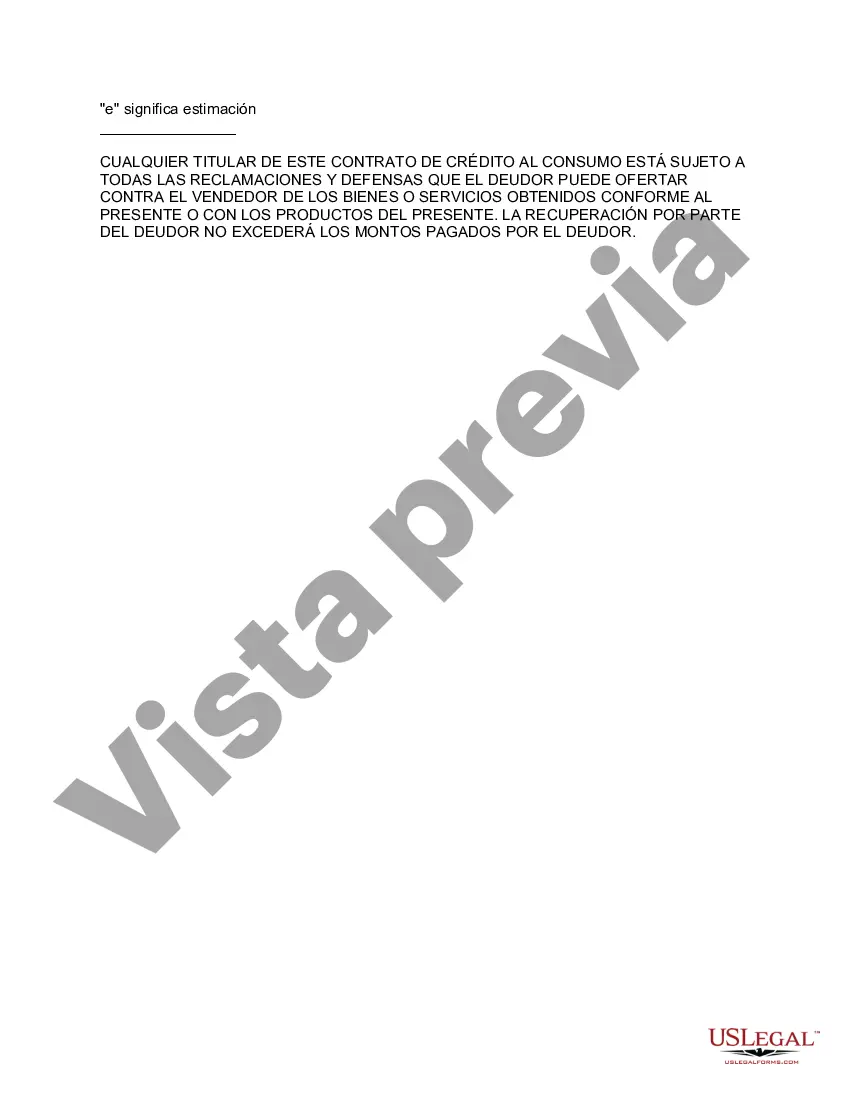

The Alabama General Disclosures Required By The Federal Truth In Lending Act — Retail InstallmenContractac— - Closed End Disclosures refer to certain mandatory disclosures that must be provided to consumers in the state of Alabama when entering into a retail installment contract for a closed-end loan. These disclosures are essential for ensuring transparency and fairness in lending practices. The Federal Truth In Lending Act (TILL) is a federal law designed to protect consumers by requiring lenders to disclose important terms and conditions of credit transactions. In Alabama, lenders must comply with TILL and provide the following general disclosures when entering into a retail installment contract: 1. Annual Percentage Rate (APR): The APR represents the total cost of credit, including both the interest rate and any other finance charges. It allows borrowers to compare the cost of different loans and make informed decisions. 2. Finance Charge: This includes all fees imposed by the lender as a condition of extending credit, excluding certain prepaid finance charges. 3. Amount Financed: This refers to the total dollar amount of credit provided to the borrower, minus any prepaid finance charges. 4. Total Payments: The total amount the borrower will repay over the life of the loan, including both the principal borrowed and the finance charge. 5. Total Sales Price: The total cost of the purchase, including any down payment, finance charge, and other fees. 6. Payment Schedule: The breakdown of periodic payments, including the number of payments, payment amount, and due dates. 7. Prepayment Penalty: If applicable, this disclosure informs borrowers about any penalties they may face for paying off the loan before the specified term. These are the general disclosures required by TILL for a retail installment contract in Alabama. However, it's important to note that there may be additional specific disclosures based on the type of loan or transaction. Such variations may include auto loans, mortgage loans, personal loans, or other specialized credit agreements. Each type of loan may have its own set of disclosures tailored to the specific terms and conditions. To fully understand the Alabama General Disclosures Required By The Federal Truth In Lending Act — Retail InstallmenContractac— - Closed End Disclosures, borrowers are encouraged to carefully review the loan agreement and consult with the lender or a qualified financial professional for any clarification needed. Complying with these disclosure requirements ensures that lenders and borrowers have a clear understanding of the terms and costs associated with the loan, promoting fairness and transparency in consumer lending.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Alabama Divulgaciones generales requeridas por la Ley Federal de Veracidad en los Préstamos - Contrato minorista a plazos - Divulgaciones cerradas - General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Description

How to fill out Alabama Divulgaciones Generales Requeridas Por La Ley Federal De Veracidad En Los Préstamos - Contrato Minorista A Plazos - Divulgaciones Cerradas?

Choosing the right authorized document template can be quite a struggle. Naturally, there are a lot of web templates available on the Internet, but how would you find the authorized develop you need? Use the US Legal Forms site. The assistance delivers a large number of web templates, including the Alabama General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, that can be used for business and private requirements. All the types are checked by experts and satisfy federal and state requirements.

When you are currently listed, log in in your profile and click the Acquire button to find the Alabama General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures. Make use of your profile to look from the authorized types you have ordered in the past. Go to the My Forms tab of the profile and obtain one more copy of your document you need.

When you are a brand new consumer of US Legal Forms, listed here are simple guidelines so that you can comply with:

- Initially, be sure you have chosen the appropriate develop for the area/state. You can look over the form while using Review button and browse the form outline to guarantee this is the best for you.

- In case the develop will not satisfy your needs, take advantage of the Seach field to get the right develop.

- Once you are certain the form is acceptable, click the Purchase now button to find the develop.

- Opt for the rates plan you want and enter the essential information. Create your profile and pay for an order with your PayPal profile or charge card.

- Opt for the data file formatting and download the authorized document template in your product.

- Full, change and print out and sign the received Alabama General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

US Legal Forms may be the biggest local library of authorized types where you will find a variety of document web templates. Use the service to download expertly-created files that comply with state requirements.