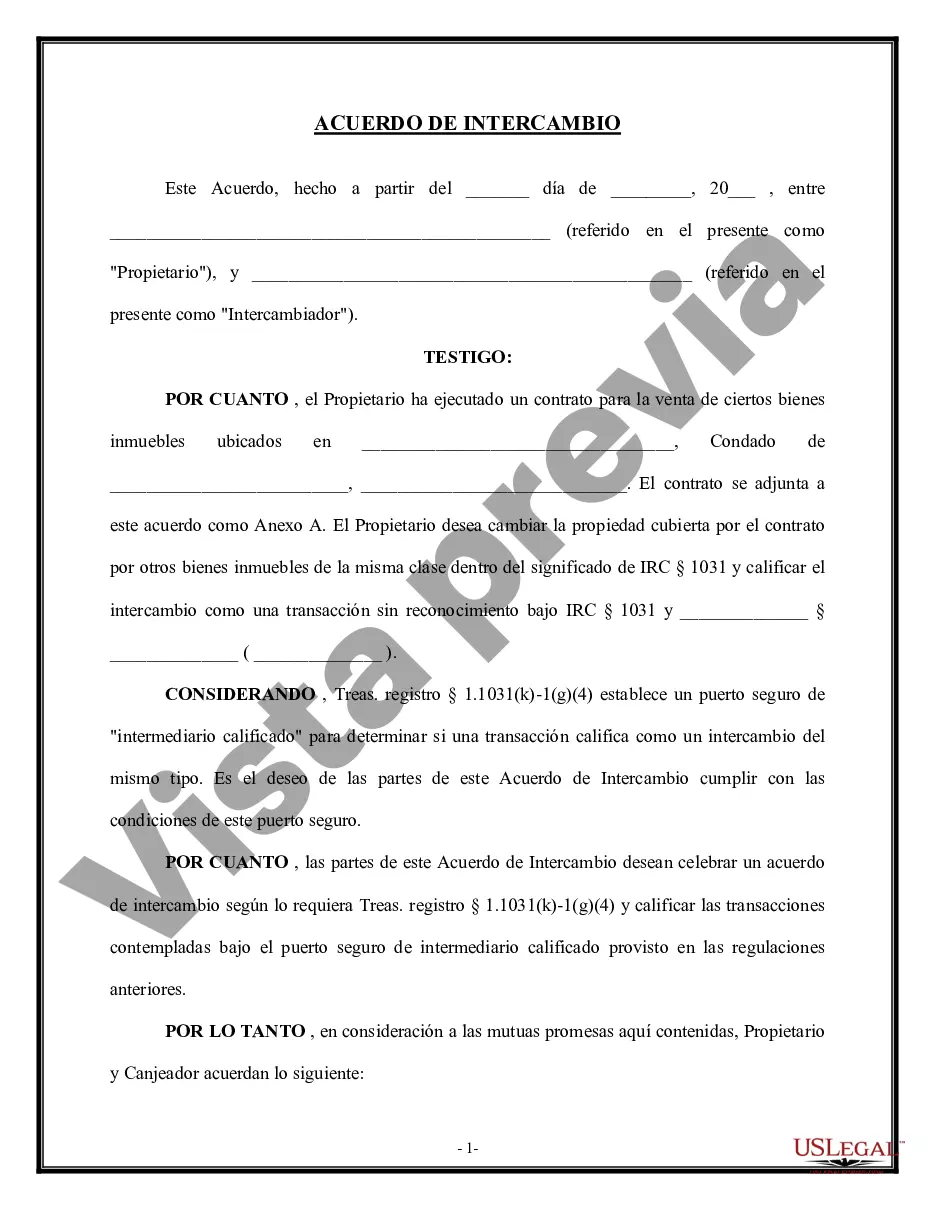

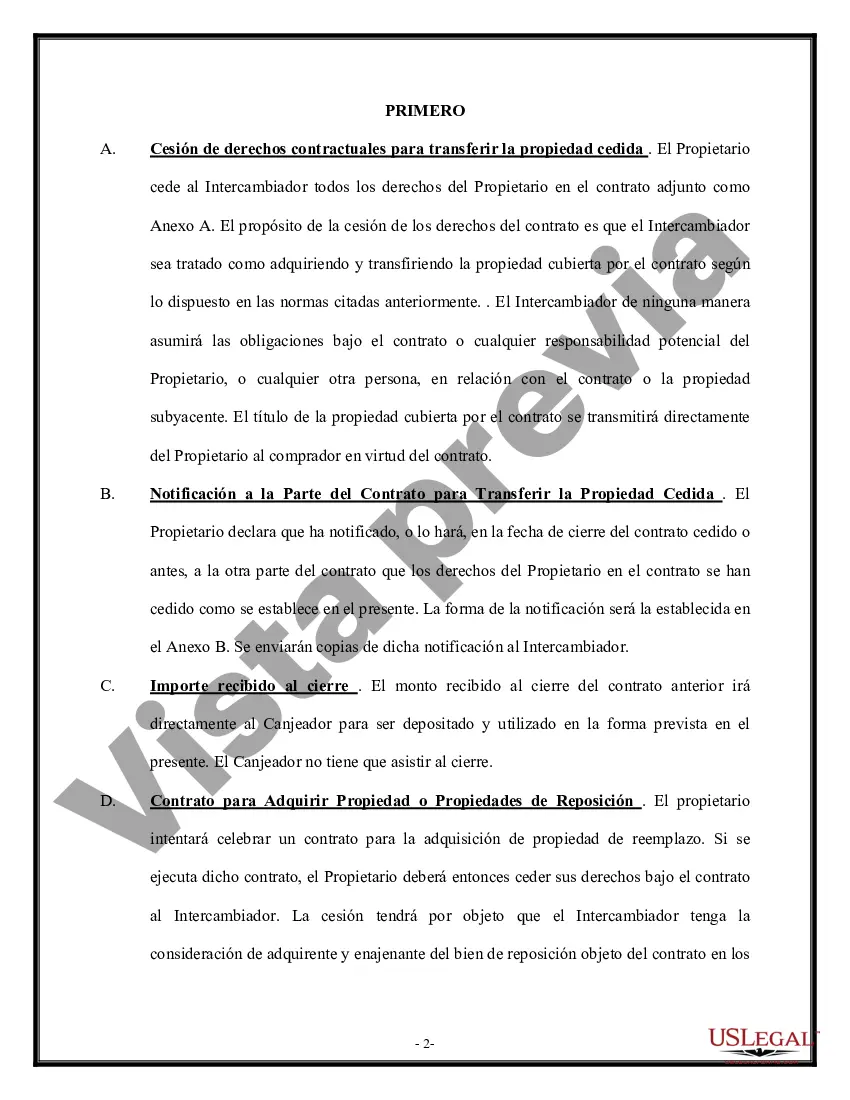

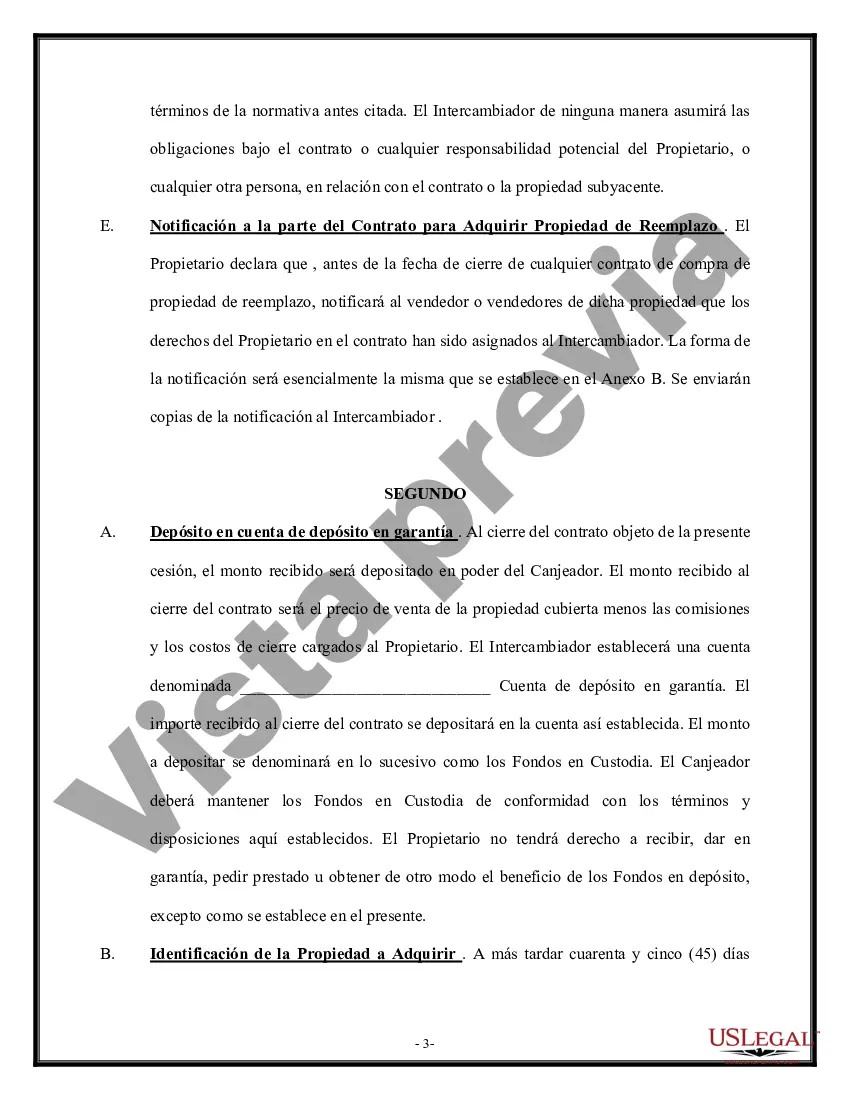

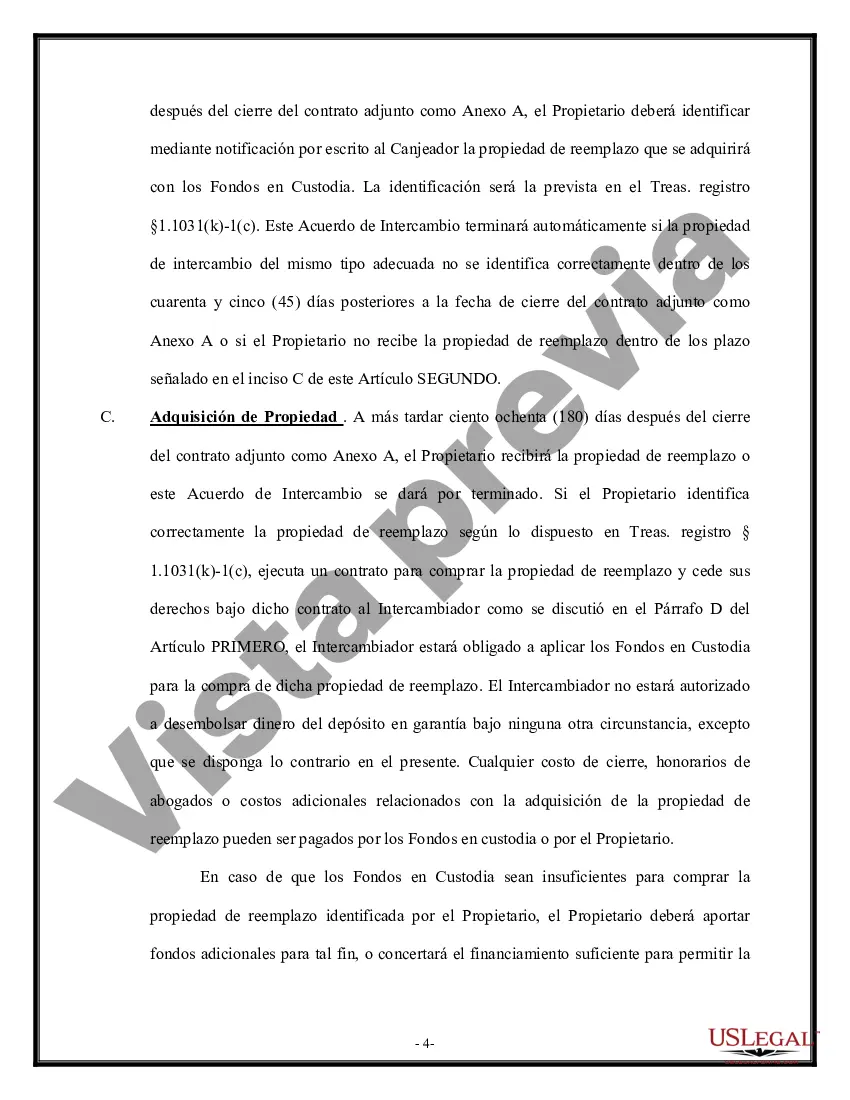

The Indiana Tax Free Exchange Agreement Section 1031 is a provision in the Indiana tax code that allows individuals and businesses to defer capital gains tax when exchanging certain types of property for like-kind property. This provision is based on section 1031 of the Internal Revenue Code (IRC), which applies to all states. Under the Indiana Tax Free Exchange Agreement Section 1031, individuals and businesses can sell investment or business property and reinvest the proceeds in a similar or "like-kind" property without incurring immediate capital gains tax. By deferring the tax, investors can retain more capital to invest in new properties, helping to stimulate economic growth and reinvestment in the local community. To qualify for the Indiana Tax Free Exchange Agreement Section 1031, certain criteria must be met. The properties involved in the exchange must be held for investment, business, or productive use, and must be of like-kind. Like-kind property refers to properties that are similar in nature or character, regardless of the differences in quality or grade. There are also time restrictions within the Indiana