As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

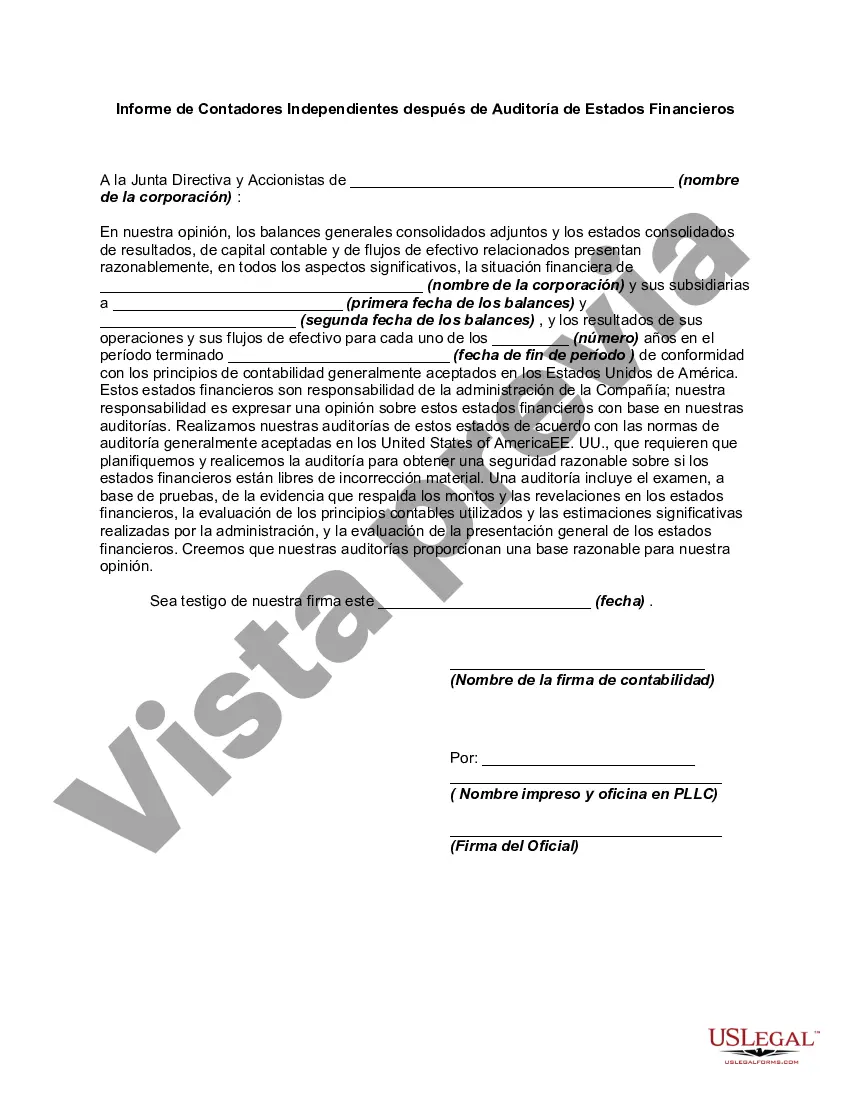

Title: Hawaii Report of Independent Accountants after Audit of Financial Statements: A Comprehensive Overview Introduction: Hawaii Report of Independent Accountants after Audit of Financial Statements is a crucial document that provides a comprehensive evaluation of an organization's financial statements. This report is prepared by independent accountants to ensure transparency, accuracy, and compliance with accounting standards. In this article, we will delve into the details of Hawaii's Report of Independent Accountants after Audit of Financial Statements, including its importance, general content, and different types. I. Importance of Hawaii Report of Independent Accountants after Audit of Financial Statements: 1. Ensuring Accuracy and Reliability: The report ensures that financial statements accurately represent an organization's financial standing, making them reliable for decision-making by investors, stakeholders, and lenders. 2. Compliance with Accounting Standards: The report verifies compliance with applicable accounting standards, enabling organizations to identify any potential non-compliance issues. 3. Increased Transparency: By providing an independent perspective on financial statements, the report enhances transparency and promotes trust between organizations and their stakeholders. II. General Content of Hawaii Report of Independent Accountants after Audit of Financial Statements: 1. Independent Auditor's Opinion: The report begins with an auditor's opinion, providing an overall evaluation of the financial statements' fairness and compliance. 2. Firm Background: It includes information about the accounting firm performing the audit, including their name, qualifications, and independence. 3. Scope of Audit: The report outlines the scope of the audit, detailing the specific financial statements and periods covered by the audit. 4. Summary of Audit Procedures: This section summarizes the audit procedures conducted by the independent accountants, including testing of internal controls, analytical procedures, and substantive tests. 5. Significant Accounting Policies: The report describes the organization's significant accounting policies applied in the preparation of financial statements. 6. Key Findings and Adjustments: Any material findings, errors, misstatements, or adjustments discovered during the audit are disclosed in this section. 7. Compliance with Laws and Regulations: The report assesses the organization's compliance with relevant laws, regulations, and industry-specific guidelines. 8. Consolidated Financial Statements: If applicable, the report presents consolidated financial statements, including balances, income statement, cash flow statement, and statement of changes in equity. 9. Other Disclosures: The report may include additional disclosures concerning uncertainties, contingent liabilities, related party transactions, and subsequent events. III. Types of Hawaii Report of Independent Accountants after Audit of Financial Statements: 1. Unqualified Opinion: This type of report is issued when the financial statements are fairly presented and comply with accounting standards. 2. Qualified Opinion: A qualified opinion is issued when the financial statements contain material misstatements or the organization's compliance with accounting standards requires adjustments. 3. Adverse Opinion: An adverse opinion is given if the financial statements are not presented fairly or do not comply with accounting standards to a significant extent. 