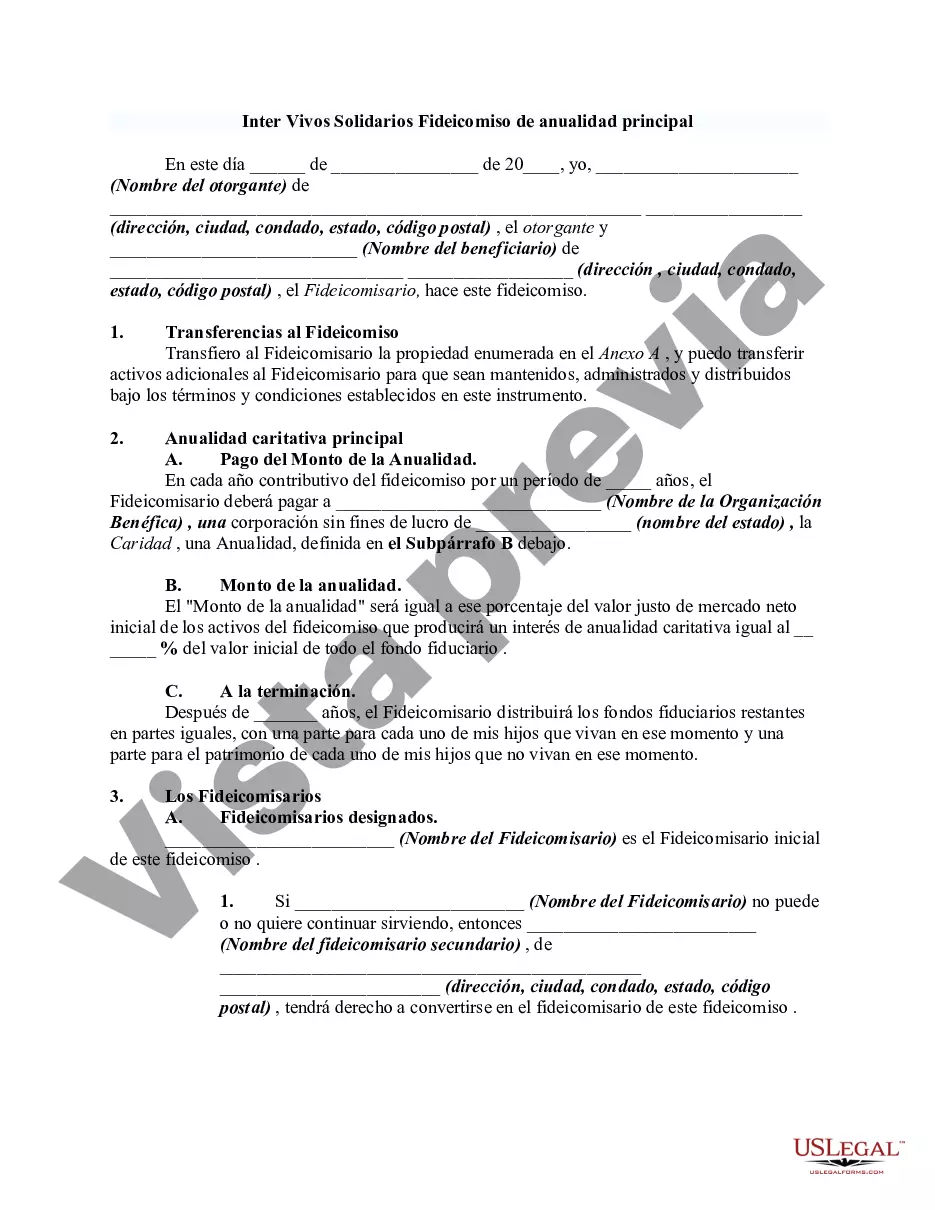

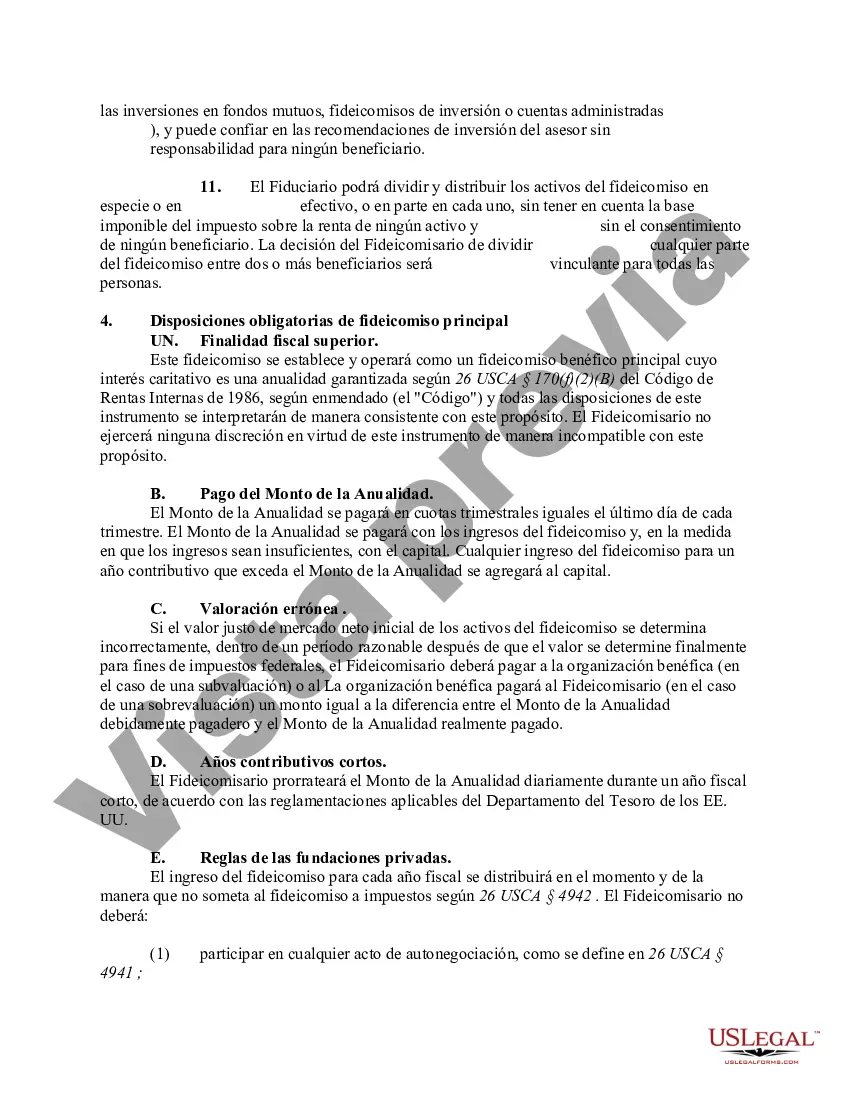

In a charitable lead trust, the lifetime payments go to the charity and the remainder returns to the donor or to the donor's estate or other beneficiaries. A donor transfers property to the lead trust, which pays a percentage of the value of the trust assets, usually for a term of years, to the charity. Unlike a charitable remainder trust, a charitable lead annuity trust creates no income tax deduction to the donor, but the income earned in the trust is not attributed to donor. The trust itself is taxed according to trust rates. The trust receives an income tax deduction for the income paid to charity.

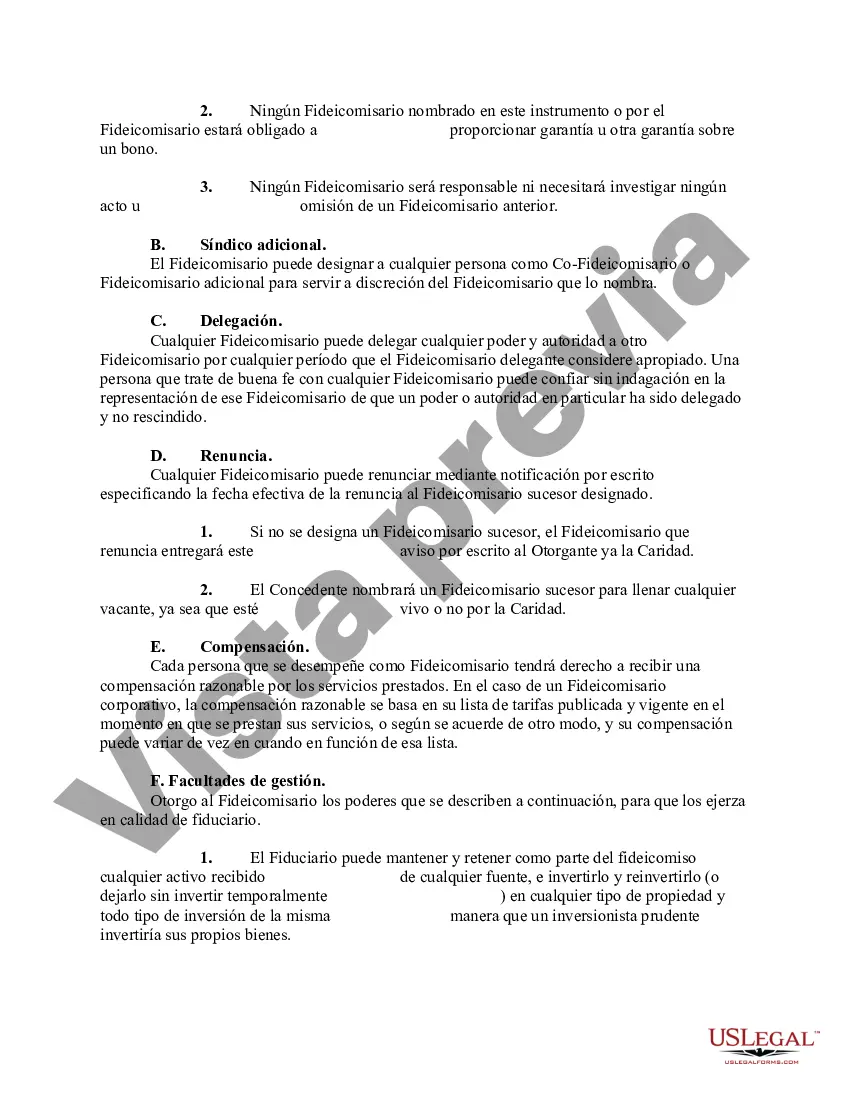

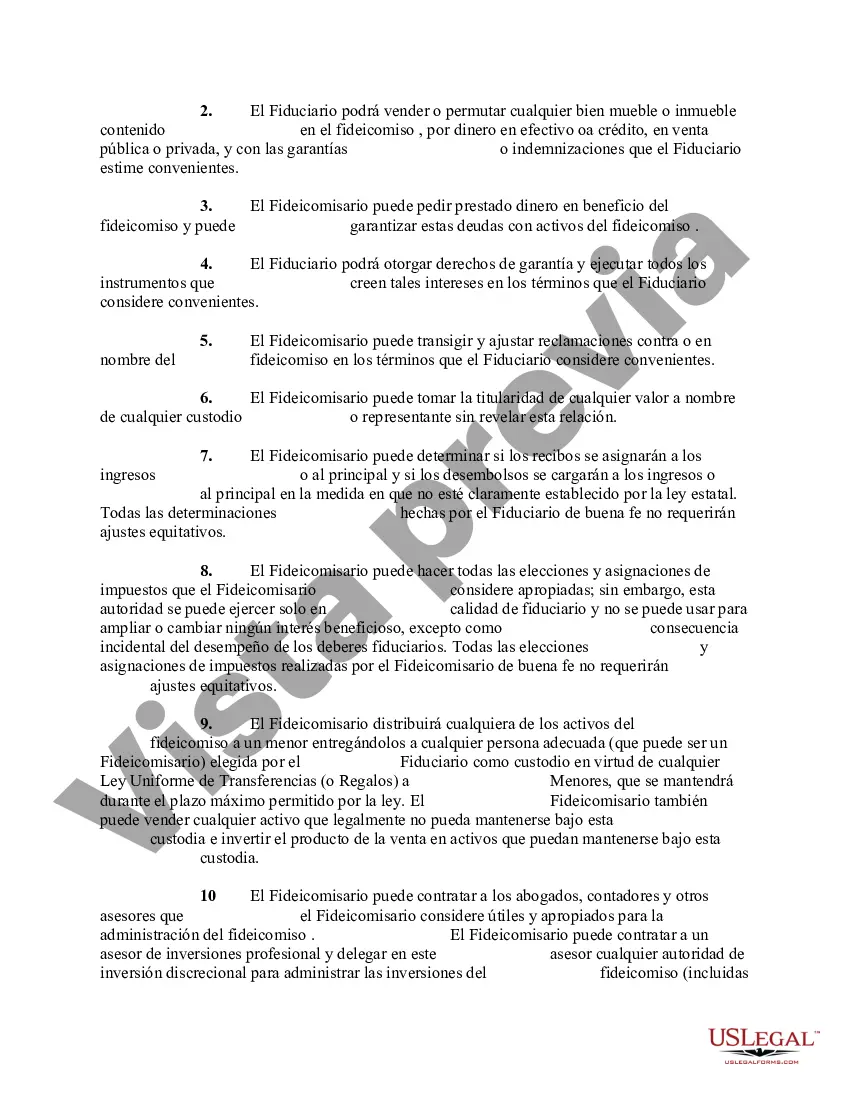

The Massachusetts Charitable Inter Vivos Lead Annuity Trust, commonly referred to as CIT or FLAT, is a type of trust designed to provide support to charitable organizations while allowing the trust creator, also known as the granter or settler, to retain control over their assets during their lifetime. This trust is established and governed by Massachusetts state law. In a Charitable Inter Vivos Lead Annuity Trust, the granter transfers assets, such as cash, securities, or real estate, to the trust while specifying a fixed annual payment or annuity to be donated to one or more charitable organizations for a predetermined period. This annual payment is known as the "charitable lead," and it is distributed before any remaining income or assets are passed on to the trust's non-charitable beneficiaries, which often include family members or other individuals. By using a Charitable Inter