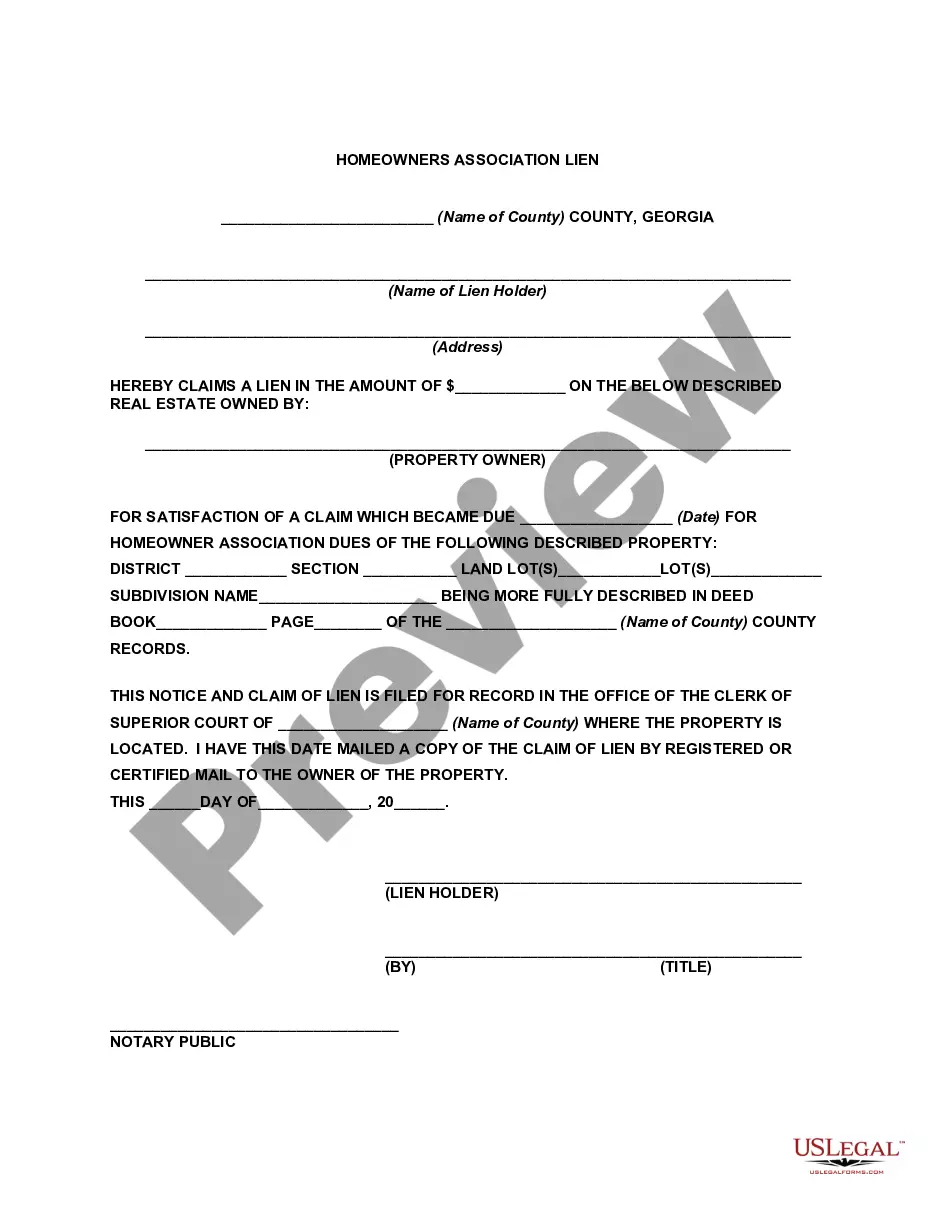

If you live in a mandatory homeowner association you probably pay annual dues, also called annual assessments. These dues help pay for such things as; maintenance of the common facilities, and professional services (including accountants, attorneys, and management companies). It is also prudent for an association to establish a reserve account to be used for large future expenditures, such as resurfacing the pool. The provisions for paying annual dues are contained in the Declaration of Covenants for your association. The Declaration of Covenants is filed on the deed records in your county's Superior Court. You automatically agreed to the terms of these covenants by purchasing your home.

