This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

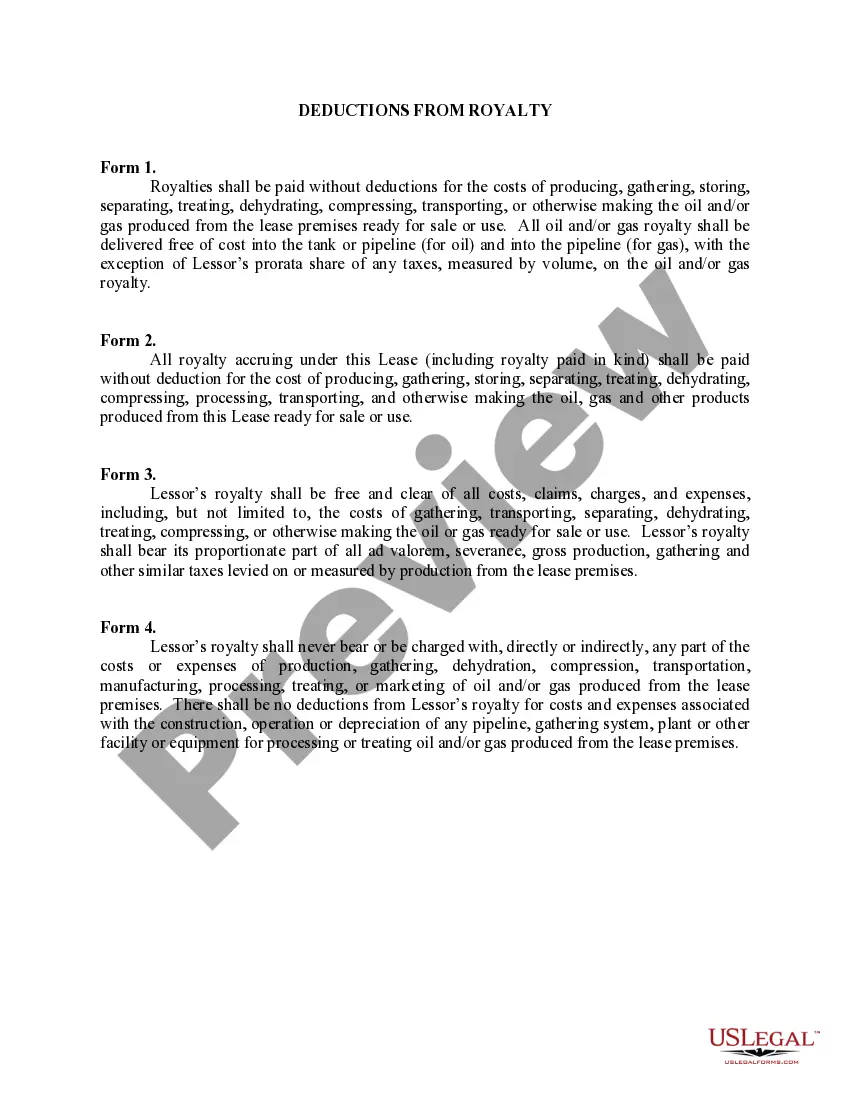

Connecticut Deductions from Royalty refer to specific tax deductions available to businesses in the state of Connecticut that receive royalty income. Royalty income is generated when a person or business earns revenue from the use or sale of intellectual property, such as patents, copyrights, trademarks, or trade secrets. These deductions are designed to incentivize businesses to develop and commercialize their intellectual property within the state. By offering deductions, Connecticut aims to attract and retain companies that rely on the creation and licensing of intellectual property, fostering innovation and economic growth. The Connecticut Department of Revenue Services (DRS) provides guidelines regarding the deductions from royalty that businesses can claim on their state tax returns. It is important for businesses to understand and correctly apply these deductions to optimize their tax savings. There are two primary types of deductions related to royalties in Connecticut: 1. Connecticut Deduction for Patent and Copyright Royalties: This deduction allows businesses to deduct a certain percentage of their royalty income derived from patents and copyrights. This includes revenue generated from licensing the use of patents or copyrights, as well as income from the sale of patented or copyrighted products. To qualify, the patent or copyright must be registered or granted under federal law and must have a useful lifespan of at least 17 years. 2. Connecticut Deduction for Trademark and Trade Secret Royalties: This deduction enables businesses to deduct a percentage of their royalty income derived from trademarks and trade secrets. It applies to royalties earned from licensing the use of trademarks and trade secrets, as well as income from the sale of products featuring trademarked logos or protected trade secrets. To be eligible for this deduction, the trademark or trade secret must be used in trade or business operations within Connecticut. To claim these deductions, businesses must maintain accurate records detailing their royalty income, expenses related to intellectual property development, and any licenses or registrations associated with the patents, copyrights, trademarks, or trade secrets. Proper documentation is crucial to support the deductions and comply with the DRS requirements. It is recommended that businesses consult with a tax professional or an accountant familiar with Connecticut tax laws to ensure they fully understand and utilize the deductions available to them. Properly claiming these deductions can result in significant tax savings for businesses operating within the state.Connecticut Deductions from Royalty refer to specific tax deductions available to businesses in the state of Connecticut that receive royalty income. Royalty income is generated when a person or business earns revenue from the use or sale of intellectual property, such as patents, copyrights, trademarks, or trade secrets. These deductions are designed to incentivize businesses to develop and commercialize their intellectual property within the state. By offering deductions, Connecticut aims to attract and retain companies that rely on the creation and licensing of intellectual property, fostering innovation and economic growth. The Connecticut Department of Revenue Services (DRS) provides guidelines regarding the deductions from royalty that businesses can claim on their state tax returns. It is important for businesses to understand and correctly apply these deductions to optimize their tax savings. There are two primary types of deductions related to royalties in Connecticut: 1. Connecticut Deduction for Patent and Copyright Royalties: This deduction allows businesses to deduct a certain percentage of their royalty income derived from patents and copyrights. This includes revenue generated from licensing the use of patents or copyrights, as well as income from the sale of patented or copyrighted products. To qualify, the patent or copyright must be registered or granted under federal law and must have a useful lifespan of at least 17 years. 2. Connecticut Deduction for Trademark and Trade Secret Royalties: This deduction enables businesses to deduct a percentage of their royalty income derived from trademarks and trade secrets. It applies to royalties earned from licensing the use of trademarks and trade secrets, as well as income from the sale of products featuring trademarked logos or protected trade secrets. To be eligible for this deduction, the trademark or trade secret must be used in trade or business operations within Connecticut. To claim these deductions, businesses must maintain accurate records detailing their royalty income, expenses related to intellectual property development, and any licenses or registrations associated with the patents, copyrights, trademarks, or trade secrets. Proper documentation is crucial to support the deductions and comply with the DRS requirements. It is recommended that businesses consult with a tax professional or an accountant familiar with Connecticut tax laws to ensure they fully understand and utilize the deductions available to them. Properly claiming these deductions can result in significant tax savings for businesses operating within the state.