Connecticut Agreement to Compromise Debt, also known as the Compromise and Settlement Agreement, is a legal document that outlines the terms and conditions for resolving a debt dispute between a creditor and a debtor in the state of Connecticut, United States. This agreement allows the parties involved to negotiate a mutually beneficial agreement and avoid potential lawsuits or collections actions. Keywords: Connecticut Agreement to Compromise Debt, Compromise and Settlement Agreement, debt dispute, creditor, debtor, Connecticut, United States, negotiate, mutually beneficial agreement, lawsuits, collections actions. There are different types of Connecticut Agreements to Compromise Debt that can be used depending on the specific circumstances: 1. Individual Debt Compromise Agreement: This type of agreement is entered into between an individual debtor and a creditor and addresses a personal debt issue. It provides a framework within which the parties can agree upon a reduced repayment amount or modified payment terms to resolve the outstanding debt. 2. Business Debt Compromise Agreement: When a business entity is involved in a debt dispute, this type of agreement comes into play. It allows businesses to negotiate reduced payment amounts or extended payment terms to settle their outstanding debts. This agreement helps protect the business's financial stability while addressing the creditor's need for debt recovery. 3. Medical Debt Compromise Agreement: In cases where medical expenses are in dispute, this type of agreement is used. It allows individuals or healthcare providers to negotiate a compromise and settle outstanding medical bills. The agreement may involve reducing the total amount owed, establishing a payment plan, or a combination of both. 4. Tax Debt Compromise Agreement: When taxpayers have unresolved tax liabilities with the Connecticut Department of Revenue Services (DRS), they may have the option to enter into a tax debt compromise agreement. This type of agreement enables taxpayers to settle their tax debts for a reduced amount, often through a lump-sum payment or installment plan, thereby providing relief from financial burdens. 5. Mortgage Debt Compromise Agreement: In situations where homeowners are struggling to meet their mortgage payments, a mortgage debt compromise agreement can be considered. This agreement allows borrowers and mortgage lenders to negotiate revised repayment terms, such as a temporary reduction in monthly payments, loan modification, or repayment plan, to avoid foreclosure and find a viable solution. In conclusion, the Connecticut Agreement to Compromise Debt is a valuable legal tool that facilitates debt resolution in various contexts, including individual, business, medical, tax, and mortgage-related debts. It provides a structured approach, protecting the interests of both parties involved while allowing for flexible and customizable solutions to overcome debt-related challenges.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Connecticut Acuerdo de Compromiso de Deuda - Agreement to Compromise Debt

