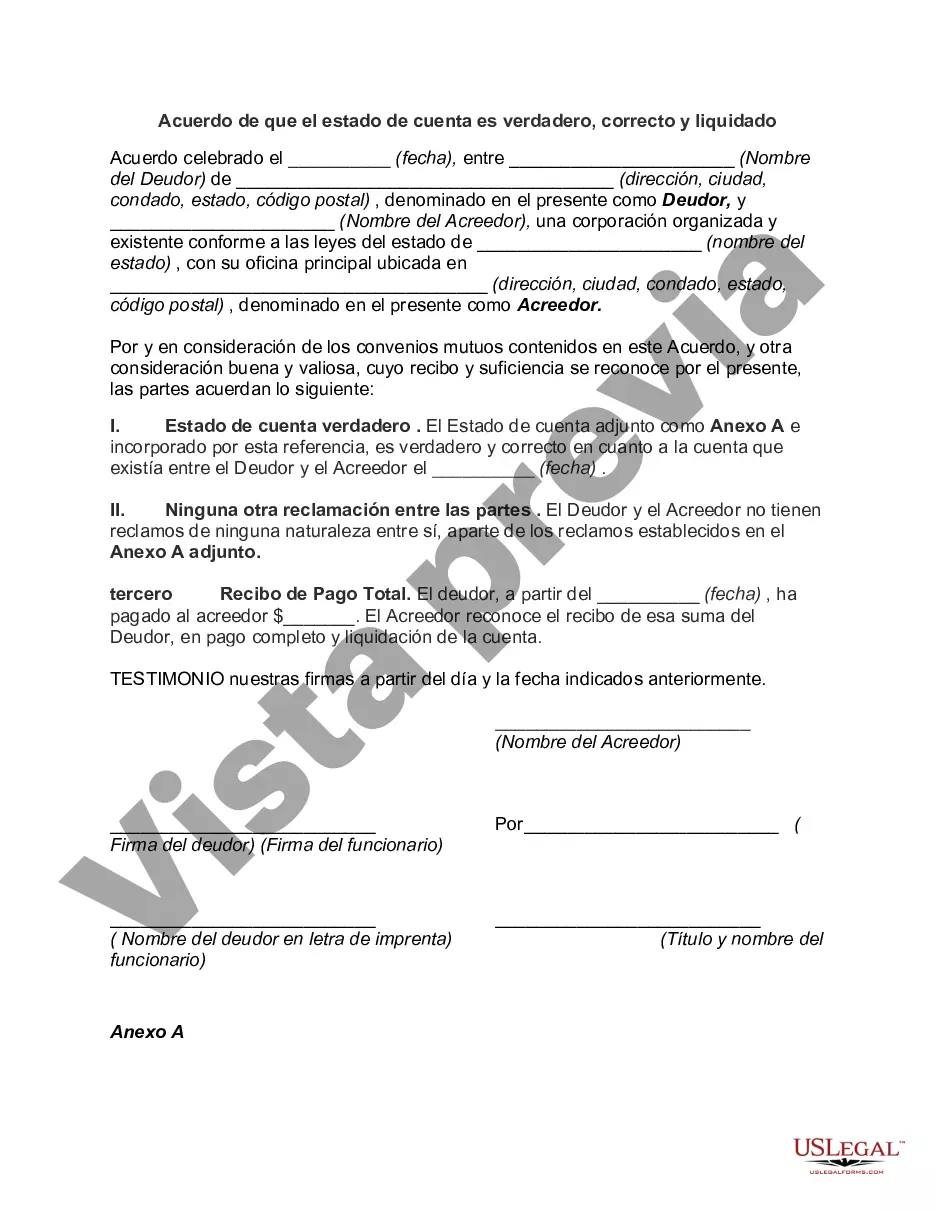

The Kentucky Agreement, also known as the Kentucky Accord, refers to a legal document or agreement that ensures the accuracy and finality of the statement of account. It is used to confirm that the statement of account is true, correct, and settled, effectively bringing an end to any financial disputes or outstanding balances. In various industries and legal contexts, there can be different types of Kentucky Agreements used to validate the accuracy of the statement of account. Some common types include: 1. Kentucky Agreement for Business Transactions: This type of agreement is commonly used in commercial or business settings where parties need to confirm the accuracy and settlement of financial transactions. It outlines the details of the transactions, confirms the amounts owed, and affirms that the statement of account provided is true and correct. 2. Kentucky Agreement for Debt Settlement: When dealing with debts, creditors or collection agencies may require a Kentucky Agreement to settle and close the account. This agreement ensures that the debtor acknowledges and accepts the stated amount due and declares it as settled, preventing any future disputes or claims. 3. Kentucky Agreement for Legal Settlement: In legal proceedings where financial matters are involved, the parties may reach a settlement agreement. As part of this agreement, a Kentucky Agreement may be included to affirm that all financial obligations have been met and the statement of account provided is accurate and final. 4. Kentucky Agreement for Real Estate Transactions: When finalizing real estate deals, a Kentucky Agreement may be used to confirm the accuracy of financial statements, including purchase price, taxes, fees, and closing costs. This agreement ensures that both buyer and seller agree that the statement of account is true, correct, and settled, solidifying the financial aspect of the transaction. In all the aforementioned types, the Kentucky Agreement serves as a legally binding document where the involved parties declare their acceptance, understanding, and agreement that the statement of account provided is accurate, true, and represents the final settlement. By signing this agreement, the parties effectively waive any future claims or disputes related to the stated financial obligations.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Kentucky Acuerdo de que el estado de cuenta es verdadero, correcto y liquidado - Agreement that Statement of Account is True, Correct and Settled

Description

How to fill out Kentucky Acuerdo De Que El Estado De Cuenta Es Verdadero, Correcto Y Liquidado?

Discovering the right lawful papers design might be a have difficulties. Needless to say, there are plenty of web templates available on the Internet, but how would you discover the lawful type you need? Use the US Legal Forms web site. The service gives thousands of web templates, like the Kentucky Agreement that Statement of Account is True, Correct and Settled, that you can use for business and private needs. Every one of the forms are checked by specialists and meet up with state and federal needs.

In case you are already signed up, log in in your bank account and click on the Obtain switch to obtain the Kentucky Agreement that Statement of Account is True, Correct and Settled. Make use of your bank account to appear with the lawful forms you have purchased previously. Proceed to the My Forms tab of your own bank account and obtain an additional backup in the papers you need.

In case you are a whole new user of US Legal Forms, here are basic directions so that you can stick to:

- Very first, make sure you have chosen the appropriate type to your town/state. You are able to look over the shape making use of the Review switch and look at the shape description to ensure it will be the right one for you.

- In case the type fails to meet up with your expectations, use the Seach field to obtain the appropriate type.

- Once you are certain that the shape would work, click on the Buy now switch to obtain the type.

- Choose the costs strategy you need and enter in the required info. Create your bank account and pay money for your order utilizing your PayPal bank account or credit card.

- Pick the data file format and acquire the lawful papers design in your system.

- Complete, revise and produce and signal the obtained Kentucky Agreement that Statement of Account is True, Correct and Settled.

US Legal Forms is the biggest library of lawful forms in which you will find various papers web templates. Use the service to acquire professionally-created papers that stick to status needs.