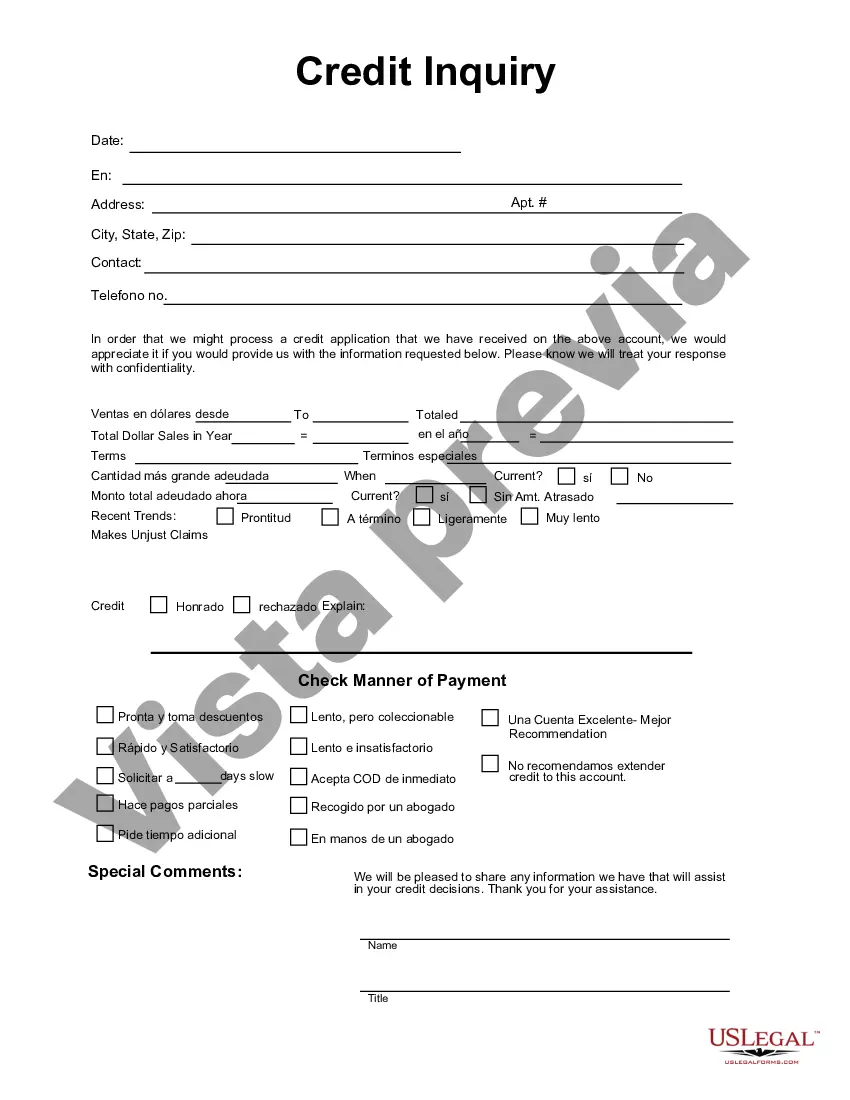

Arkansas Credit Inquiry is a term used in the realm of credit reporting and evaluation in the state of Arkansas. It refers to the process where lenders or financial institutions obtain a copy of an individual's credit report to assess their creditworthiness before making lending decisions. The credit report provides a comprehensive overview of an individual's credit history, accounts, payment history, and public records. Various types of credit inquiries can occur in Arkansas, including soft inquiries and hard inquiries. A soft inquiry occurs when a person or entity checks their own credit report or when a lender pulls the credit report without the intent of granting credit. Soft inquiries have no impact on an individual's credit score. Examples of soft inquiries in Arkansas Credit Inquiry may include a person reviewing their own credit report, credit card companies doing periodic account reviews, or insurance companies checking credit history for underwriting purposes. On the other hand, a hard inquiry is initiated when a financial institution pulls an individual's credit report with the intent of making a lending decision. Hard inquiries are typically triggered when someone applies for credit, such as a credit card, mortgage, auto loan, or personal loan. Each hard inquiry can potentially impact an individual's credit score and remains on the credit report for up to two years. In Arkansas, hard inquiries are crucial for lenders to assess a borrower's creditworthiness and determine the terms and conditions of the credit they are seeking. It is essential for individuals to be aware of the different types of Arkansas Credit Inquiry, as too many hard inquiries within a short period can negatively impact credit scores. However, multiple inquiries within a specific timeframe (typically 14-45 days) for the same type of loan are often treated as a single inquiry by credit scoring models. This allows borrowers to shop around for the best loan terms without worrying about excessive credit score deductions. Additionally, it is important to note that certain entities, such as employers or landlords, may request a modified version of a credit report called a "consumer report" for employment or rental application purposes. These inquiries are regulated by the Fair Credit Reporting Act (FCRA) and do not impact an individual's credit score. In conclusion, Arkansas Credit Inquiry encompasses the process of obtaining and reviewing credit reports to evaluate an individual's creditworthiness. Soft inquiries have no impact on credit scores and are often initiated by individuals or entities for personal or periodic review purposes. Meanwhile, hard inquiries occur when lenders or financial institutions pull credit reports with the intention of lending credit, and they can impact credit scores. It is crucial for individuals to be aware of the various types of inquiries to maintain a healthy credit profile.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Arkansas Consulta de crédito - Credit Inquiry

Description

How to fill out Arkansas Consulta De Crédito?

Are you presently in a position where you will need documents for sometimes company or individual uses nearly every day time? There are plenty of authorized file themes available online, but getting ones you can depend on isn`t easy. US Legal Forms delivers a huge number of type themes, just like the Arkansas Credit Inquiry, which are published in order to meet state and federal needs.

Should you be presently knowledgeable about US Legal Forms site and also have your account, just log in. Afterward, you can obtain the Arkansas Credit Inquiry template.

Should you not provide an bank account and want to begin to use US Legal Forms, adopt these measures:

- Get the type you need and ensure it is for that appropriate area/state.

- Make use of the Review switch to analyze the form.

- Read the information to ensure that you have chosen the right type.

- When the type isn`t what you`re looking for, make use of the Research industry to discover the type that meets your requirements and needs.

- When you discover the appropriate type, click Buy now.

- Pick the prices strategy you desire, fill in the specified information and facts to create your bank account, and purchase the order with your PayPal or bank card.

- Select a convenient document formatting and obtain your version.

Locate each of the file themes you may have purchased in the My Forms food list. You can obtain a more version of Arkansas Credit Inquiry any time, if possible. Just select the essential type to obtain or print out the file template.

Use US Legal Forms, the most comprehensive variety of authorized forms, to save lots of some time and prevent blunders. The service delivers skillfully manufactured authorized file themes which you can use for a range of uses. Create your account on US Legal Forms and start making your life easier.