Vivos Lead Annuity Trust, the granter can support their preferred charitable causes during their lifetime, potentially benefiting from income and estate tax deductions, while still ensuring that their non-charitable beneficiaries receive the remaining trust assets after a specified period. There are different types of Massachusetts Charitable Inter Vivos Lead Annuity Trusts, each with unique characteristics and benefits. These include: 1. Non-Grantor Charitable Lead Annuity Trust (FLAT): In this type of trust, the granter transfers assets to the trust, and the charitable lead annuity payment is fixed throughout the trust's term. At the end of the term, any remaining trust assets pass to the non-charitable beneficiaries with potential estate tax advantages. 2. Granter Charitable Lead Annuity Trust (Granter FLAT): In a Granter FLAT, the granter includes the annuity payment received by the charitable organization as taxable income, potentially resulting in a charitable income tax deduction upfront. This type of trust can be beneficial when the granter has a high-income year or anticipates lower tax rates in the future. 3. Charitable Remainder Annuity Trust with a Charitable Inter Vivos Lead Annuity Trust (CAT with FLAT): This trust structure involves the granter establishing both a Charitable Remainder Annuity Trust (CAT) and a Charitable Inter Vivos Lead Annuity Trust (FLAT). The CAT provides income to non-charitable beneficiaries for a specified period or their lifetimes, while the FLAT makes charitable lead annuity payments during the same timeframe. This arrangement allows the granter to support both charitable causes and non-charitable beneficiaries