The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

Georgia Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is a type of financing option that is not governed by the regulations set forth in the federal law. This type of installment sale allows individuals and businesses in Georgia to enter into an agreement for the purchase of goods or services, with the repayment being made through scheduled installments. One example of Georgia Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is the sale of real estate properties. When a property is sold using an installment sale agreement, the buyer agrees to make regular payments to the seller over a predetermined period of time, typically with interest. The property acts as collateral, providing security for the seller in case of default. Another type of Georgia Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is the sale of vehicles. In this case, individuals or businesses can purchase a vehicle through an installment sale agreement, with the buyer making regular payments until the full purchase price, along with any interest, is paid off. The vehicle serves as collateral, ensuring the seller's interests are protected. Other examples of installment sales not covered by the Federal Consumer Credit Protection Act with Security Agreement in Georgia include the sale of furniture, appliances, electronics, and other consumer goods. These types of transactions allow buyers to acquire goods immediately while spreading out the payments over time, often with interest. It is important to note that while these Georgia Installment Sales are not covered by the federal law, Georgia may have its own regulations and laws to protect consumers in such transactions. It is advisable for buyers and sellers to familiarize themselves with the applicable state laws, including any disclosure requirements, interest rate limits, and remedies available in case of default. In summary, a Georgia Installment Sale not covered by the Federal Consumer Credit Protection Act with Security Agreement refers to various types of transactions in which buyers make regular payments over time for the purchase of goods or services, with security provided through collateral. Real estate, vehicles, and consumer goods are common examples of installment sales in Georgia that fall outside the scope of federal regulations.Georgia Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is a type of financing option that is not governed by the regulations set forth in the federal law. This type of installment sale allows individuals and businesses in Georgia to enter into an agreement for the purchase of goods or services, with the repayment being made through scheduled installments. One example of Georgia Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is the sale of real estate properties. When a property is sold using an installment sale agreement, the buyer agrees to make regular payments to the seller over a predetermined period of time, typically with interest. The property acts as collateral, providing security for the seller in case of default. Another type of Georgia Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement is the sale of vehicles. In this case, individuals or businesses can purchase a vehicle through an installment sale agreement, with the buyer making regular payments until the full purchase price, along with any interest, is paid off. The vehicle serves as collateral, ensuring the seller's interests are protected. Other examples of installment sales not covered by the Federal Consumer Credit Protection Act with Security Agreement in Georgia include the sale of furniture, appliances, electronics, and other consumer goods. These types of transactions allow buyers to acquire goods immediately while spreading out the payments over time, often with interest. It is important to note that while these Georgia Installment Sales are not covered by the federal law, Georgia may have its own regulations and laws to protect consumers in such transactions. It is advisable for buyers and sellers to familiarize themselves with the applicable state laws, including any disclosure requirements, interest rate limits, and remedies available in case of default. In summary, a Georgia Installment Sale not covered by the Federal Consumer Credit Protection Act with Security Agreement refers to various types of transactions in which buyers make regular payments over time for the purchase of goods or services, with security provided through collateral. Real estate, vehicles, and consumer goods are common examples of installment sales in Georgia that fall outside the scope of federal regulations.

