The Indiana Profit-Sharing Plan and Trust Agreement is a legal document that outlines the terms and conditions governing the establishment and administration of a profit-sharing plan in the state of Indiana. This agreement is designed to provide employees with a share in the profits of their employer's business, fostering a sense of ownership and incentivizing productivity. The Indiana Profit-Sharing Plan and Trust Agreement typically includes provisions related to eligibility requirements, contribution limits, vesting schedules, participant benefits, and plan administration. Employers have the flexibility to tailor the terms of the agreement to meet the specific needs of their business and employees. There are several types of profit-sharing plans that can be established under the Indiana Profit-Sharing Plan and Trust Agreement. These include: 1. Basic Profit-Sharing Plan: This type of plan is the most common and straightforward. It allows employers to allocate a portion of the company's profits to eligible employees in the form of contributions to a trust account. 2. 401(k) Profit-Sharing Plan: This plan combines the features of a profit-sharing plan with a 401(k) retirement savings plan. It allows employees to contribute a portion of their pre-tax income to the plan and receive employer-matching contributions based on the company's profits. 3. Integrated Profit-Sharing Plan: This plan is designed to coordinate with Social Security benefits. Employers can contribute additional benefits to the plan based on a formula that takes into account the Social Security benefits received by eligible employees. 4. Age-Weighted Profit-Sharing Plan: This plan allows employers to allocate a higher percentage of the company's profits to older employees who are closer to retirement. It takes into account the employee's age and years of service to determine the allocated benefits. 5. New Comparability Profit-Sharing Plan: This plan is structured to provide varying contribution levels to different groups of employees based on predetermined classifications. Employers can allocate higher contribution percentages to certain employees, such as executives or highly compensated individuals. It is crucial for employers to consult with legal and financial professionals when establishing an Indiana Profit-Sharing Plan and Trust Agreement to ensure compliance with state and federal regulations. By implementing a profit-sharing plan, employers can promote employee engagement, attract and retain top talent, and contribute to the overall financial well-being of their workforce.

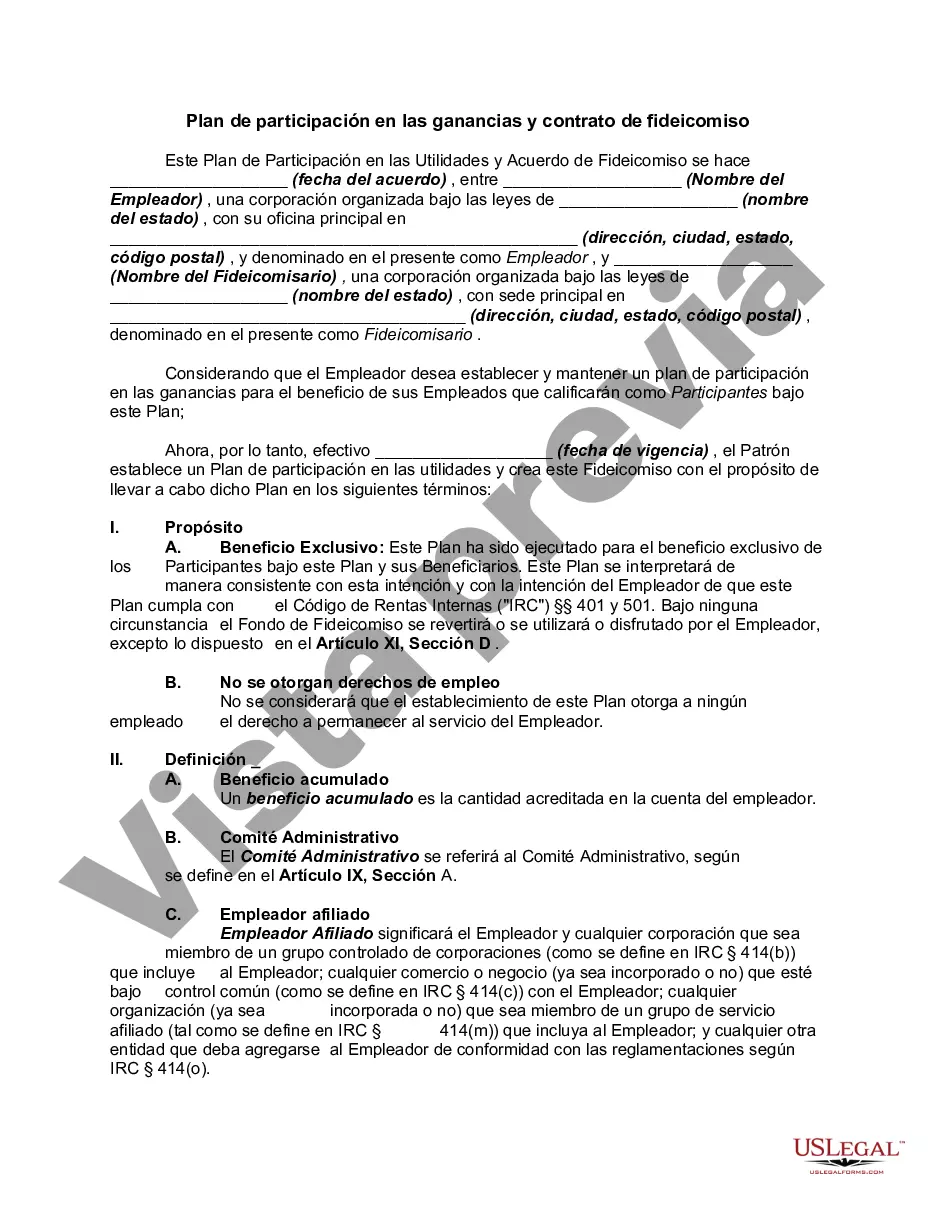

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Indiana Plan de participación en las ganancias y contrato de fideicomiso - Profit-Sharing Plan and Trust Agreement

Description

How to fill out Indiana Plan De Participación En Las Ganancias Y Contrato De Fideicomiso?

US Legal Forms - among the largest libraries of lawful types in the United States - provides an array of lawful document web templates you are able to down load or printing. Using the site, you can get a large number of types for enterprise and individual purposes, sorted by types, states, or search phrases.You can get the most recent types of types like the Indiana Profit-Sharing Plan and Trust Agreement within minutes.

If you already have a monthly subscription, log in and down load Indiana Profit-Sharing Plan and Trust Agreement from your US Legal Forms local library. The Obtain switch can look on every single develop you view. You gain access to all formerly saved types from the My Forms tab of your account.

If you wish to use US Legal Forms the very first time, here are simple recommendations to get you started out:

- Make sure you have chosen the correct develop to your area/state. Click the Review switch to analyze the form`s content material. Browse the develop description to ensure that you have selected the proper develop.

- In case the develop doesn`t match your needs, utilize the Lookup industry on top of the screen to find the the one that does.

- When you are satisfied with the form, confirm your choice by simply clicking the Purchase now switch. Then, opt for the rates program you like and give your qualifications to sign up to have an account.

- Procedure the transaction. Make use of Visa or Mastercard or PayPal account to accomplish the transaction.

- Select the structure and down load the form on your own product.

- Make changes. Fill up, edit and printing and sign the saved Indiana Profit-Sharing Plan and Trust Agreement.

Every single template you added to your bank account lacks an expiry date and is also your own property forever. So, in order to down load or printing yet another backup, just visit the My Forms segment and click around the develop you want.

Get access to the Indiana Profit-Sharing Plan and Trust Agreement with US Legal Forms, one of the most comprehensive local library of lawful document web templates. Use a large number of skilled and condition-distinct web templates that meet up with your organization or individual demands and needs.