simultaneously. Establishing a Massachusetts Charitable Inter Vivos Lead Annuity Trust requires careful consideration and legal expertise. It is essential to consult with an experienced estate planning attorney or financial advisor to ensure the trust aligns with your philanthropic goals and financial circumstances while adhering to state laws and regulations.The Massachusetts Charitable Inter Vivos Lead Annuity Trust, commonly referred to as CIT or FLAT, is a type of trust designed to provide support to charitable organizations while allowing the trust creator, also known as the granter or settler, to retain control over their assets during their lifetime. This trust is established and governed by Massachusetts state law. In a Charitable Inter Vivos Lead Annuity Trust, the granter transfers assets, such as cash, securities, or real estate, to the trust while specifying a fixed annual payment or annuity to be donated to one or more charitable organizations for a predetermined period. This annual payment is known as the "charitable lead," and it is distributed before any remaining income or assets are passed on to the trust's non-charitable beneficiaries, which often include family members or other individuals. By using a Charitable Inter Vivos Lead Annuity Trust, the granter can support their preferred charitable causes during their lifetime, potentially benefiting from income and estate tax deductions, while still ensuring that their non-charitable beneficiaries receive the remaining trust assets after a specified period. There are different types of Massachusetts Charitable Inter Vivos Lead Annuity Trusts, each with unique characteristics and