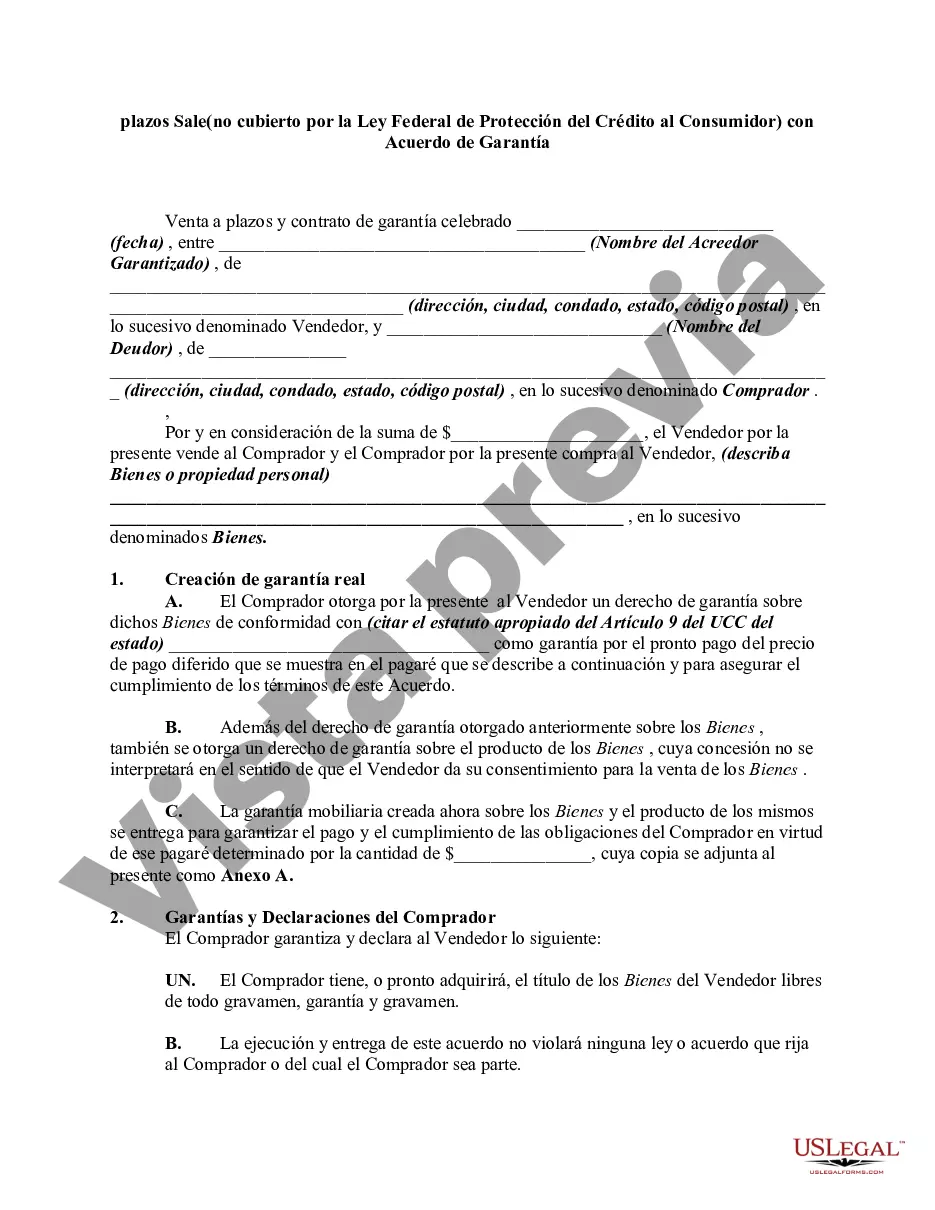

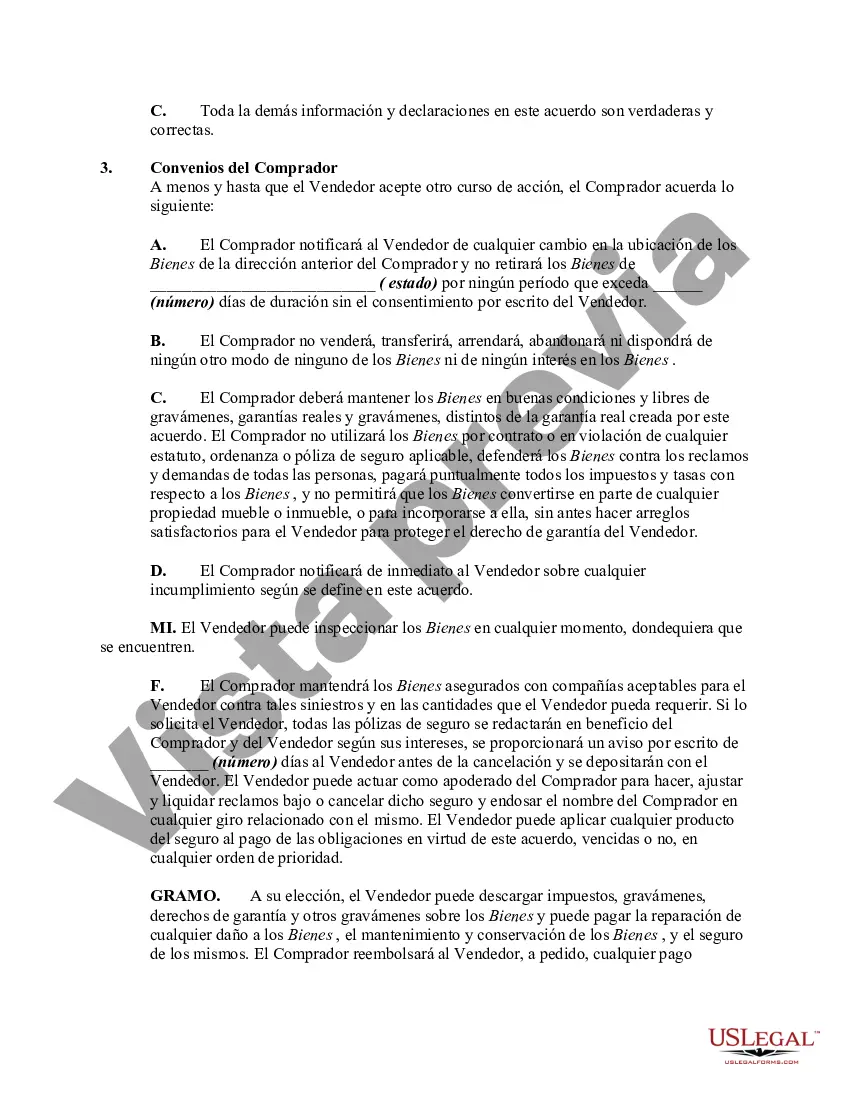

