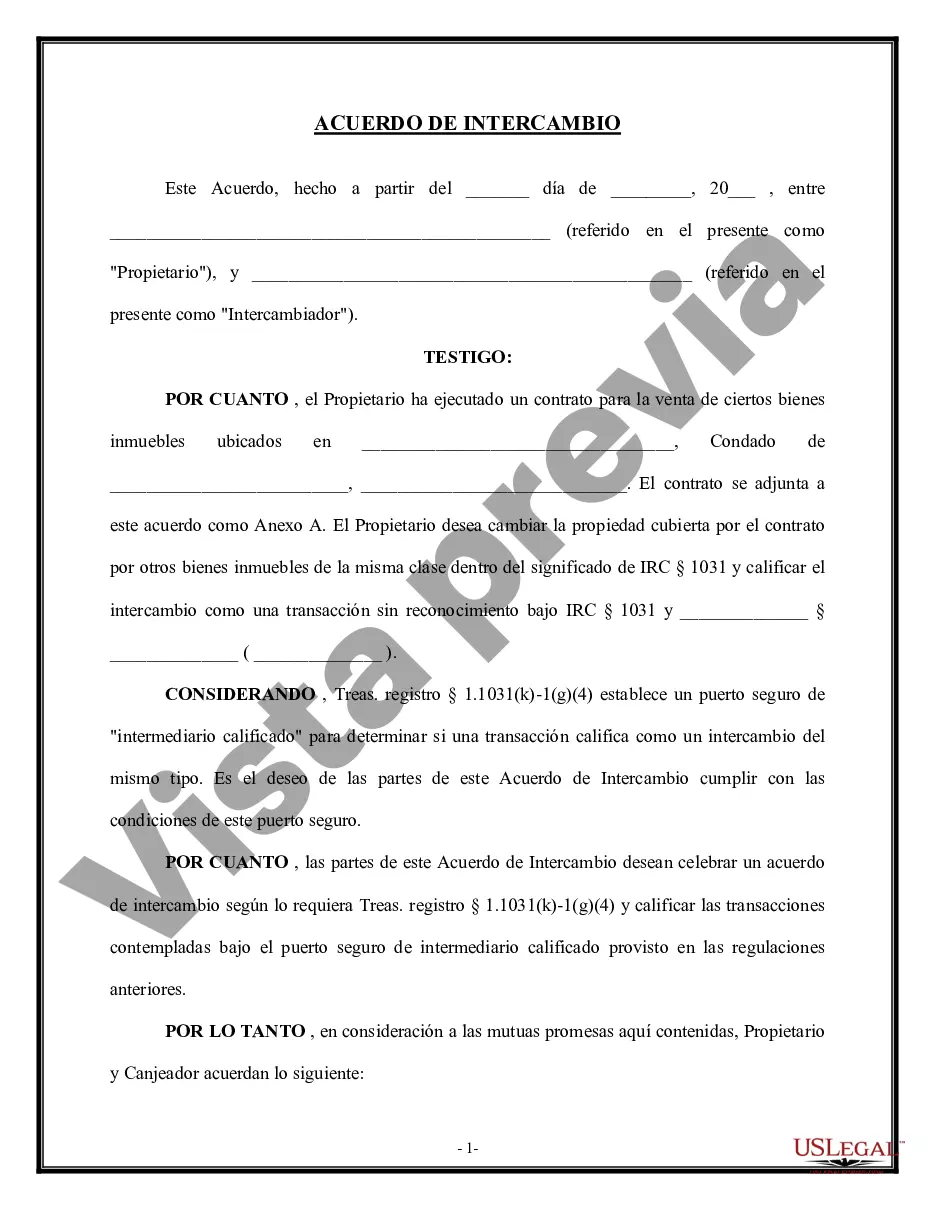

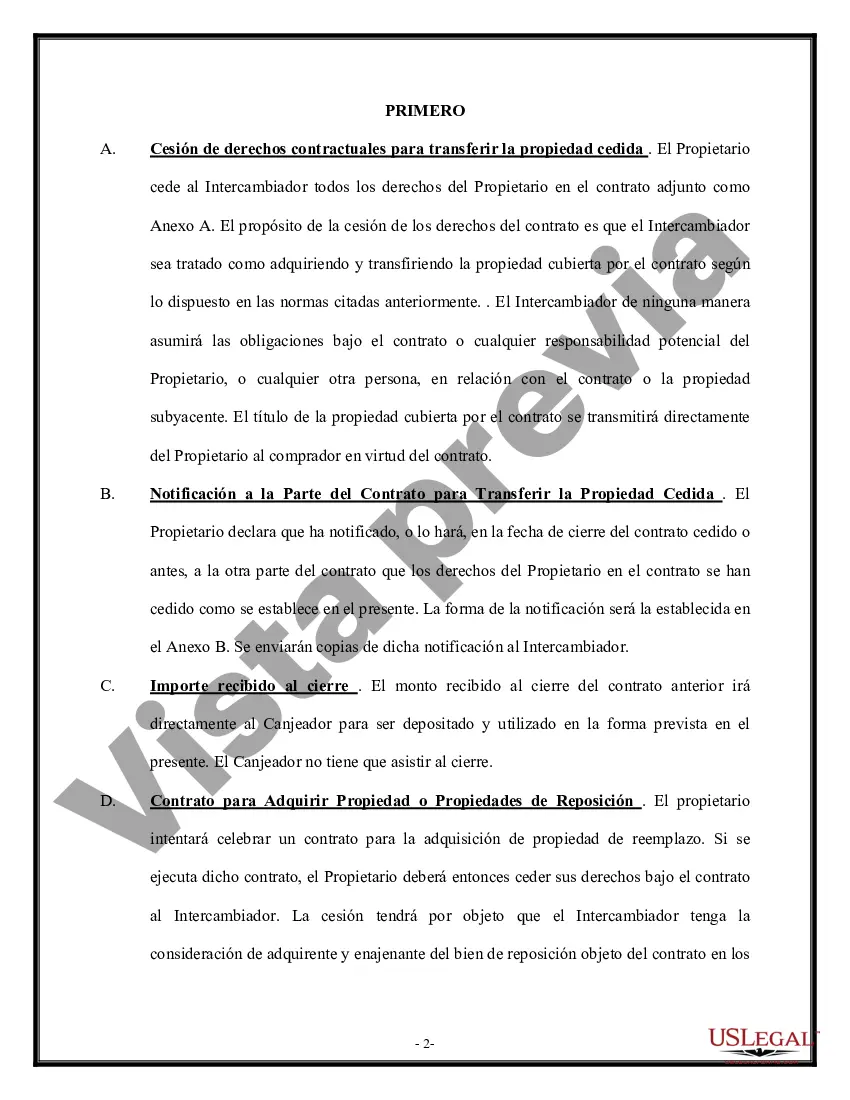

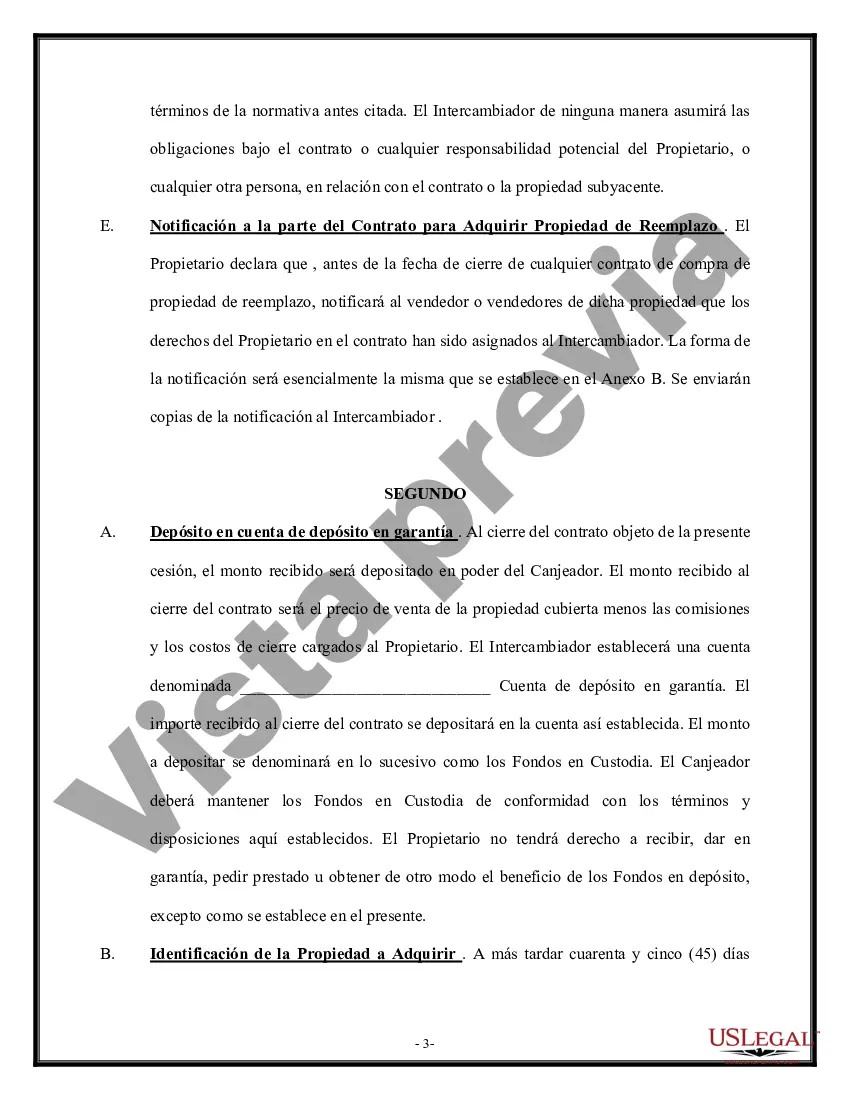

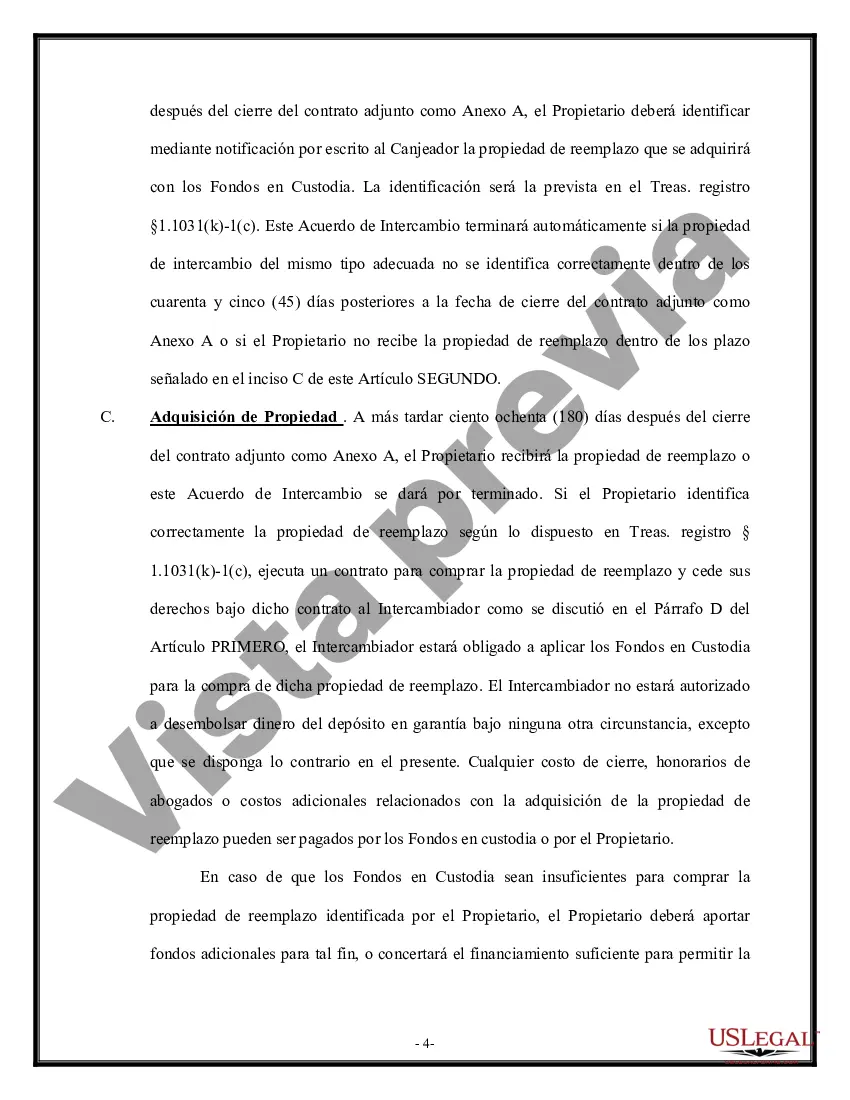

Illinois Tax Free Exchange Agreement Section 1031, also known as a 1031 exchange, is a provision within the Illinois tax code that allows individuals or businesses to defer the payment of capital gains taxes on the sale of certain qualifying properties. This provision is based on the federal tax code section 1031, which allows for tax-free exchanges of similar properties. Under the Illinois Tax Free Exchange Agreement Section 1031, individuals or businesses can sell an investment property and reinvest the proceeds into a like-kind property, thus deferring the capital gains tax that would normally be due upon the sale. This provision is particularly beneficial for real estate investors or businesses looking to sell and reinvest in similar properties, without incurring immediate tax liabilities. To qualify for the Illinois Tax Free Exchange Agreement Section 1031, the property being sold and the property being acquired must be held for investment or for productive use in a trade or business. Like-kind refers to properties that are of the same nature or character, regardless of differences in quality or grade. For example, an individual can exchange a residential