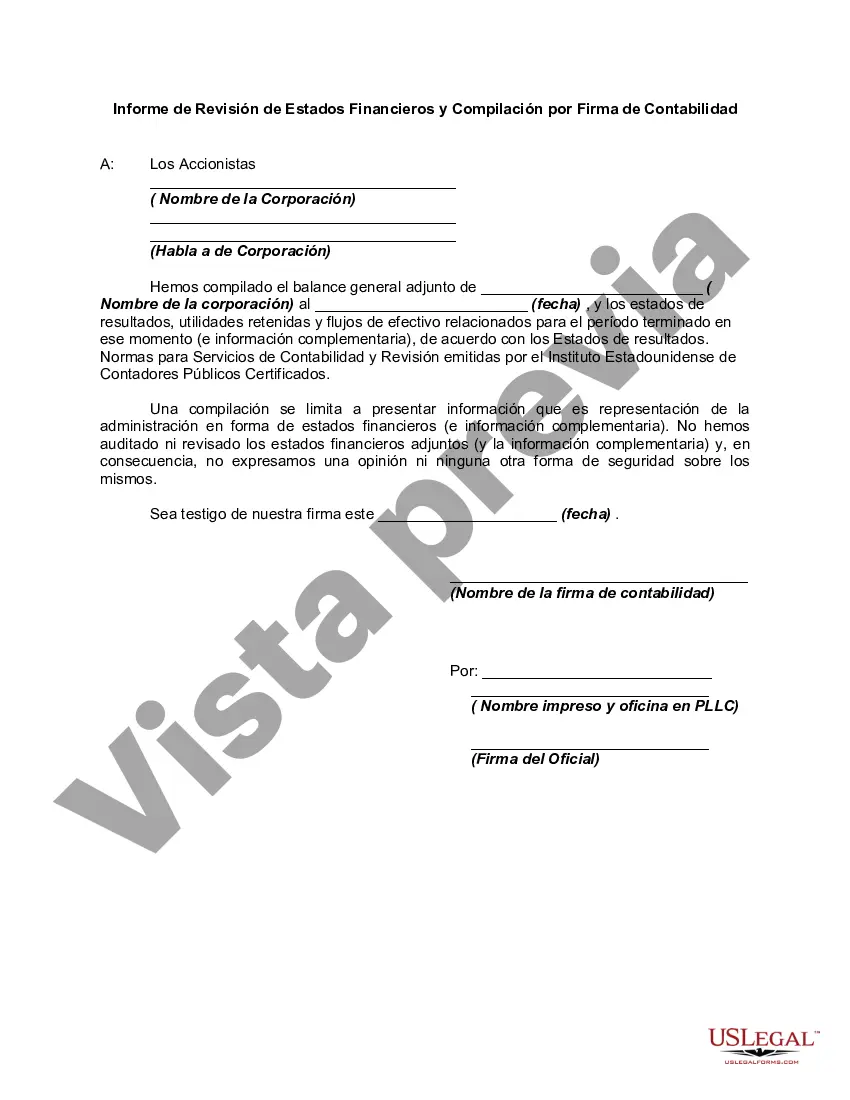

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Title: Comprehensive Guide to Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm Introduction: Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm plays a crucial role in assessing the financial health and compliance of an organization operating within the state. These reports provide essential information to stakeholders, including investors, lenders, and regulatory bodies. In this comprehensive guide, we will delve into the details of Louisiana Reports from Review of Financial Statements and Compilation by Accounting Firm, examining their significance, purpose, and the different types of reports available. I. Louisiana Report from Review of Financial Statements: The Louisiana Report from Review of Financial Statements is an evaluation conducted by an independent accounting firm to analyze the financial statements prepared by a client. This report aims to provide limited assurance that the financial statements are free from material misstatements and are prepared in accordance with the applicable accounting principles. The report typically covers the following key areas: 1. Scope of the review: This section explains the extent of the review performed by the accounting firm, outlining the procedures and methodologies applied. It helps stakeholders understand the limitations of the review and the level of assurance provided. 2. Management's responsibility: Here, the report emphasizes that the responsibility for the financial statements' accuracy and compliance lies with the management. It clarifies that the review performed does not alleviate management's responsibility for the financial statements. 3. Accountant's review procedures: This section describes the specific procedures followed by the accounting firm during the review process. It may include inquiries, analytical procedures, and other investigative measures employed to assess the reasonableness of financial information. 4. Review findings and opinion: The report concludes with the accountant's findings and opinion regarding the reviewed financial statements. The opinion may state that the financial statements appear to be free from material misstatements, providing limited assurance to stakeholders. II. Louisiana Report from Compilation of Financial Statements: The Louisiana Report from Compilation of Financial Statements involves the preparation of financial statements by an accountant based on information provided by the client. This report does not provide any assurance or opinion about the financial statements' accuracy or compliance. Instead, it presents the financial data in a standardized format, facilitating its use for internal purposes such as management decision-making and tax filing. The compilation report broadly covers the following elements: 1. Accountant's responsibility: This section clarifies the accountant's role regarding the client's financial statements. It highlights that the compilation report offers no assurance or opinion on the financial statements' accuracy and compliance. 2. Management's responsibility: Similar to the review report, this section emphasizes management's responsibility for the financial statements' preparation and integrity. It stresses that the accountant's involvement is limited to compiling the provided financial information. 3. Compilation procedure: Here, the report explains the processes undertaken by the accountant to compile the financial statements. It outlines the accountant's responsibility to ensure the information is properly organized and presented in accordance with the applicable accounting standards. Conclusion: Louisiana Reports from Review of Financial Statements and Compilation by Accounting Firm play a vital role in providing stakeholders with valuable insights into an organization's financial health and adherence to accounting principles. By understanding the different types of reports available, stakeholders can make informed decisions based on the assurance or limited assurance provided. Leveraging the expertise of accounting firms to conduct these reviews and compilations enables businesses to maintain transparency, strengthen investor confidence, and comply with