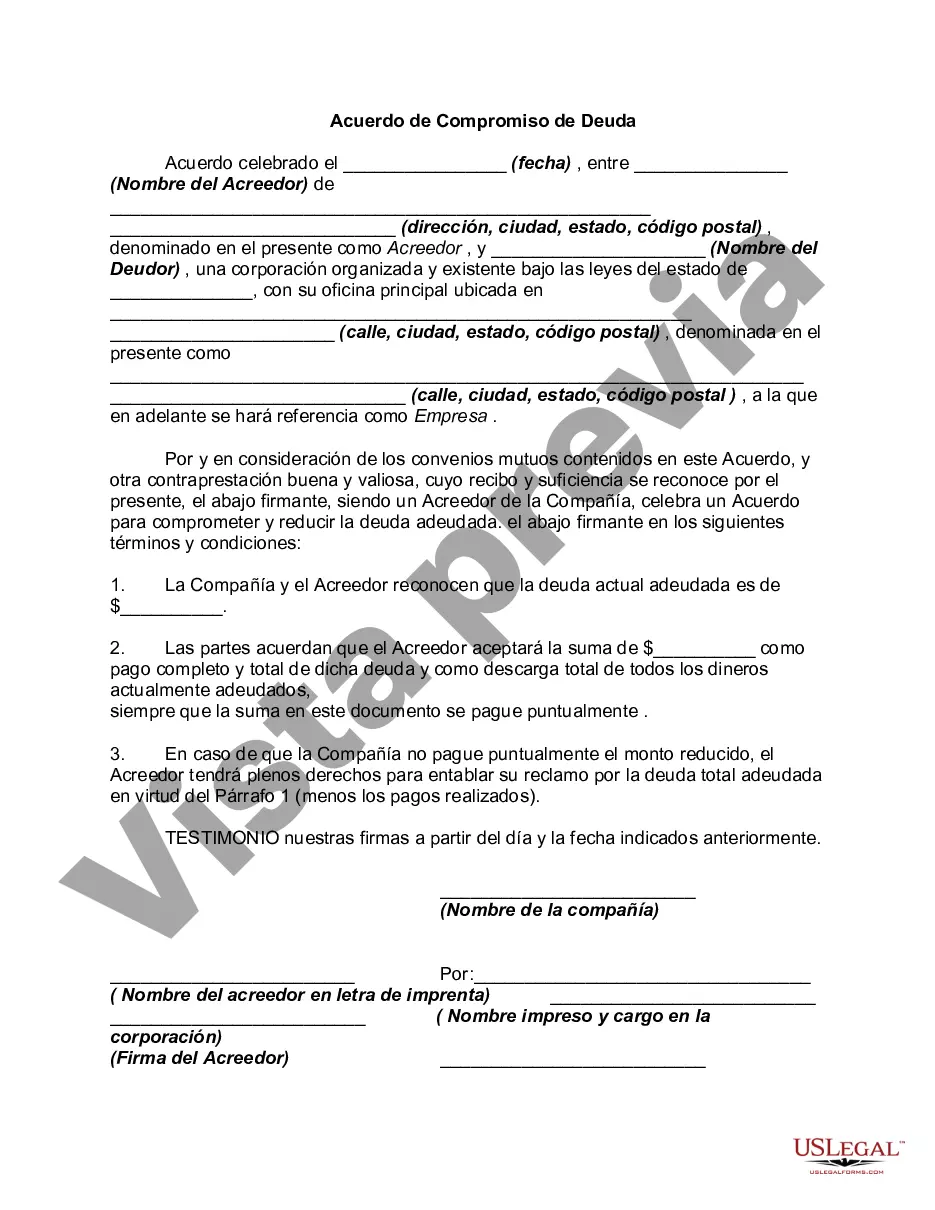

Description

How to fill out Connecticut Acuerdo De Compromiso De Deuda?

Choosing the right lawful file template could be a have difficulties. Obviously, there are a variety of themes available on the net, but how will you find the lawful kind you require? Take advantage of the US Legal Forms internet site. The services offers a large number of themes, such as the Connecticut Agreement to Compromise Debt, that can be used for company and private needs. All of the forms are checked out by professionals and meet up with federal and state needs.

In case you are already authorized, log in for your profile and click the Acquire button to obtain the Connecticut Agreement to Compromise Debt. Utilize your profile to appear from the lawful forms you might have bought earlier. Check out the My Forms tab of your profile and acquire another backup of the file you require.

In case you are a brand new consumer of US Legal Forms, listed below are easy guidelines so that you can comply with:

- Very first, ensure you have chosen the appropriate kind for your personal metropolis/region. It is possible to look over the shape making use of the Review button and look at the shape explanation to make certain it will be the right one for you.

- In case the kind does not meet up with your requirements, use the Seach field to get the correct kind.

- When you are sure that the shape is acceptable, click on the Purchase now button to obtain the kind.

- Opt for the rates program you want and type in the necessary info. Make your profile and pay money for the transaction utilizing your PayPal profile or credit card.

- Select the submit structure and obtain the lawful file template for your system.

- Full, modify and produce and indicator the acquired Connecticut Agreement to Compromise Debt.

US Legal Forms will be the greatest library of lawful forms that you will find numerous file themes. Take advantage of the service to obtain expertly-created files that comply with express needs.