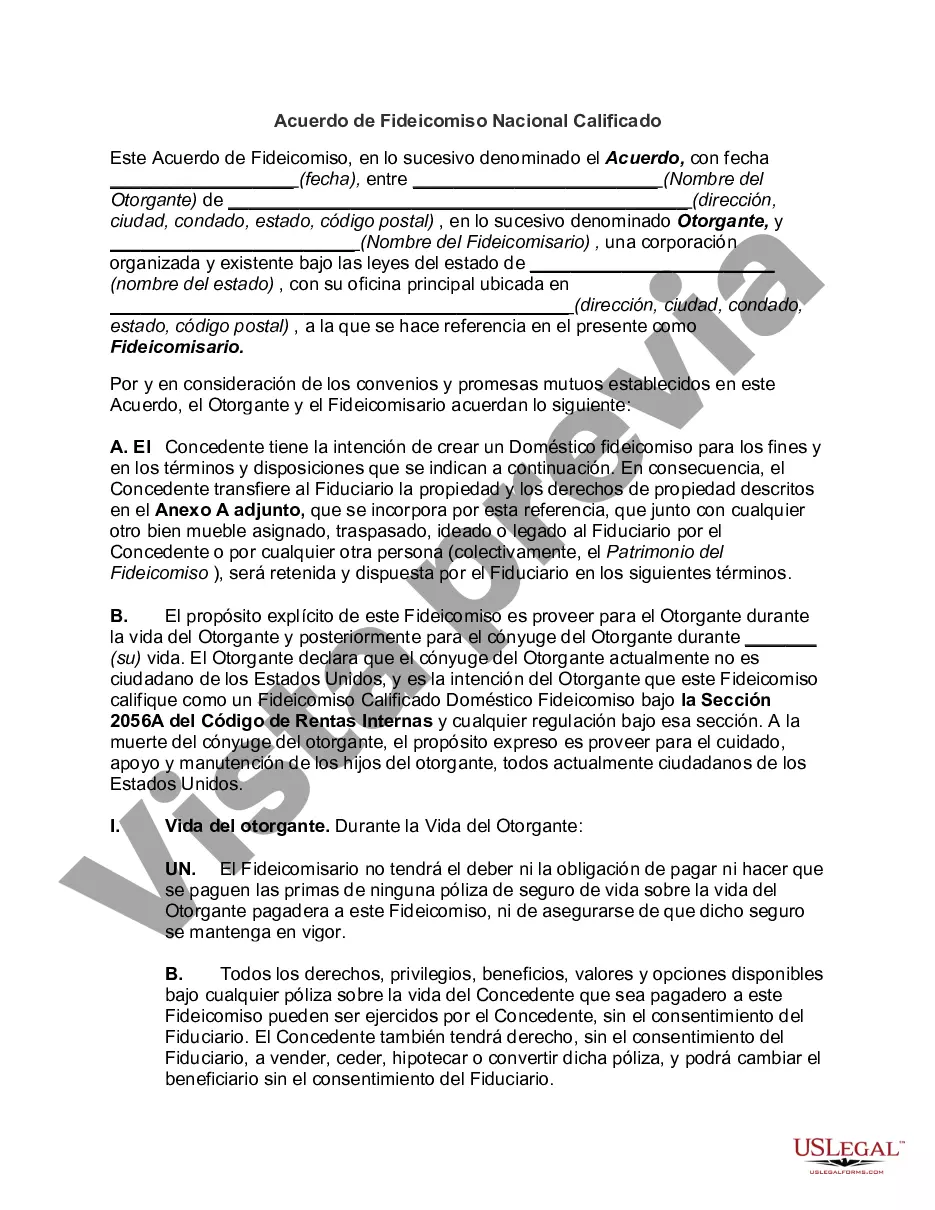

An Indiana Qualified Domestic Trust Agreement, commonly known as an Indiana DOT Agreement, is a legal document designed to address estate planning concerns for non-U.S. citizen spouses who inherit property from their U.S. citizen spouses. This arrangement allows the non-U.S. citizen spouse to take advantage of the marital deduction and defer the payment of federal estate taxes until the property is sold or transferred. In order to qualify as an Indiana DOT Agreement, certain requirements must be met. Firstly, the trust must be created after the death of the U.S. citizen spouse and be irrevocable. Additionally, the trust must have at least one trustee, who can be an individual or an institution, and must be a U.S. citizen or a U.S. domestic corporation. The trustee's role is crucial as they are responsible for managing the trust assets and ensuring compliance with the trust agreement. Furthermore, the Indiana DOT Agreement dictates that at least one trustee must be a qualified trustee, which means they will be personally liable for any taxes imposed on the trust. This provision is essential as it ensures the IRS can collect estate taxes if the non-U.S. citizen spouse were to avoid making the necessary payments. There are two primary types of Indiana Qualified Domestic Trust Agreements. The first type is a "system trust" or a "conduit trust." Under this arrangement, the income generated by the trust is distributed annually to the non-U.S. citizen spouse, and any estate taxes applicable to the principal portion of the trust are deferred until the non-U.S. citizen spouse's death. However, the principal cannot be distributed without triggering estate taxes. The second type of Indiana DOT Agreement is a "comprehensive trust" or a "non-conduit trust." This trust offers more flexibility by allowing the trustee to distribute both income and principal to the non-U.S. citizen spouse and, at the same time, defer estate taxes. It provides greater control and access to the trust assets for the surviving non-U.S. citizen spouse. In conclusion, an Indiana Qualified Domestic Trust Agreement serves as a vital tool for non-U.S. citizen spouses to effectively manage and preserve their inherited wealth while minimizing estate taxes. It ensures compliance with U.S. estate tax laws and allows the surviving spouse to benefit from the marital deduction. By choosing the appropriate type of trust agreement, individuals can tailor their estate plan to their specific needs and goals.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Indiana Acuerdo de Fideicomiso Nacional Calificado - Qualified Domestic Trust Agreement