regulatory requirements.Title: Comprehensive Guide to Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm Introduction: Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm plays a crucial role in assessing the financial health and compliance of an organization operating within the state. These reports provide essential information to stakeholders, including investors, lenders, and regulatory bodies. In this comprehensive guide, we will delve into the details of Louisiana Reports from Review of Financial Statements and Compilation by Accounting Firm, examining their significance, purpose, and the different types of reports available. I. Louisiana Report from Review of Financial Statements: The Louisiana Report from Review of Financial Statements is an evaluation conducted by an independent accounting firm to analyze the financial statements prepared by a client. This report aims to provide limited assurance that the financial statements are free from material misstatements and are prepared in accordance with the applicable accounting principles. The report typically covers the following key areas: 1. Scope of the review: This section explains the extent of the review performed by the accounting firm, outlining the procedures and methodologies applied. It helps stakeholders understand the limitations of the review and the level of assurance provided. 2. Management's responsibility: Here, the report emphasizes that the responsibility for the financial statements' accuracy and compliance lies with the management. It clarifies that the review performed does not alleviate management's responsibility for the financial statements. 3. Accountant's review procedures: This section describes the specific procedures followed by the accounting firm during the review process. It may include inquiries, analytical procedures, and other investigative measures employed to assess the reasonableness of financial information. 4. Review findings and opinion: The report concludes with the accountant's findings and opinion regarding the reviewed financial statements. The opinion may state that the financial statements appear to be free from material misstatements, providing limited assurance to stakeholders. II. Louisiana Report from Compilation of Financial Statements: The Louisiana Report from Compilation of Financial Statements involves the preparation of financial statements by an accountant based on information provided by the client. This report does not provide any assurance or opinion about the financial statements' accuracy or compliance. Instead, it presents the financial data in a standardized format, facilitating its use for internal purposes such as management decision-making and tax filing. The compilation report broadly covers the following elements: 1. Accountant's responsibility: This section clarifies the accountant's role regarding the client's financial statements. It highlights that the compilation report offers no assurance or opinion on the financial statements' accuracy and compliance. 2. Management's responsibility: Similar to the review report, this section emphasizes management's responsibility for the financial statements' preparation and integrity. It stresses that the accountant's involvement is limited to compiling the provided financial information. 3. Compilation procedure: Here, the report explains the processes undertaken by the accountant to compile the financial statements. It outlines the accountant's responsibility to ensure the information is properly organized and presented in accordance with the applicable accounting standards. Conclusion: Louisiana Reports from Review of Financial Statements and Compilation by Accounting Firm play a vital role in providing stakeholders with valuable insights into an organization's financial health and adherence to accounting principles. By understanding the different types of reports available, stakeholders can make informed decisions based on the assurance or limited assurance provided. Leveraging the expertise of accounting firms to conduct these reviews and compilations enables businesses to maintain transparency, strengthen investor confidence, and comply with regulatory requirements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.