A Line of Credit refers to the maximum borrowing power that a lender extends to a borrower. The borrower may draw required amounts from the fixed amount. Usually, it is a credit source extended to any credit-worthy business by a bank or any financial institution. A line of credit includes cash credit, overdraft, demand loan, export packing credit, term loan, discounting or purchase of commercial bills, etc. The borrower may use the line of credit to overcome liquidity problems. Requisite amounts may be withdrawn from the account as and when required. The borrower pays interest only for the amount withdrawn.

A Colorado Line of Credit Promissory Note is a legally binding document that outlines the terms and conditions between a borrower and a lender regarding a line of credit. This financial agreement serves as a legally enforceable contract that ensures both parties adhere to their agreed-upon obligations. It is essential to thoroughly understand the elements and provisions of a Line of Credit Promissory Note when considering entering into this type of financial transaction in Colorado. The Colorado Line of Credit Promissory Note typically begins with a detailed introductory section, which specifies the names, addresses, and contact information of the borrower and lender. This section establishes the identities of the parties involved and ensures clarity in later sections of the note. Additionally, it may outline the governing law and jurisdiction to be followed in case of any disputes or legal matters. The note then proceeds to outline the loan terms, which include the principal amount borrowed, the interest rate applied to the outstanding balance, and any fees associated with the line of credit. This section also defines the repayment provisions, such as the repayment schedule, the frequency of payments, and the duration of the note. It may include details on whether the interest is fixed or variable, and if there are any penalties or fees for early repayment. Furthermore, the note should highlight the rights and responsibilities of both the borrower and the lender. It may include provisions specifying how funds can be withdrawn from the line of credit and any restrictions on the use of the borrowed funds. The responsibilities of the borrower regarding timely repayments, keeping accurate records, and maintaining the line of credit within the agreed limits should also be included. In addition to the general Colorado Line of Credit Promissory Note, specific types may exist, tailored to suit varying financial circumstances and needs. Some examples may include secured lines of credit, where the borrower provides collateral to secure the loan, or unsecured lines of credit, which require no collateral. There may also be fixed-rate or variable-rate line of credit promissory notes, depending on whether the interest rate remains the same or fluctuates over time. Considering the importance of accuracy in financial documentation, it is advisable for both parties to seek legal advice before finalizing and signing a Colorado Line of Credit Promissory Note. By doing so, they can ensure that all legal requirements are met, their interests are protected, and they fully understand their rights and obligations.A Colorado Line of Credit Promissory Note is a legally binding document that outlines the terms and conditions between a borrower and a lender regarding a line of credit. This financial agreement serves as a legally enforceable contract that ensures both parties adhere to their agreed-upon obligations. It is essential to thoroughly understand the elements and provisions of a Line of Credit Promissory Note when considering entering into this type of financial transaction in Colorado. The Colorado Line of Credit Promissory Note typically begins with a detailed introductory section, which specifies the names, addresses, and contact information of the borrower and lender. This section establishes the identities of the parties involved and ensures clarity in later sections of the note. Additionally, it may outline the governing law and jurisdiction to be followed in case of any disputes or legal matters. The note then proceeds to outline the loan terms, which include the principal amount borrowed, the interest rate applied to the outstanding balance, and any fees associated with the line of credit. This section also defines the repayment provisions, such as the repayment schedule, the frequency of payments, and the duration of the note. It may include details on whether the interest is fixed or variable, and if there are any penalties or fees for early repayment. Furthermore, the note should highlight the rights and responsibilities of both the borrower and the lender. It may include provisions specifying how funds can be withdrawn from the line of credit and any restrictions on the use of the borrowed funds. The responsibilities of the borrower regarding timely repayments, keeping accurate records, and maintaining the line of credit within the agreed limits should also be included. In addition to the general Colorado Line of Credit Promissory Note, specific types may exist, tailored to suit varying financial circumstances and needs. Some examples may include secured lines of credit, where the borrower provides collateral to secure the loan, or unsecured lines of credit, which require no collateral. There may also be fixed-rate or variable-rate line of credit promissory notes, depending on whether the interest rate remains the same or fluctuates over time. Considering the importance of accuracy in financial documentation, it is advisable for both parties to seek legal advice before finalizing and signing a Colorado Line of Credit Promissory Note. By doing so, they can ensure that all legal requirements are met, their interests are protected, and they fully understand their rights and obligations.

