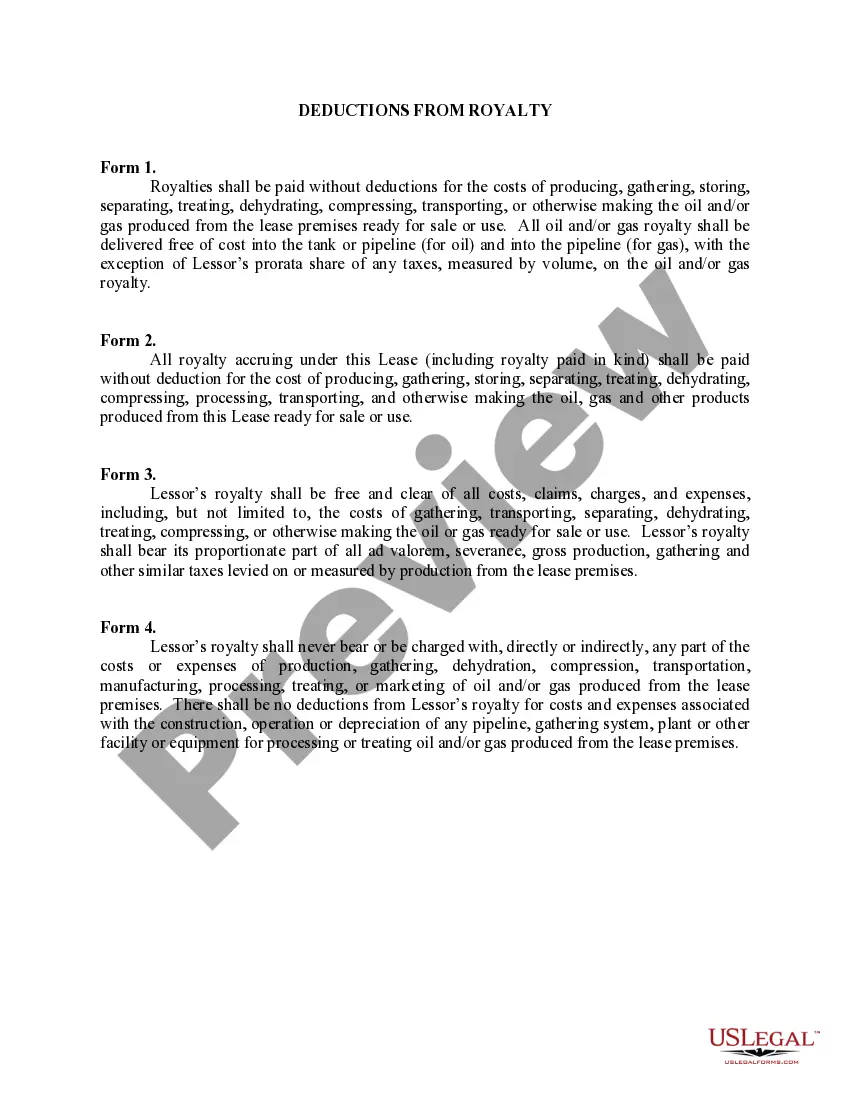

This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

District of Columbia Deductions from Royalty refer to the specific rules and regulations surrounding the deductions applied to royalty income in the District of Columbia. These deductions play a crucial role in determining the taxable income of individuals or businesses receiving royalty payments within the jurisdiction of the District of Columbia. Understanding these deductions is essential for taxpayers and royalty recipients to accurately report and calculate their tax liability. Let's delve into the various types of District of Columbia Deductions from Royalty: 1. Ordinary and Necessary Expenses: Taxpayers in the District of Columbia are allowed to deduct ordinary and necessary expenses directly related to the generation of royalty income. These expenses might include costs associated with producing, manufacturing, extracting, or developing the copyrighted works, patents, trademarks, or other intellectual properties generating royalties. 2. Transaction Costs: Royalty recipients often incur transaction costs such as legal fees, commissions, and other expenses related to the acquisition, production, or sale of the underlying intellectual property rights. The District of Columbia allows taxpayers to deduct these transaction costs from their royalty income, resulting in a lower taxable amount. 3. Depletion Allowance: In some cases, royalty income may derive from the extraction or depletion of natural resources, like minerals, oils, or gases. The District of Columbia permits a depletion deduction to compensate for the reduction or exhaustion of these resources, thereby reducing the taxable income. 4. Depreciation and Amortization: Royalty recipients might have acquired or developed assets, such as buildings, machinery, or copyrights, which gradually lose their value over time. District of Columbia tax laws allow for depreciation deductions on tangible assets and amortization deductions on intangible assets, enabling taxpayers to gradually recover the initial investment. 5. Self-Employment Tax Deductions: Individuals who receive royalty income as self-employed individuals in the District of Columbia can deduct a portion of their self-employment tax. This deduction represents the employer's share of employment taxes, providing some relief for self-employed creative professionals or entrepreneurs. It is essential to consult a tax professional or refer to the official guidelines provided by the District of Columbia's tax authorities to ensure accurate application of these deductions. Remaining up-to-date with any potential changes in tax laws and regulations is also crucial for complying with the District's tax obligations while maximizing eligible deductions.District of Columbia Deductions from Royalty refer to the specific rules and regulations surrounding the deductions applied to royalty income in the District of Columbia. These deductions play a crucial role in determining the taxable income of individuals or businesses receiving royalty payments within the jurisdiction of the District of Columbia. Understanding these deductions is essential for taxpayers and royalty recipients to accurately report and calculate their tax liability. Let's delve into the various types of District of Columbia Deductions from Royalty: 1. Ordinary and Necessary Expenses: Taxpayers in the District of Columbia are allowed to deduct ordinary and necessary expenses directly related to the generation of royalty income. These expenses might include costs associated with producing, manufacturing, extracting, or developing the copyrighted works, patents, trademarks, or other intellectual properties generating royalties. 2. Transaction Costs: Royalty recipients often incur transaction costs such as legal fees, commissions, and other expenses related to the acquisition, production, or sale of the underlying intellectual property rights. The District of Columbia allows taxpayers to deduct these transaction costs from their royalty income, resulting in a lower taxable amount. 3. Depletion Allowance: In some cases, royalty income may derive from the extraction or depletion of natural resources, like minerals, oils, or gases. The District of Columbia permits a depletion deduction to compensate for the reduction or exhaustion of these resources, thereby reducing the taxable income. 4. Depreciation and Amortization: Royalty recipients might have acquired or developed assets, such as buildings, machinery, or copyrights, which gradually lose their value over time. District of Columbia tax laws allow for depreciation deductions on tangible assets and amortization deductions on intangible assets, enabling taxpayers to gradually recover the initial investment. 5. Self-Employment Tax Deductions: Individuals who receive royalty income as self-employed individuals in the District of Columbia can deduct a portion of their self-employment tax. This deduction represents the employer's share of employment taxes, providing some relief for self-employed creative professionals or entrepreneurs. It is essential to consult a tax professional or refer to the official guidelines provided by the District of Columbia's tax authorities to ensure accurate application of these deductions. Remaining up-to-date with any potential changes in tax laws and regulations is also crucial for complying with the District's tax obligations while maximizing eligible deductions.