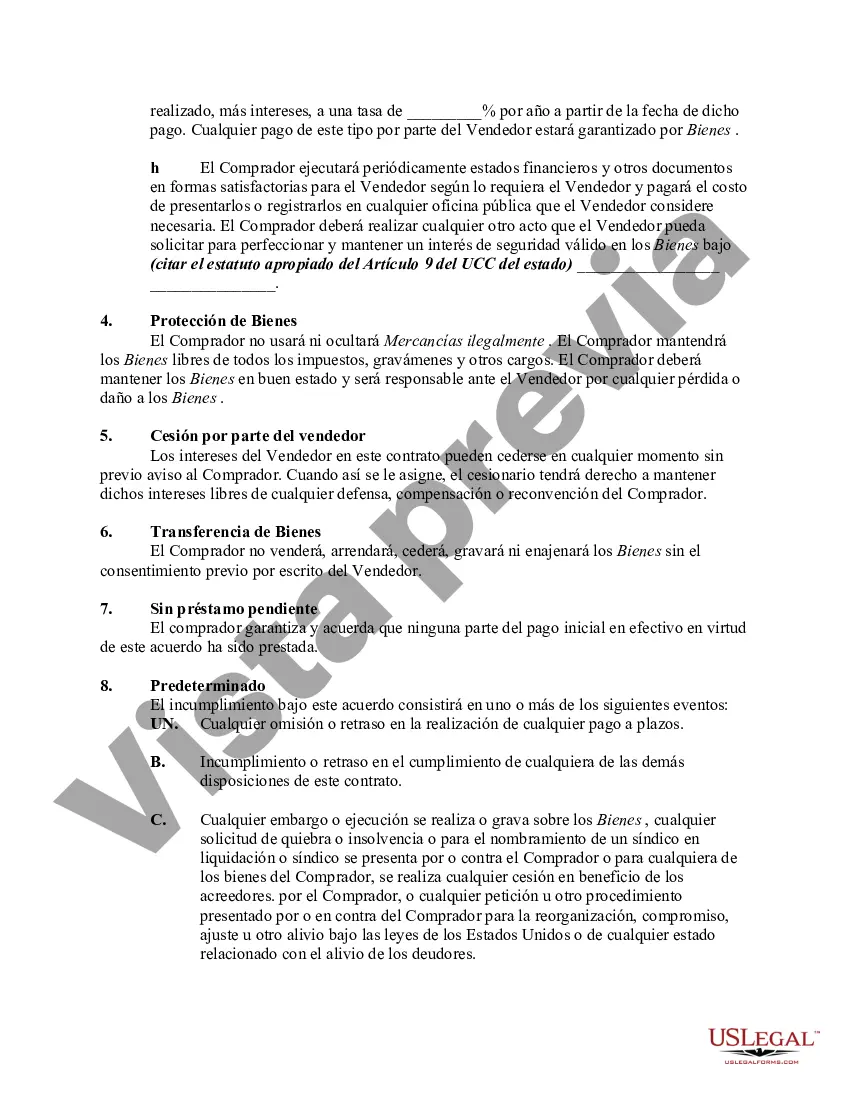

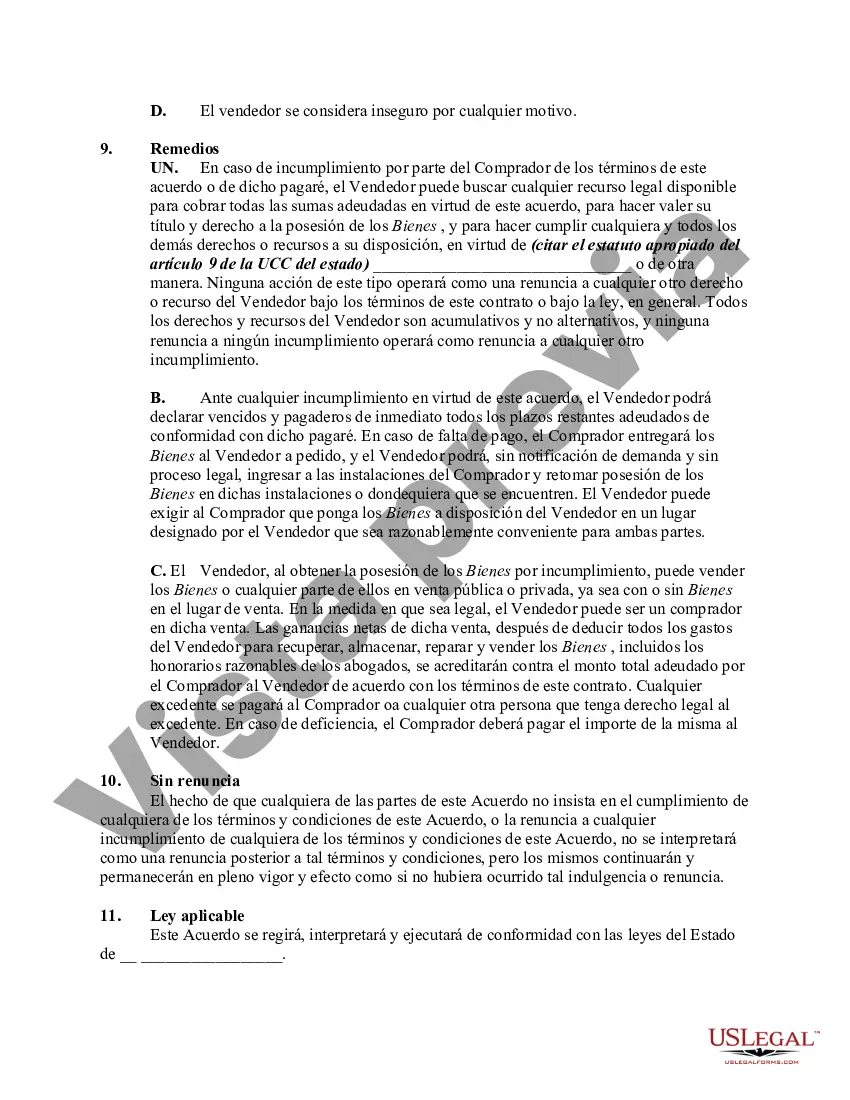

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.