4. Disclaimer of Opinion: In rare cases, when auditors cannot express an opinion due to limitations imposed or insufficient evidence, a disclaimer of opinion is given. Conclusion: The Hawaii Report of Independent Accountants after Audit of Financial Statements serves as a crucial document in assessing an organization's financial health and compliance. By providing an independent review, it helps stakeholders make informed decisions. Understanding the general content and different types of such reports is essential for organizations and individuals seeking transparency and credibility in financial reporting.Title: Hawaii Report of Independent Accountants after Audit of Financial Statements: A Comprehensive Overview Introduction: Hawaii Report of Independent Accountants after Audit of Financial Statements is a crucial document that provides a comprehensive evaluation of an organization's financial statements. This report is prepared by independent accountants to ensure transparency, accuracy, and compliance with accounting standards. In this article, we will delve into the details of Hawaii's Report of Independent Accountants after Audit of Financial Statements, including its importance, general content, and different types. I. Importance of Hawaii Report of Independent Accountants after Audit of Financial Statements: 1. Ensuring Accuracy and Reliability: The report ensures that financial statements accurately represent an organization's financial standing, making them reliable for decision-making by investors, stakeholders, and lenders. 2. Compliance with Accounting Standards: The report verifies compliance with applicable accounting standards, enabling organizations to identify any potential non-compliance issues. 3. Increased Transparency: By providing an independent perspective on financial statements, the report enhances transparency and promotes trust between organizations and their stakeholders. II. General Content of Hawaii Report of Independent Accountants after Audit of Financial Statements: 1. Independent Auditor's Opinion: The report begins with an auditor's opinion, providing an overall evaluation of the financial statements' fairness and compliance. 2. Firm Background: It includes information about the accounting firm performing the audit, including their name, qualifications, and independence. 3. Scope of Audit: The report outlines the scope of the audit, detailing the specific financial statements and periods covered by the audit. 4. Summary of Audit Procedures: This section summarizes the audit procedures conducted by the independent accountants, including testing of internal controls, analytical procedures, and substantive tests. 5. Significant Accounting Policies: The report describes the organization's significant accounting policies applied in the preparation of financial statements. 6. Key Findings and Adjustments: Any material findings, errors, misstatements, or adjustments discovered during the audit are disclosed in this section. 7. Compliance with Laws and Regulations: The report assesses the organization's compliance with relevant laws, regulations, and industry-specific guidelines. 8. Consolidated Financial Statements: If applicable, the report presents consolidated financial statements, including balances, income statement, cash flow statement, and statement of changes in equity. 9. Other Disclosures: The report may include additional disclosures concerning uncertainties, contingent liabilities, related party transactions, and subsequent events. III. Types of Hawaii Report of Independent Accountants after Audit of Financial Statements: 1. Unqualified Opinion: This type of report is issued when the financial statements are fairly presented and comply with accounting standards. 2. Qualified Opinion: A qualified opinion is issued when the financial statements contain material misstatements or the organization's compliance with accounting standards requires adjustments. 3. Adverse Opinion: An adverse opinion is given if the financial statements are not presented fairly or do not comply with accounting standards to a significant extent. 4. Disclaimer of Opinion: In rare cases, when auditors cannot express an opinion due to limitations imposed or insufficient evidence, a disclaimer of opinion is given. Conclusion: The Hawaii Report of Independent Accountants after Audit of Financial Statements serves as a crucial document in assessing an organization's financial health and compliance. By providing an independent review, it helps stakeholders make informed decisions. Understanding the general content and different types of such reports is essential for organizations and individuals seeking transparency and credibility in financial reporting.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.