rental property for a commercial property, or vice versa, and still qualify for the tax deferral. It is important to note that not all types of exchanges are eligible for tax deferral under Section 1031 of the Illinois tax code. Some types of exchanges specifically excluded from qualification include exchanges of personal residences or vacation homes. Additionally, exchanges involving inventory, stocks, bonds, or partnership interests do not qualify for tax deferral. There are different types of exchanges that fall under the Illinois Tax Free Exchange Agreement Section 1031, including simultaneous exchanges, delayed exchanges, and reverse exchanges. 1. Simultaneous Exchange: This type of exchange requires the transfer of the relinquished property (property being sold) and the acquisition of the replacement property to occur at the same time, often with the help of a qualified intermediary. 2. Delayed Exchange: In a delayed exchange, the taxpayer sells the relinquished property first and then has a specific timeframe (usually 180 days) to identify and acquire the replacement property. This is the most common type of 1031 exchange. 3. Reverse Exchange: A reverse exchange involves the acquisition of the replacement property before the sale of the relinquished property. This type of exchange requires the use of an Exchange Accommodation Titleholder (EAT) and is more complex and less commonly used than other types of exchanges. Overall, the Illinois Tax Free Exchange Agreement Section 1031 provides individuals and businesses with a valuable tax planning tool to defer capital gains taxes on the sale of investment properties. However, it is crucial for taxpayers to consult with tax professionals and adhere to the specific requirements and timelines outlined in the tax code to ensure compliance and maximize the benefits of this provision.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Illinois Acuerdo de Intercambio Libre de Impuestos Sección 1031 - Tax Free Exchange Agreement Section 1031

Description

How to fill out Illinois Acuerdo De Intercambio Libre De Impuestos Sección 1031?

Choosing the right legal record format could be a have difficulties. Needless to say, there are a lot of templates available on the net, but how do you discover the legal type you want? Take advantage of the US Legal Forms web site. The support gives a huge number of templates, including the Illinois Tax Free Exchange Agreement Section 1031, which can be used for enterprise and private requires. Each of the types are checked by professionals and meet state and federal demands.

When you are previously registered, log in in your account and then click the Obtain switch to have the Illinois Tax Free Exchange Agreement Section 1031. Make use of account to appear from the legal types you possess acquired formerly. Check out the My Forms tab of your account and get another version in the record you want.

When you are a new customer of US Legal Forms, listed below are straightforward instructions that you can follow:

- Initially, ensure you have selected the proper type for the metropolis/state. You may check out the form utilizing the Preview switch and study the form explanation to ensure it is the right one for you.

- When the type does not meet your expectations, take advantage of the Seach area to discover the correct type.

- Once you are sure that the form is acceptable, go through the Buy now switch to have the type.

- Pick the rates strategy you want and enter in the essential info. Build your account and pay for an order making use of your PayPal account or charge card.

- Choose the document formatting and download the legal record format in your product.

- Comprehensive, modify and print and indication the received Illinois Tax Free Exchange Agreement Section 1031.

US Legal Forms is definitely the biggest local library of legal types that you can find different record templates. Take advantage of the company to download professionally-created paperwork that follow status demands.