Description

How to fill out Indiana Acuerdo De Fideicomiso Nacional Calificado?

US Legal Forms - one of many most significant libraries of legal kinds in the USA - offers a wide array of legal document layouts you may download or print out. Making use of the web site, you can get a huge number of kinds for business and person functions, sorted by groups, says, or keywords.You can find the latest variations of kinds much like the Indiana Qualified Domestic Trust Agreement in seconds.

If you currently have a membership, log in and download Indiana Qualified Domestic Trust Agreement in the US Legal Forms library. The Acquire switch will appear on each develop you look at. You have accessibility to all in the past downloaded kinds from the My Forms tab of your own bank account.

In order to use US Legal Forms initially, listed below are straightforward recommendations to obtain started:

- Be sure to have picked the proper develop for the area/state. Click the Review switch to check the form`s articles. See the develop outline to actually have chosen the proper develop.

- In case the develop doesn`t match your specifications, take advantage of the Lookup discipline near the top of the screen to find the one which does.

- Should you be content with the shape, affirm your choice by visiting the Purchase now switch. Then, pick the prices strategy you prefer and offer your references to sign up for the bank account.

- Method the purchase. Make use of your Visa or Mastercard or PayPal bank account to perform the purchase.

- Pick the format and download the shape on the gadget.

- Make modifications. Complete, change and print out and signal the downloaded Indiana Qualified Domestic Trust Agreement.

Every single design you included with your account does not have an expiry day and is also the one you have for a long time. So, if you wish to download or print out an additional version, just proceed to the My Forms area and then click in the develop you require.

Gain access to the Indiana Qualified Domestic Trust Agreement with US Legal Forms, the most extensive library of legal document layouts. Use a huge number of specialist and state-particular layouts that meet up with your business or person requires and specifications.