Escrow refers to a type of account in which the money, a mortgage or deed of trust, an existing promissory note secured by the real property, escrow "instructions" from both parties, an accounting of the funds and other documents necessary to complete the transaction by a date, is held by a third party, called an "escrow agent", until the conditions of an agreement are met. When the funding is complete and the deed is clear, the escrow agent will then record the deed to the buyer and deliver funds to the seller. The escrow agent or officer is an independent holder and agent for both parties who receives a fee for their services.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

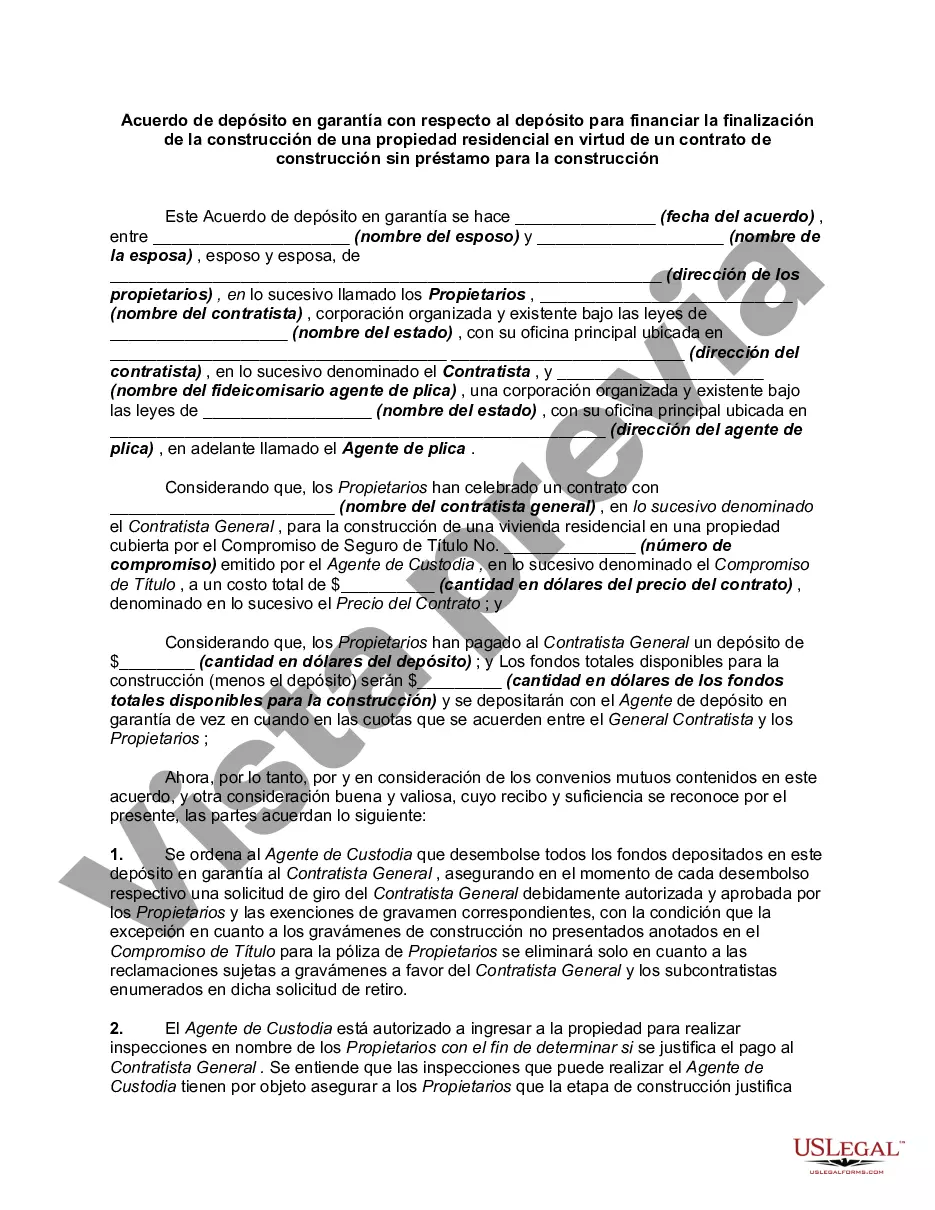

Indiana Escrow Agreement is a legally binding document that governs the use of an escrow account to fund the completion of construction on a residential property under a construction contract, in instances where no construction loan is involved. This agreement acts as a safeguard for all parties involved in the construction project, including the property owner, the contractor, and any other stakeholders. The primary purpose of an Indiana Escrow Agreement is to protect the interests of both the property owner and the contractor by ensuring that funds are properly allocated and disbursed throughout the construction process. By utilizing an escrow account, the property owner can hold the funds necessary for the completion of the project until specific construction milestones or requirements are met. One type of Indiana Escrow Agreement relating to a deposit for the completion of construction of a residential property is the "Milestone-Based Escrow Agreement." This type of agreement involves the funds being released to the contractor based on predetermined milestones or stages of completion. These milestones are typically defined in the construction contract and may include the completion of specific tasks, such as foundations, framing, plumbing, electrical work, and other significant construction aspects. Once each milestone is satisfactorily completed, the funds for that particular stage are released from the escrow account to the contractor. Another type of Indiana Escrow Agreement is the "Cost-Based Escrow Agreement." This agreement involves the disbursement of funds based on the actual costs incurred during the construction process. The property owner and the contractor agree upon the estimated cost of the entire construction project, and the escrow account holds an amount equal to that estimation. As the construction progresses, the contractor submits invoices or receipts for the materials and labor expenses incurred, and the funds are released from the escrow account accordingly. In both types of Indiana Escrow Agreements, specific conditions and requirements are outlined to protect the interests of all parties involved. These may include documentation of the construction progress, inspections, lien waivers, and any other provisions deemed necessary to ensure the successful completion of the residential property construction project. In conclusion, an Indiana Escrow Agreement regarding the deposit to fund the completion of construction