A Massachusetts Promissory Note in Connection with a Sale and Purchase of a Mobile Home is a legally binding document that outlines the terms and conditions of a loan agreement between the buyer and the seller of a mobile home. This note serves as a written record of the financial agreement and sets forth the obligations and responsibilities of both parties involved in the transaction. Keywords: Massachusetts Promissory Note, Sale and Purchase, Mobile Home, Loan Agreement, Terms and Conditions, Buyer, Seller, Financial Agreement, Obligations, Responsibilities, Transaction. There are several types of Massachusetts Promissory Notes in Connection with a Sale and Purchase of a Mobile Home that are commonly used: 1. Fixed-Rate Promissory Note: This type of promissory note establishes a fixed interest rate for the loan, which remains unchanged throughout the loan term. The buyer agrees to repay the loan amount in regular installments over a specified period, typically ranging from 5 to 30 years. 2. Adjustable-Rate Promissory Note: In an adjustable-rate promissory note, the interest rate is not fixed and can fluctuate according to market conditions. The initial interest rate is usually lower than that of a fixed-rate note, but it can increase or decrease periodically based on predetermined intervals stipulated in the agreement. 3. Balloon Payment Promissory Note: A balloon payment promissory note involves regular installments for a specific period, typically shorter than the actual loan term. At the end of this period, a large final payment called the balloon payment is due, representing the remaining balance of the loan. This type of note is often used when the buyer anticipates a significant influx of funds in the future. 4. Installment Promissory Note: An installment promissory note establishes equal periodic payments, including both principal and interest, over a fixed period. The buyer agrees to repay the loan amount in agreed-upon installments, usually monthly, until the full loan balance is cleared. 5. Secured Promissory Note: A secured promissory note utilizes the mobile home itself as collateral for the loan. If the buyer defaults on the loan payments, the seller has the right to seize and sell the mobile home to recoup the outstanding balance. In conclusion, a Massachusetts Promissory Note in Connection with a Sale and Purchase of a Mobile Home is a crucial legal document that outlines the terms and conditions of a loan agreement for the sale and purchase of a mobile home. Different types of notes, such as fixed-rate, adjustable-rate, balloon payment, installment, and secured promissory notes, offer various repayment options to accommodate the buyer and seller's preferences and financial needs.

