A Surety makes itself liable for another's debts, defaults or obligations, etc. In other words, it is acting as a co-signer or guarantor for a specific deposit, performance or contract. A performance bond is a non-cancelable commitment issued by the surety to the owner of the project (obligee) guaranteeing that the contractor will complete the referenced contract within its set terms and conditions. The surety is in effect co-signing the contract. A payment bond guarantees that all sub contractors, labor and material suppliers will be paid leaving the project lien free. required to post a bond in case of any losses incurred as a result of their work or failure to complete work on the contract for the project. The bond serves as an insurance policy to the property owner or other party who may incur such loss.

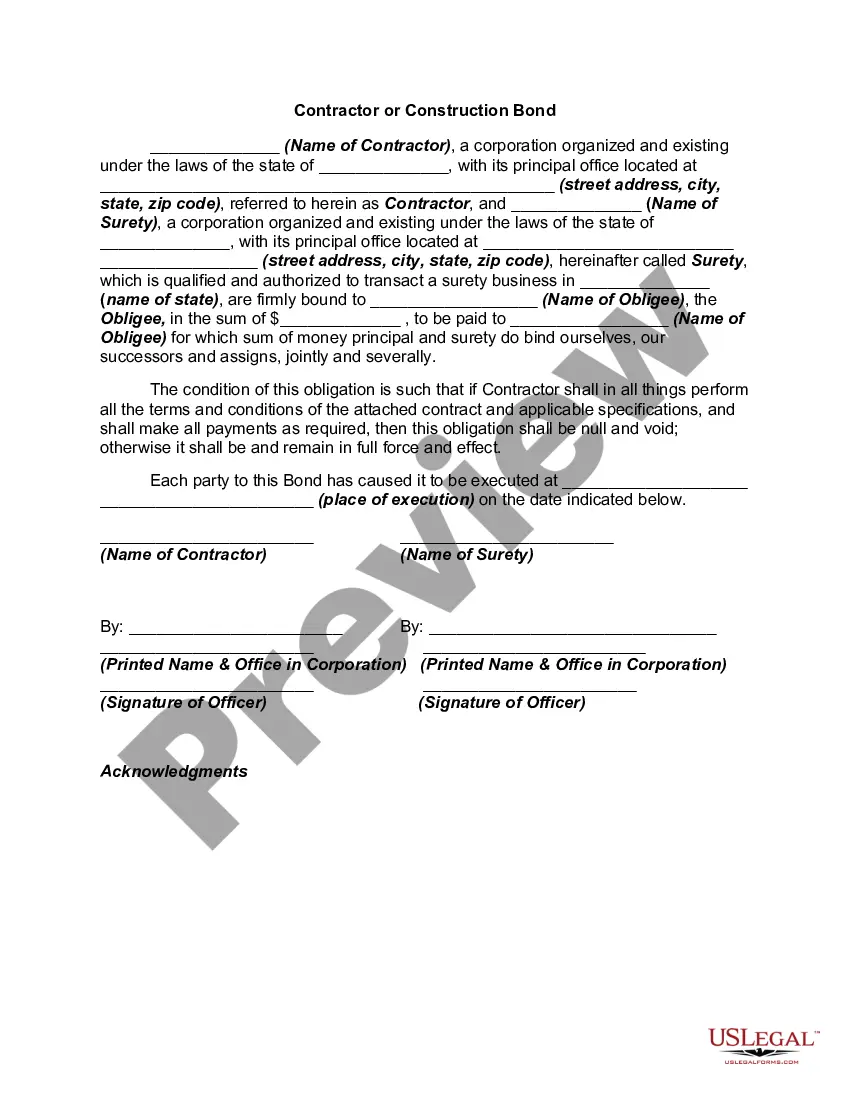

An Indiana Contractor or Construction Bond is a type of surety bond that is commonly required for contractors and construction companies in the state of Indiana. This bond is typically used to provide financial protection to project owners and ensure that contractors fulfill their contractual obligations. This bond acts as a guarantee that the contractor will complete the project according to the agreed-upon terms and conditions. It also serves as a safeguard for the project owner by providing compensation in the event that the contractor fails to complete the project, performs defective work, or violates any other terms of the contract. There are different types of Indiana Contractor or Construction Bonds that may be required depending on the specific project and circumstances. These include: 1. Bid Bond: This bond is required during the bidding process and guarantees that the contractor will enter into a contract with the project owner if selected as the winning bidder. It provides assurance to the project owner that the contractor has the financial capacity and expertise to undertake the project. 2. Performance Bond: This bond ensures that the contractor will complete the project in accordance with the terms and specifications outlined in the contract. It provides protection to the project owner in the event of non-completion or inadequate performance by the contractor. 3. Payment Bond: This bond protects subcontractors, suppliers, and laborers involved in the project by guaranteeing payment for their services and materials. It ensures that these parties will be compensated in the event that the contractor fails to make the required payments. 4. Maintenance Bond: This bond provides coverage for a specified period after the completion of the project, typically one to two years. It guarantees that the contractor will address any defects or issues that arise during the maintenance period. Obtaining an Indiana Contractor or Construction Bond usually requires the contractor to work with a surety bond company. The process involves submitting an application, undergoing underwriting, and paying a premium based on factors such as the project's size, scope, and the contractor's creditworthiness. It is essential for contractors to maintain a good credit history and financial standing to secure favorable bond terms. In summary, an Indiana Contractor or Construction Bond is a crucial financial instrument that provides security for both project owners and contractors in the construction industry. It ensures that projects are completed as agreed and protects the interests of all parties involved. By understanding the different types of bonds available, contractors can meet the necessary bonding requirements and establish a reputation for reliability and professionalism.An Indiana Contractor or Construction Bond is a type of surety bond that is commonly required for contractors and construction companies in the state of Indiana. This bond is typically used to provide financial protection to project owners and ensure that contractors fulfill their contractual obligations. This bond acts as a guarantee that the contractor will complete the project according to the agreed-upon terms and conditions. It also serves as a safeguard for the project owner by providing compensation in the event that the contractor fails to complete the project, performs defective work, or violates any other terms of the contract. There are different types of Indiana Contractor or Construction Bonds that may be required depending on the specific project and circumstances. These include: 1. Bid Bond: This bond is required during the bidding process and guarantees that the contractor will enter into a contract with the project owner if selected as the winning bidder. It provides assurance to the project owner that the contractor has the financial capacity and expertise to undertake the project. 2. Performance Bond: This bond ensures that the contractor will complete the project in accordance with the terms and specifications outlined in the contract. It provides protection to the project owner in the event of non-completion or inadequate performance by the contractor. 3. Payment Bond: This bond protects subcontractors, suppliers, and laborers involved in the project by guaranteeing payment for their services and materials. It ensures that these parties will be compensated in the event that the contractor fails to make the required payments. 4. Maintenance Bond: This bond provides coverage for a specified period after the completion of the project, typically one to two years. It guarantees that the contractor will address any defects or issues that arise during the maintenance period. Obtaining an Indiana Contractor or Construction Bond usually requires the contractor to work with a surety bond company. The process involves submitting an application, undergoing underwriting, and paying a premium based on factors such as the project's size, scope, and the contractor's creditworthiness. It is essential for contractors to maintain a good credit history and financial standing to secure favorable bond terms. In summary, an Indiana Contractor or Construction Bond is a crucial financial instrument that provides security for both project owners and contractors in the construction industry. It ensures that projects are completed as agreed and protects the interests of all parties involved. By understanding the different types of bonds available, contractors can meet the necessary bonding requirements and establish a reputation for reliability and professionalism.