on a residential property without a construction loan is crucial for safeguarding the interests of all parties involved. By utilizing either a milestone-based or cost-based escrow agreement, the property owner and the contractor can ensure proper allocation and disbursement of funds to successfully complete the construction project.Indiana Escrow Agreement is a legally binding document that governs the use of an escrow account to fund the completion of construction on a residential property under a construction contract, in instances where no construction loan is involved. This agreement acts as a safeguard for all parties involved in the construction project, including the property owner, the contractor, and any other stakeholders. The primary purpose of an Indiana Escrow Agreement is to protect the interests of both the property owner and the contractor by ensuring that funds are properly allocated and disbursed throughout the construction process. By utilizing an escrow account, the property owner can hold the funds necessary for the completion of the project until specific construction milestones or requirements are met. One type of Indiana Escrow Agreement relating to a deposit for the completion of construction of a residential property is the "Milestone-Based Escrow Agreement." This type of agreement involves the funds being released to the contractor based on predetermined milestones or stages of completion. These milestones are typically defined in the construction contract and may include the completion of specific tasks, such as foundations, framing, plumbing, electrical work, and other significant construction aspects. Once each milestone is satisfactorily completed, the funds for that particular stage are released from the escrow account to the contractor. Another type of Indiana Escrow Agreement is the "Cost-Based Escrow Agreement." This agreement involves the disbursement of funds based on the actual costs incurred during the construction process. The property owner and the contractor agree upon the estimated cost of the entire construction project, and the escrow account holds an amount equal to that estimation. As the construction progresses, the contractor submits invoices or receipts for the materials and labor expenses incurred, and the funds are released from the escrow account accordingly. In both types of Indiana Escrow Agreements, specific conditions and requirements are outlined to protect the interests of all parties involved. These may include documentation of the construction progress, inspections, lien waivers, and any other provisions deemed necessary to ensure the successful completion of the residential property construction project. In conclusion, an Indiana Escrow Agreement regarding the deposit to fund the completion of construction on a residential property without a construction loan is crucial for safeguarding the interests of all parties involved. By utilizing either a milestone-based or cost-based escrow agreement, the property owner and the contractor can ensure proper allocation and disbursement of funds to successfully complete the construction project.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.