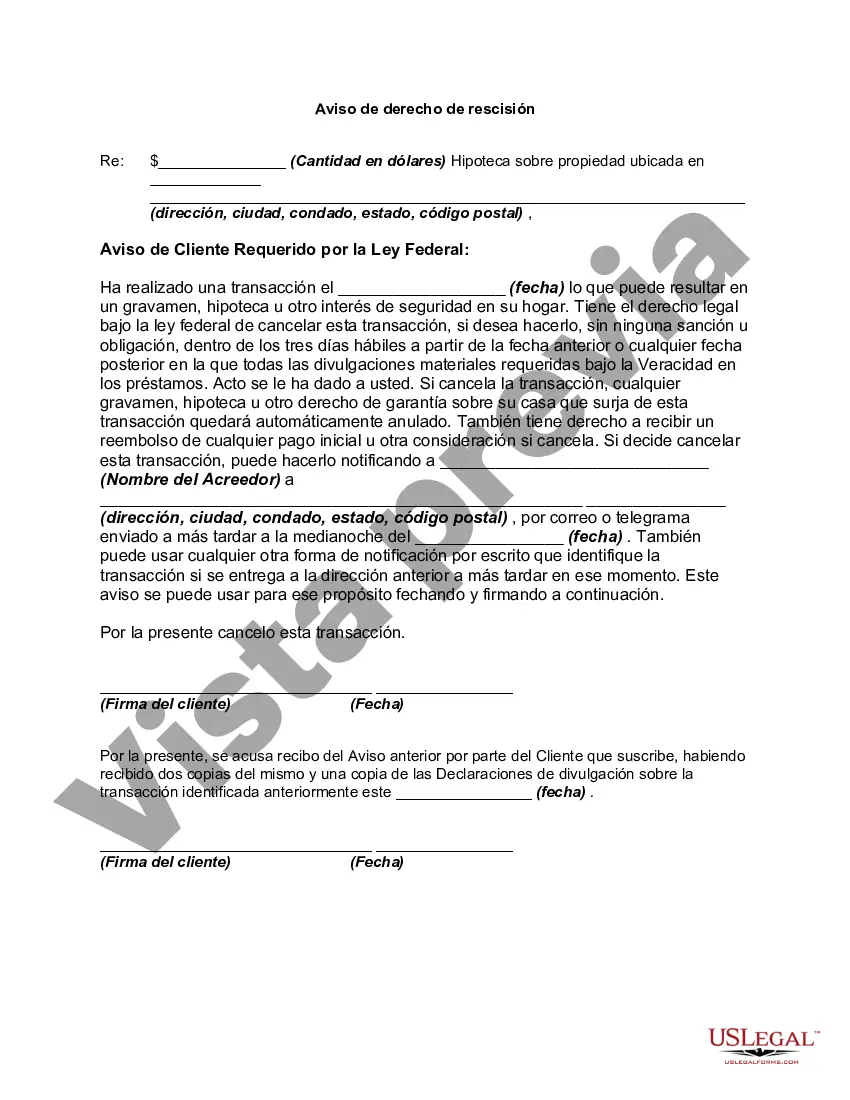

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

The District of Columbia Right to Rescind when a Security Interest in a Consumer's Principal Dwelling is Involved — Rescission allows consumers in the District of Columbia to cancel certain mortgage transactions that involve their principal residence. This right to rescind provides homeowners with an important safeguard to protect their interests and ensure transparency in lending practices. Under the District of Columbia Right to Rescind, consumers have the legal right to cancel a mortgage transaction within a specific time frame if the loan involves their principal dwelling. This right is particularly relevant when a security interest, such as a mortgage or a home equity line of credit, is taken against the consumer's principal residence. The process of rescission requires consumers to notify the lender in writing within three business days from the date of the transaction. By exercising this right, consumers can effectively cancel the loan agreement and take back ownership of their property free from the encumbrance of the security interest. This right empowers homeowners to reassess their financial choices and protect their homes from potentially burdensome obligations. It is important to note that the District of Columbia Right to Rescind when a security interest in a consumer's principal dwelling is involved applies to specific mortgage transactions governed by federal laws. Different types of applicable transactions include refinancing, home equity loans, or second mortgages. These transactions involve borrowing against the equity in the consumer's home and, as such, fall under the purview of the District of Columbia Right to Rescind. In cases where consumers exercise their right to rescind, the lender must promptly return any money or property received as part of the transaction. The cancellation of the loan agreement also voids the security interest created by the transaction, effectively restoring the consumer's ownership rights to their principal dwelling. Rescission serves as a vital consumer protection mechanism, ensuring that homeowners are not bound by unfavorable loan terms or predatory lending practices. This right grants District of Columbia residents the ability to review and reconsider their mortgage decisions, contributing to fair and transparent lending practices in the region. In conclusion, the District of Columbia Right to Rescind when a security interest in a consumer's principal dwelling is involved — Rescission allows homeowners to cancel mortgage transactions within a specific time period. This essential right protects consumers from potentially disadvantageous loan terms and predatory lending practices, granting them the ability to reassess their financial choices and reclaim ownership of their homes. Different types of applicable transactions include refinancing, home equity loans, or second mortgages.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.