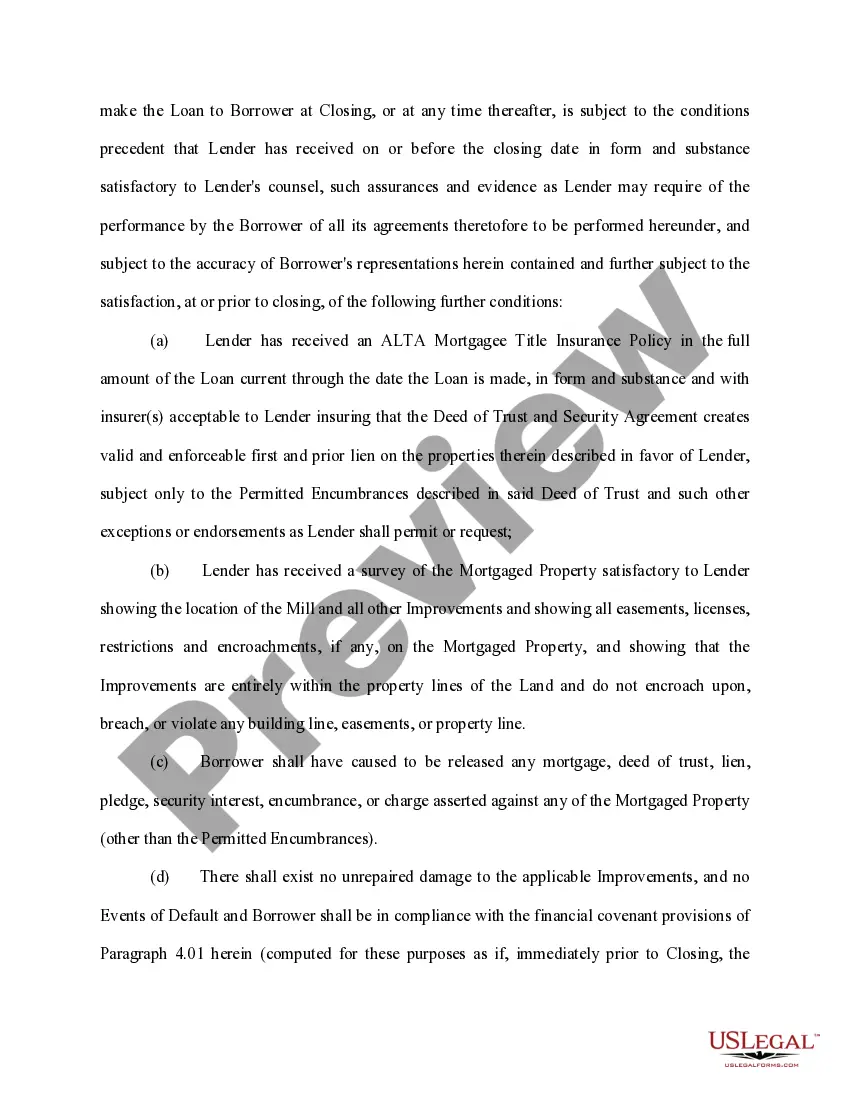

Delaware Loan Agreement for Vehicle is a legally binding document that outlines the terms and conditions under which a loan is provided to individuals or businesses in Delaware to finance the purchase of a vehicle. In this agreement, the lender (often a financial institution or individual) provides a specific amount of money to the borrower, while the borrower agrees to repay the loan within a predetermined period, plus any applicable interest charges. The Delaware Loan Agreement for Vehicle typically includes essential information, such as the names and contact details of the borrower and lender, the vehicle's description (make, model, year, identification number), the loan amount, interest rate, repayment schedule, and any collateral or security provided by the borrower. Additionally, the agreement may contain provisions regarding late payment fees, default consequences, and dispute resolution procedures. It is worth noting that there are several types of Delaware Loan Agreement for Vehicle, depending on the specific circumstances and preferences of the parties involved. Some variations include: 1. Secured Loan Agreement: This agreement involves pledging the vehicle or other valuable assets as collateral, providing the lender with a security interest in case of default, which helps reduce the risk for the lender and may result in a lower interest rate for the borrower. 2. Unsecured Loan Agreement: In this type of agreement, there is no collateral involved. The lender, relying solely on the borrower's creditworthiness, agrees to provide the loan amount without any security interest. As a result, unsecured loans often carry higher interest rates. 3. Installment Loan Agreement: This agreement breaks down the total loan amount and interest into a series of fixed monthly payments over an agreed-upon period. It is a popular choice for borrowers who prefer a structured repayment schedule. 4. Balloon Payment Loan Agreement: This type of agreement allows borrowers to make lower monthly payments during the loan term, with a large final payment (balloon payment) due at the end. Such agreements can be useful for individuals or businesses expecting a significant amount of money in the future but need immediate access to a vehicle. In conclusion, a Delaware Loan Agreement for Vehicle is a vital legal document that safeguards the interests of both the borrower and lender when financing a vehicle purchase. By clearly defining the terms and conditions of the loan, it ensures transparency, helps prevent disputes, and provides a framework for successful repayment. Whether it is a secured or unsecured, installment or balloon payment loan agreement, it is crucial for all parties involved to carefully read and understand the terms before signing.

Delaware Loan Agreement for Vehicle

Description

How to fill out Delaware Loan Agreement For Vehicle?

If you want to total, obtain, or print lawful document templates, use US Legal Forms, the biggest assortment of lawful varieties, which can be found on-line. Take advantage of the site`s easy and hassle-free research to find the papers you need. A variety of templates for business and individual reasons are categorized by types and claims, or keywords and phrases. Use US Legal Forms to find the Delaware Loan Agreement for Vehicle in just a handful of mouse clicks.

In case you are already a US Legal Forms consumer, log in in your accounts and then click the Acquire option to obtain the Delaware Loan Agreement for Vehicle. You can also accessibility varieties you previously delivered electronically inside the My Forms tab of the accounts.

If you are using US Legal Forms the very first time, refer to the instructions listed below:

- Step 1. Be sure you have selected the form for the proper town/country.

- Step 2. Use the Review solution to examine the form`s information. Don`t forget about to see the description.

- Step 3. In case you are not happy using the develop, utilize the Look for field towards the top of the monitor to get other variations of the lawful develop web template.

- Step 4. After you have located the form you need, select the Acquire now option. Pick the pricing prepare you favor and add your qualifications to sign up to have an accounts.

- Step 5. Procedure the deal. You may use your Мisa or Ьastercard or PayPal accounts to finish the deal.

- Step 6. Pick the file format of the lawful develop and obtain it on your own system.

- Step 7. Total, revise and print or indication the Delaware Loan Agreement for Vehicle.

Every single lawful document web template you buy is your own property for a long time. You may have acces to each develop you delivered electronically inside your acccount. Click the My Forms segment and select a develop to print or obtain once more.

Compete and obtain, and print the Delaware Loan Agreement for Vehicle with US Legal Forms. There are thousands of professional and state-certain varieties you can utilize to your business or individual requirements.