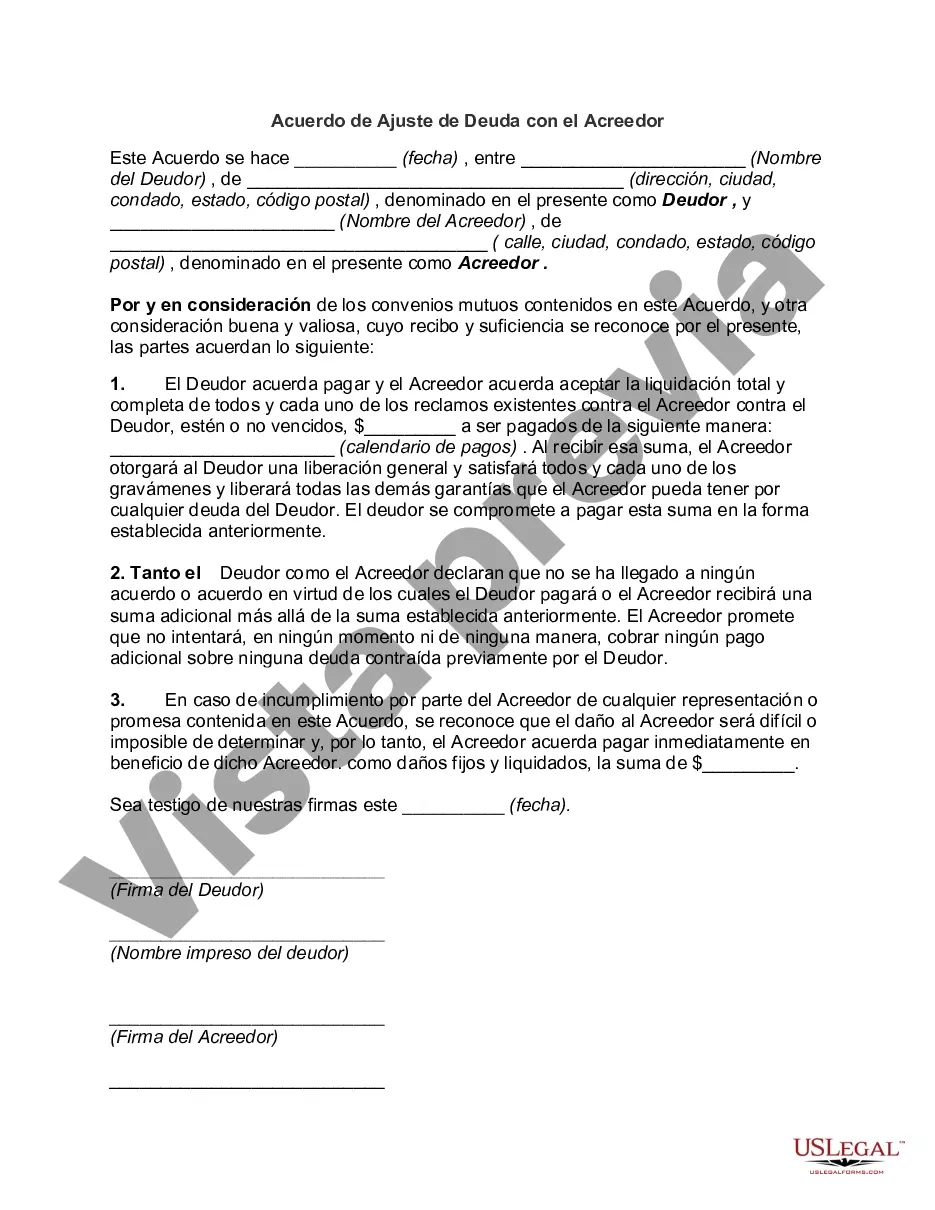

Alabama Debt Adjustment Agreement with Creditor: In Alabama, a Debt Adjustment Agreement with a Creditor refers to a legal arrangement between a debtor and their creditor. This agreement allows the debtor to restructure their outstanding debts through a formalized plan, making it more manageable to repay. This type of agreement enables individuals who are struggling financially to work out a repayment plan with their creditor. Debtors facing overwhelming debt can seek relief with the help of a debt adjustment agreement, allowing them to regain control of their finances and avoid bankruptcy. One important aspect to consider is that there are different types of Alabama Debt Adjustment Agreements with Creditors. Some common types are: 1. Debt Consolidation Agreement: This agreement combines multiple debts into a single loan or repayment plan. By consolidating debts, individuals can benefit from a lower interest rate and make a single monthly payment, simplifying their financial situation. 2. Debt Repayment Plan: Under this agreement, a debtor and creditor work together to create a structured repayment plan. This plan typically involves negotiating reduced interest rates, waived fees, or extended payment terms, making it more feasible for the debtor to repay their debt. 3. Debt Settlement Agreement: In this type of agreement, the debtor and creditor negotiate a reduced lump-sum payment to settle the debt. Creditors may agree to accept a lower amount to avoid the risk of the debtor defaulting or filing for bankruptcy. 4. Credit Counseling Agreement: Debtors who opt for credit counseling may enter into an agreement where a certified credit counselor helps negotiate lower interest rates and payment terms with the creditor. The credit counselor serves as an intermediary, assisting the debtor in creating a budget and managing their finances effectively. 5. Temporary Forbearance Agreement: This agreement allows debtors to temporarily suspend or reduce monthly payments for a set period, providing them with breathing room during a financial hardship. Once the agreed-upon period ends, regular payments resume. It is crucial to understand the terms and conditions of the Alabama Debt Adjustment Agreement with the Creditor, including any fees, interest rates, or potential impacts on creditworthiness. Debtors should consult with legal and financial professionals to ensure they choose the most suitable agreement for their specific circumstances. Remember, an Alabama Debt Adjustment Agreement with a Creditor serves as a tool to help individuals regain control over their financial lives, work towards debt repayment, and ultimately achieve financial stability.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Alabama Acuerdo de Ajuste de Deuda con el Acreedor - Debt Adjustment Agreement with Creditor