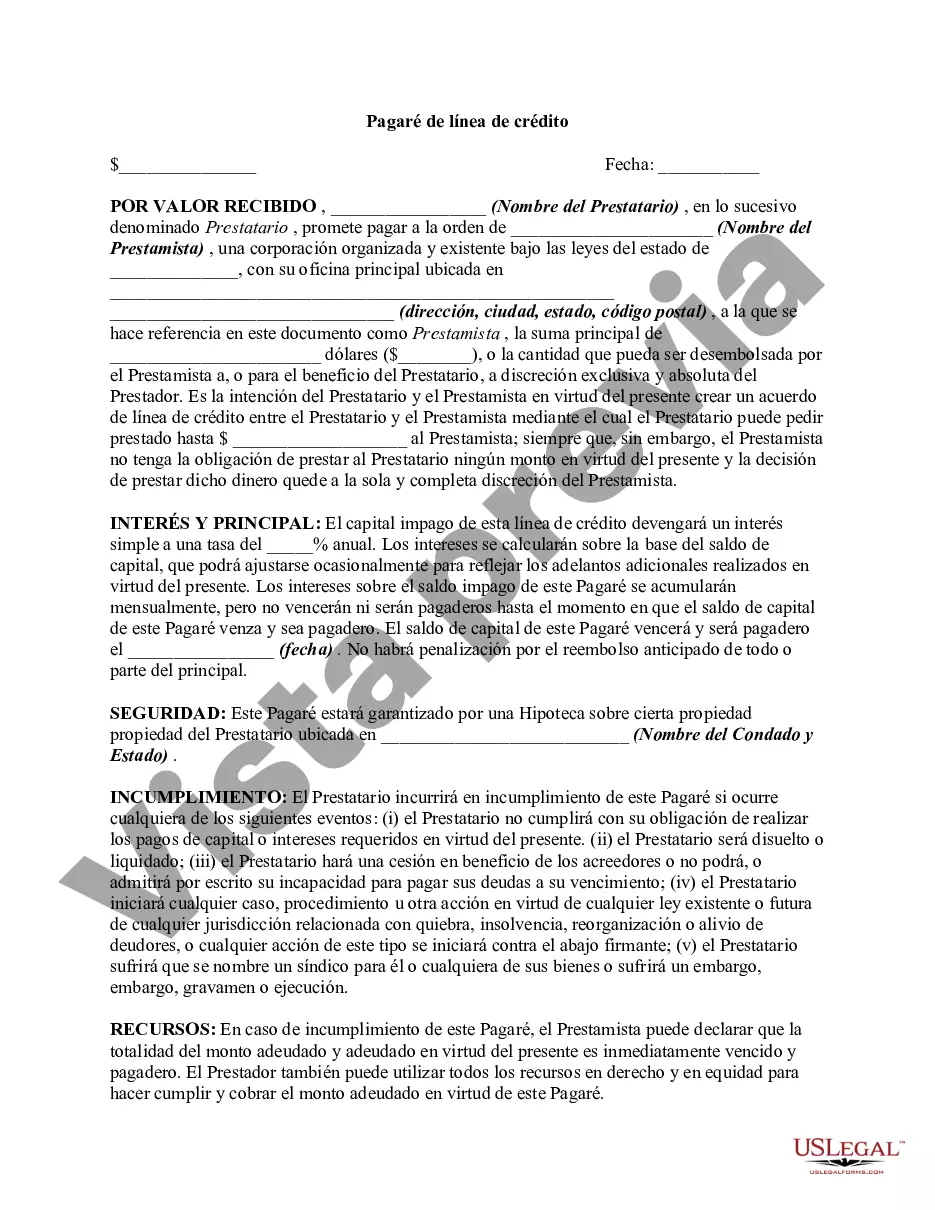

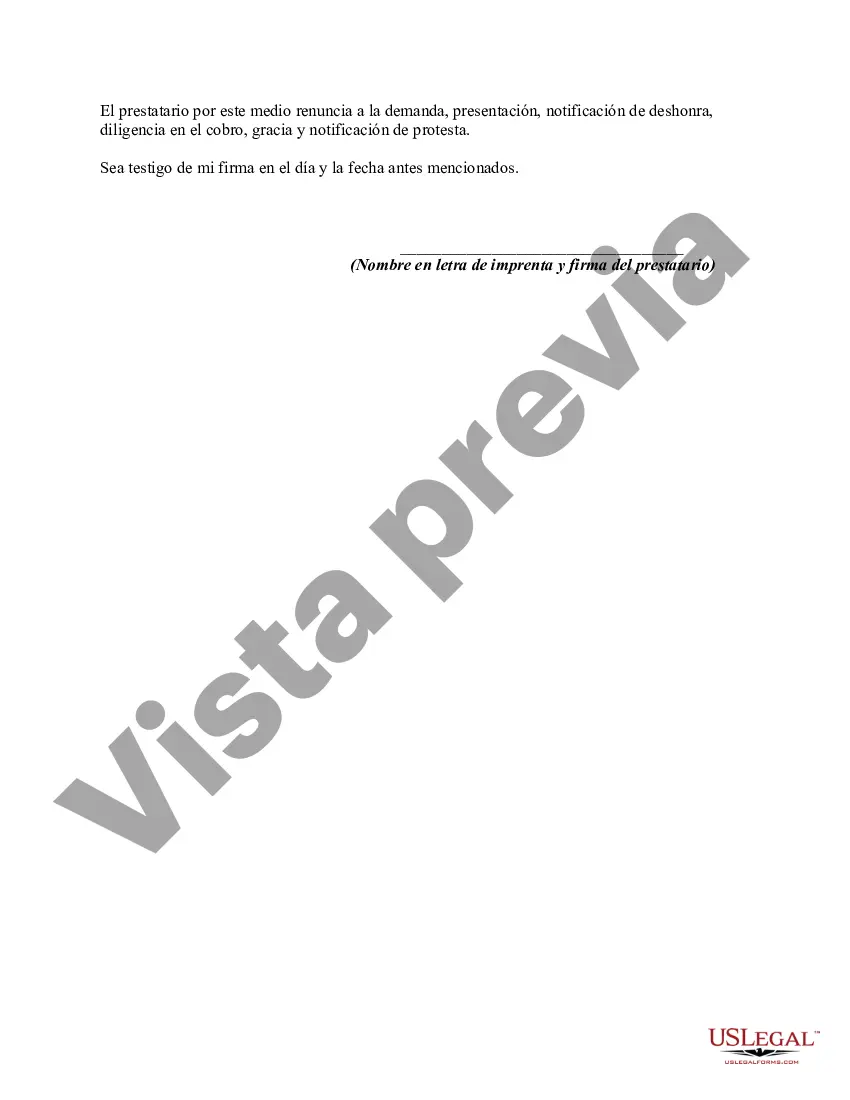

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.