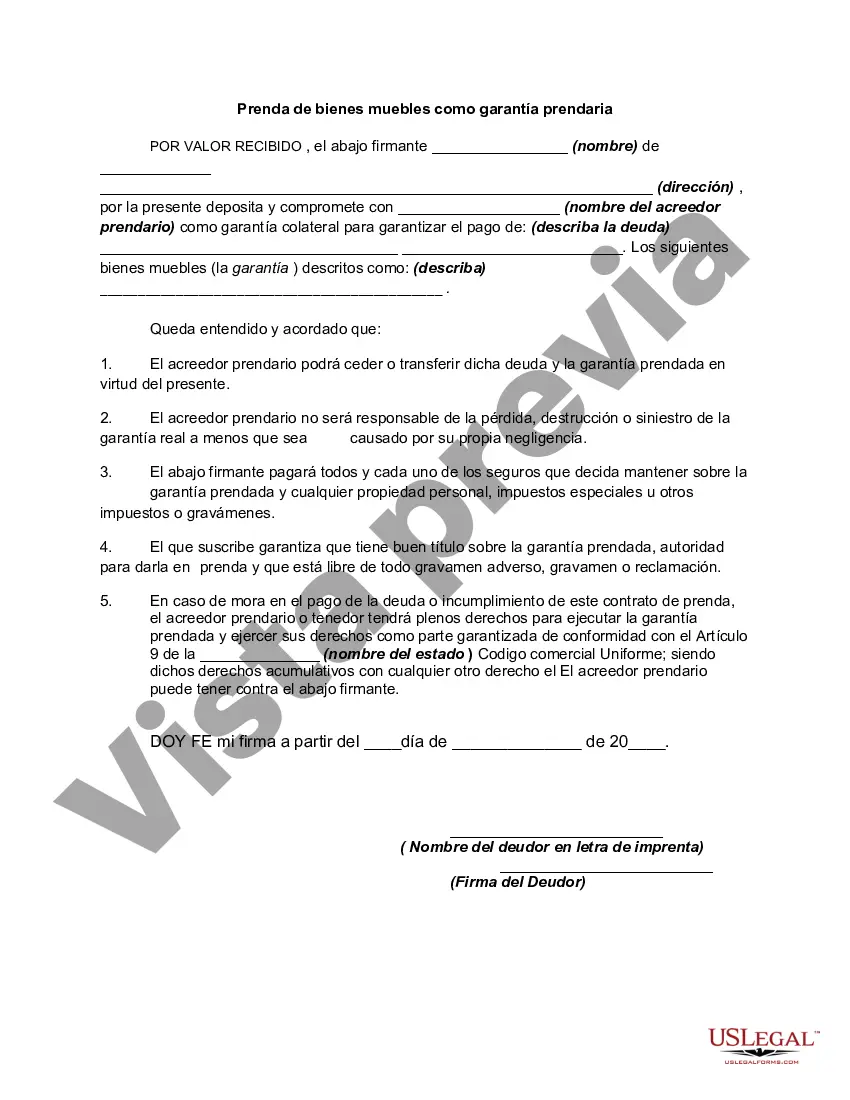

The Illinois Pledge of Personal Property as Collateral Security is a legal mechanism that allows individuals or businesses to use their personal property as collateral when securing a loan or debt. This pledge acts as a form of security, ensuring that in the event of default or non-payment, the lender has a right to seize and sell the pledged property to recover the outstanding debt. In Illinois, there are different types of pledges of personal property as collateral security, each with its own set of guidelines and rules. Some common types include: 1. Traditional Pledge: This basic form of pledge involves the borrower offering personal property, such as vehicles, equipment, inventory, or even financial investments, as collateral security for a loan. 2. Deposit Account Control Agreement: This type of pledge involves the borrower granting the lender control over a deposit account in order to secure a loan. It allows the lender to directly access the funds in the account in case of default. 3. Chattel Mortgage: In a chattel mortgage, the borrower pledges personal property assets to secure a loan. This often applies to movable property, such as machinery, vehicles, or equipment, and involves the transfer of ownership rights to the lender until the loan is fully repaid. 4. UCC-1 Financing Statement: The Uniform Commercial Code (UCC) 1 financing statement is a widely used legal document that creates a security interest in personal property. It is filed with the Illinois Secretary of State's office to provide public notice of the lender's interest in the pledged property. The Illinois Pledge of Personal Property as Collateral Security is governed by various laws and regulations such as the Illinois Commercial Code and the Uniform Commercial Code Article 9. It is important for both lenders and borrowers to understand these laws and comply with all necessary requirements when entering into a pledge agreement. The pledge of personal property offers lenders a level of assurance and protection in the event of default, as they have a legal claim on the pledged assets. From the borrower's perspective, it provides an opportunity to access financing by leveraging their personal property. Before entering into any pledge agreement, it is advisable for both parties to seek legal advice to ensure compliance with all relevant regulations and to understand their rights and obligations. Additionally, thorough valuation and documentation of the pledged assets are crucial to accurately establish their worth and facilitate smooth transaction processes.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Illinois Prenda de bienes muebles como garantía prendaria - Pledge of Personal Property as Collateral Security

Description

How to fill out Illinois Prenda De Bienes Muebles Como Garantía Prendaria?

If you have to full, down load, or print out lawful papers templates, use US Legal Forms, the greatest assortment of lawful types, that can be found on the Internet. Use the site`s easy and hassle-free research to obtain the documents you want. Different templates for company and individual functions are categorized by categories and claims, or keywords. Use US Legal Forms to obtain the Illinois Pledge of Personal Property as Collateral Security with a handful of mouse clicks.

When you are presently a US Legal Forms client, log in in your accounts and click on the Acquire switch to get the Illinois Pledge of Personal Property as Collateral Security. You may also access types you formerly saved from the My Forms tab of your respective accounts.

Should you use US Legal Forms initially, follow the instructions under:

- Step 1. Be sure you have chosen the shape for the proper area/land.

- Step 2. Use the Review choice to examine the form`s content material. Do not neglect to see the outline.

- Step 3. When you are not happy together with the develop, use the Search industry near the top of the display to locate other types of your lawful develop web template.

- Step 4. After you have located the shape you want, go through the Buy now switch. Select the rates program you like and include your qualifications to register on an accounts.

- Step 5. Approach the transaction. You can use your charge card or PayPal accounts to finish the transaction.

- Step 6. Pick the format of your lawful develop and down load it on the gadget.

- Step 7. Complete, change and print out or sign the Illinois Pledge of Personal Property as Collateral Security.

Each and every lawful papers web template you get is the one you have forever. You might have acces to each develop you saved inside your acccount. Go through the My Forms section and select a develop to print out or down load once again.

Compete and down load, and print out the Illinois Pledge of Personal Property as Collateral Security with US Legal Forms. There are thousands of professional and state-particular types you may use to your company or individual demands.