Description

How to fill out Alabama Acuerdo De Ajuste De Deuda Con El Acreedor?

US Legal Forms - one of several most significant libraries of authorized types in the States - delivers a wide range of authorized file web templates you can download or printing. Using the web site, you will get thousands of types for business and personal functions, sorted by groups, suggests, or search phrases.You will discover the most up-to-date types of types such as the Alabama Debt Adjustment Agreement with Creditor within minutes.

If you already possess a membership, log in and download Alabama Debt Adjustment Agreement with Creditor in the US Legal Forms catalogue. The Download option can look on every single kind you look at. You gain access to all earlier saved types from the My Forms tab of your profile.

If you wish to use US Legal Forms initially, allow me to share straightforward guidelines to obtain started out:

- Be sure to have picked the best kind for your personal area/state. Click on the Review option to review the form`s information. See the kind explanation to ensure that you have chosen the proper kind.

- In the event the kind does not fit your requirements, take advantage of the Look for discipline towards the top of the display to obtain the one that does.

- If you are satisfied with the shape, confirm your choice by clicking on the Purchase now option. Then, choose the prices program you want and supply your accreditations to register for an profile.

- Method the transaction. Use your bank card or PayPal profile to accomplish the transaction.

- Find the formatting and download the shape on your own device.

- Make alterations. Complete, revise and printing and indicator the saved Alabama Debt Adjustment Agreement with Creditor.

Each design you included with your bank account lacks an expiry time and it is the one you have for a long time. So, if you wish to download or printing yet another version, just proceed to the My Forms area and then click around the kind you need.

Get access to the Alabama Debt Adjustment Agreement with Creditor with US Legal Forms, by far the most extensive catalogue of authorized file web templates. Use thousands of professional and condition-particular web templates that meet your small business or personal requirements and requirements.