The amount of the annual dues or "assessment" is determined each year by the Board of the Association. To protect the interests of both the homeowners and their lenders, the covenants often establish a maximum assessment based on the anticipated costs for maintaining the community. Usually, this maximum cannot be exceeded without a vote from the membership, but some covenants allow the Board to increase this amount each year by a specific percentage, or in step with the Consumer Price Index.

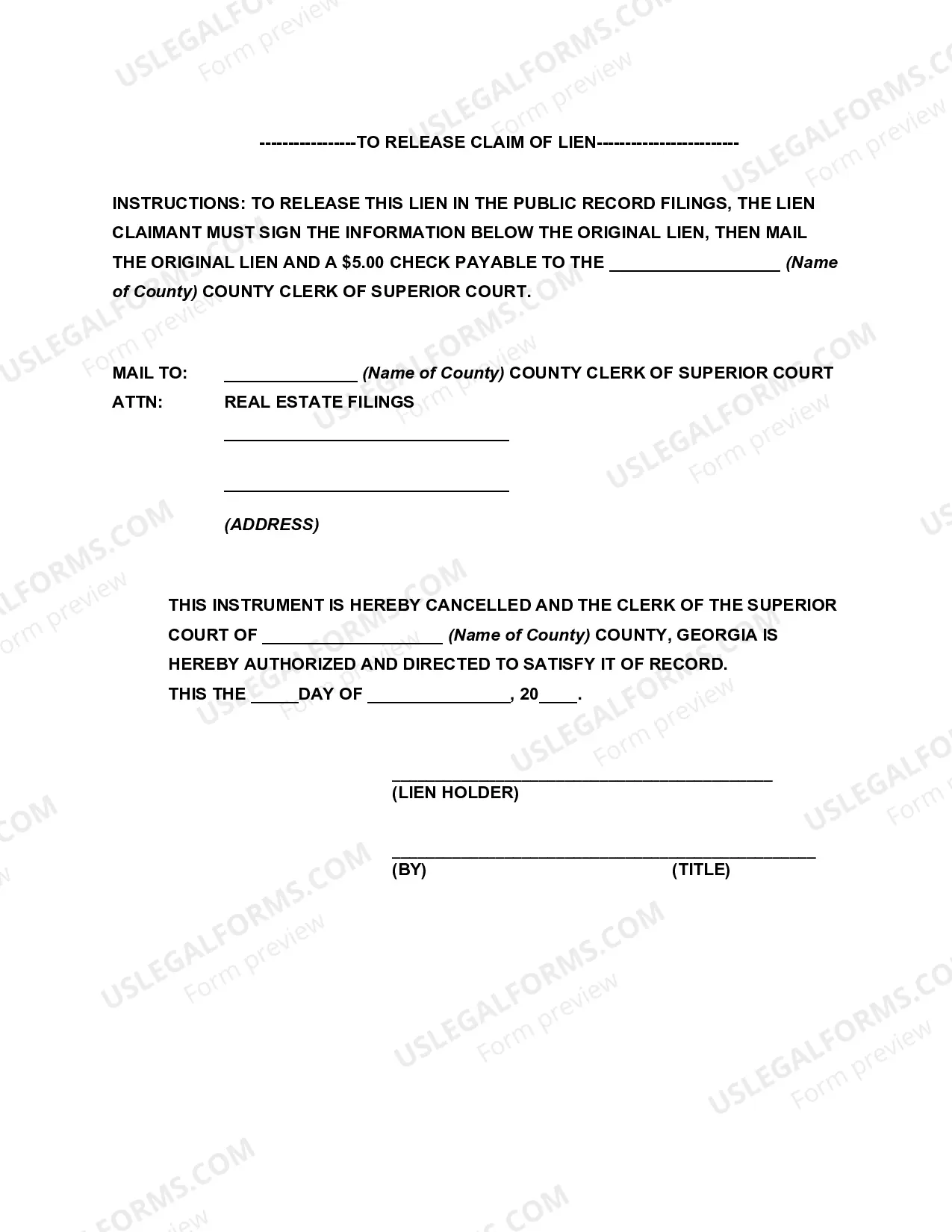

If a homeowner does not pay the dues, most covenants state that the association may charge a late fee and interest. In addition, a lien can be filed on the property called an "Assessment Lien." This lien may contain extra costs including recording fees, cancellation fees, and attorney fees. It is not necessary to institute suit in order to file the lien.