benefits. These include: 1. Non-Grantor Charitable Lead Annuity Trust (FLAT): In this type of trust, the granter transfers assets to the trust, and the charitable lead annuity payment is fixed throughout the trust's term. At the end of the term, any remaining trust assets pass to the non-charitable beneficiaries with potential estate tax advantages. 2. Granter Charitable Lead Annuity Trust (Granter FLAT): In a Granter FLAT, the granter includes the annuity payment received by the charitable organization as taxable income, potentially resulting in a charitable income tax deduction upfront. This type of trust can be beneficial when the granter has a high-income year or anticipates lower tax rates in the future. 3. Charitable Remainder Annuity Trust with a Charitable Inter Vivos Lead Annuity Trust (CAT with FLAT): This trust structure involves the granter establishing both a Charitable Remainder Annuity Trust (CAT) and a Charitable Inter Vivos Lead Annuity Trust (FLAT). The CAT provides income to non-charitable beneficiaries for a specified period or their lifetimes, while the FLAT makes charitable lead annuity payments during the same timeframe. This arrangement allows the granter to support both charitable causes and non-charitable beneficiaries simultaneously. Establishing a Massachusetts Charitable Inter Vivos Lead Annuity Trust requires careful consideration and legal expertise. It is essential to consult with an experienced estate planning attorney or financial advisor to ensure the trust aligns with your philanthropic goals and financial circumstances while adhering to state laws and regulations.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.