Tax Free Exchange Agreement Section 1031. The taxpayer must identify potential replacement properties within 45 days of selling the original property and complete the exchange by acquiring the replacement property within 180 days. It is important to note that not all property exchanges qualify for tax deferral under the Indiana Tax Free Exchange Agreement Section 1031. Exchanges involving personal residences, inventory properties, or property held primarily for sale are generally not eligible for tax deferral. However, if the property meets the criteria, individuals and businesses can take advantage of the tax benefits provided by the agreement. In addition to the standard Indiana Tax Free Exchange Agreement Section 1031, there are other variations of the agreement that may be applicable in specific circumstances. These include reverse exchanges and build-to-suit exchanges. Reverse exchanges occur when an investor acquires the replacement property before selling the relinquished property. This allows investors to secure a desired property even if they haven't yet found a buyer for their existing property. Build-to-suit exchanges, on the other hand, involve the construction or improvement of the replacement property. This allows investors to use the exchange to finance the development or improvement of a property, expanding their investment opportunities. Overall, the Indiana Tax Free Exchange Agreement Section 1031 provides a valuable tool for individuals and businesses to defer capital gains tax and reinvest in like-kind properties. With various types of exchanges available under this provision, investors can create a tax-efficient plan to maximize their investment potential and contribute to the growth of Indiana's economy.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Indiana Acuerdo de Intercambio Libre de Impuestos Sección 1031 - Tax Free Exchange Agreement Section 1031

Description

How to fill out Indiana Acuerdo De Intercambio Libre De Impuestos Sección 1031?

Have you been in the placement that you need to have documents for sometimes company or individual purposes nearly every day? There are a variety of lawful record templates available online, but locating types you can rely is not straightforward. US Legal Forms offers a huge number of type templates, just like the Indiana Tax Free Exchange Agreement Section 1031, that are written to fulfill federal and state demands.

If you are presently familiar with US Legal Forms website and possess a free account, simply log in. Following that, you can obtain the Indiana Tax Free Exchange Agreement Section 1031 template.

Should you not come with an profile and want to start using US Legal Forms, follow these steps:

- Obtain the type you want and ensure it is to the proper city/state.

- Use the Review key to check the form.

- Look at the explanation to ensure that you have selected the right type.

- If the type is not what you`re trying to find, take advantage of the Search field to get the type that fits your needs and demands.

- When you get the proper type, click Acquire now.

- Select the prices prepare you would like, fill out the specified information to generate your bank account, and pay for the transaction using your PayPal or bank card.

- Decide on a practical document file format and obtain your copy.

Locate all of the record templates you possess bought in the My Forms menu. You can get a more copy of Indiana Tax Free Exchange Agreement Section 1031 any time, if needed. Just go through the needed type to obtain or print the record template.

Use US Legal Forms, by far the most extensive variety of lawful forms, to conserve some time and stay away from errors. The services offers skillfully created lawful record templates that you can use for an array of purposes. Make a free account on US Legal Forms and commence producing your daily life a little easier.