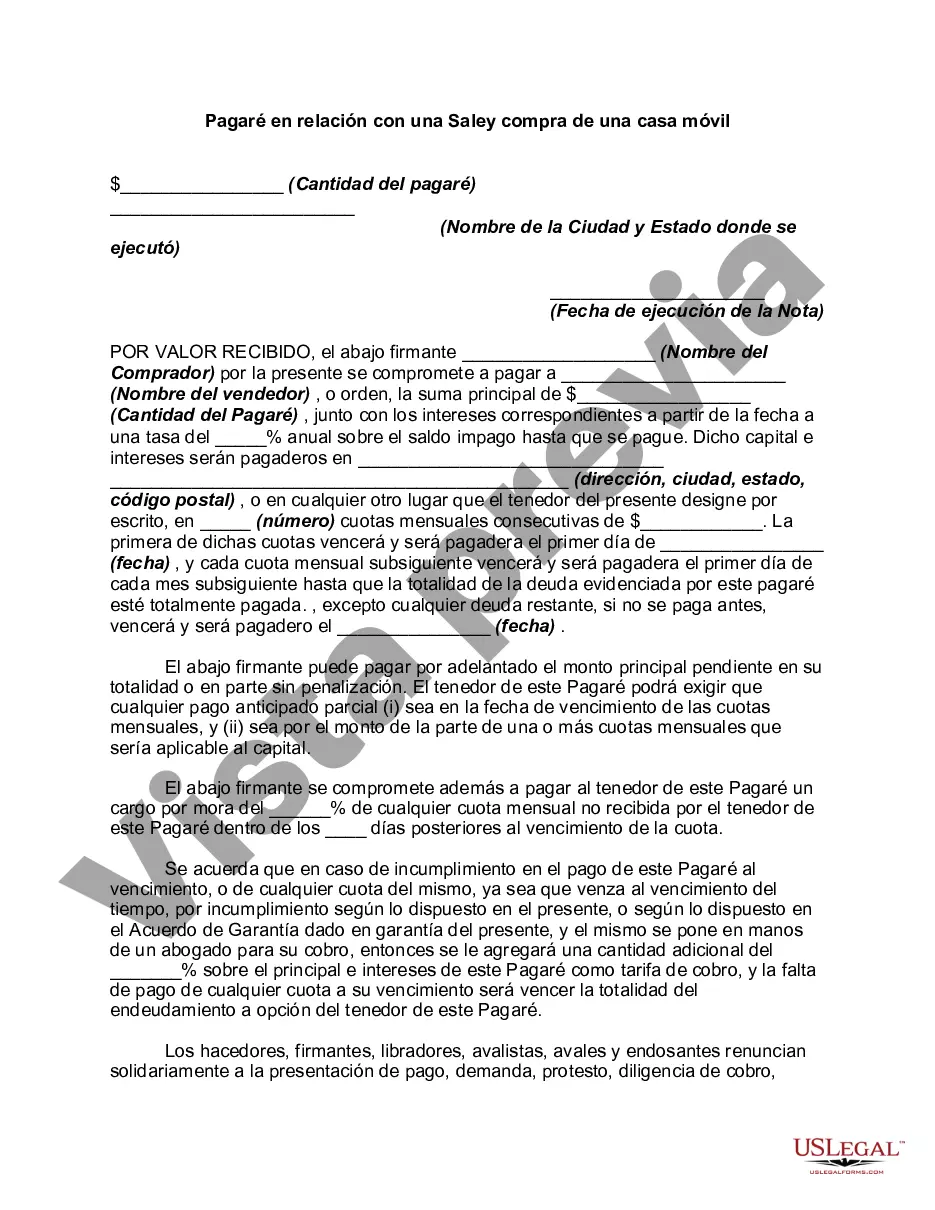

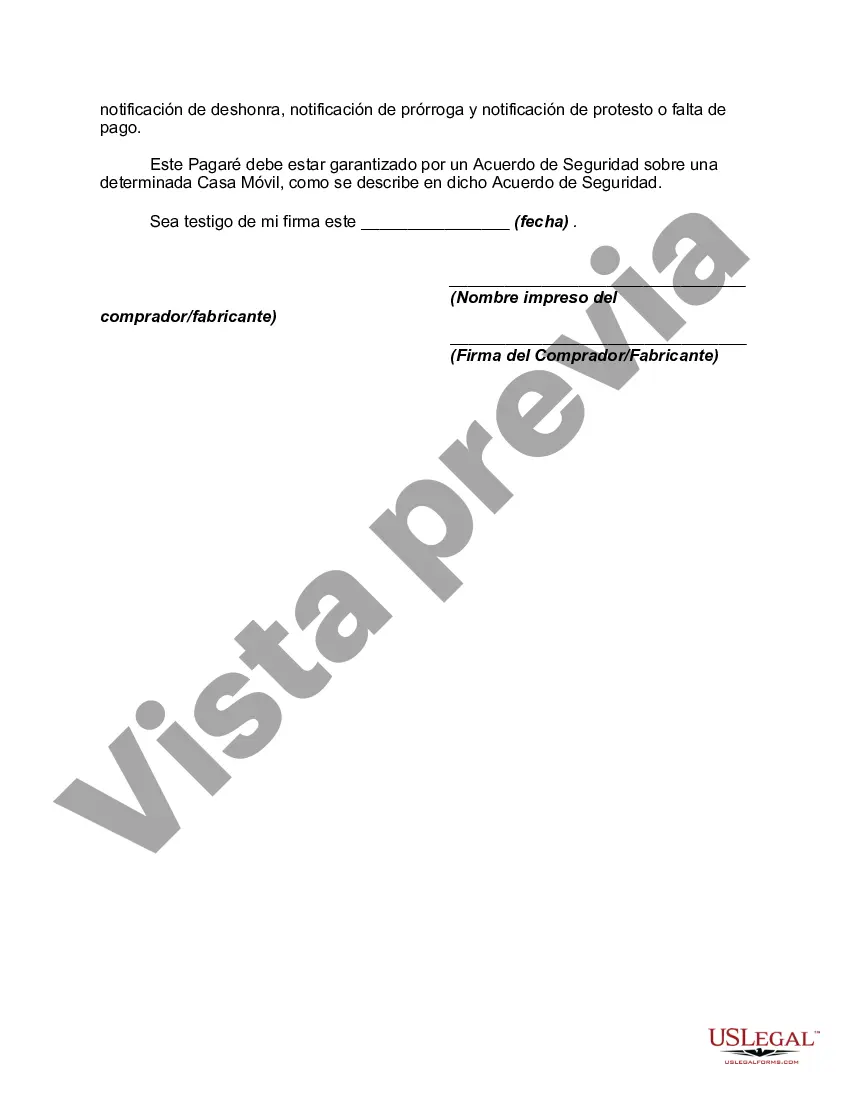

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Massachusetts Pagaré en relación con la compra y venta de una casa móvil - Promissory Note in Connection with a Sale and Purchase of a Mobile Home

Description

How to fill out Massachusetts Pagaré En Relación Con La Compra Y Venta De Una Casa Móvil?

Are you presently inside a place in which you need to have documents for sometimes business or specific functions virtually every time? There are tons of legitimate file layouts available online, but getting ones you can rely is not straightforward. US Legal Forms offers thousands of kind layouts, like the Massachusetts Promissory Note in Connection with a Sale and Purchase of a Mobile Home, that are written to meet federal and state demands.

If you are currently knowledgeable about US Legal Forms internet site and also have a free account, just log in. Afterward, you may acquire the Massachusetts Promissory Note in Connection with a Sale and Purchase of a Mobile Home web template.

If you do not come with an bank account and would like to begin using US Legal Forms, abide by these steps:

- Discover the kind you will need and make sure it is for the right metropolis/county.

- Use the Review button to check the shape.

- See the description to ensure that you have chosen the proper kind.

- In the event the kind is not what you are looking for, take advantage of the Lookup discipline to obtain the kind that meets your needs and demands.

- When you find the right kind, simply click Purchase now.

- Choose the prices strategy you need, fill in the desired information to produce your account, and pay for the order with your PayPal or bank card.

- Decide on a hassle-free file formatting and acquire your duplicate.

Discover every one of the file layouts you might have purchased in the My Forms menu. You can obtain a extra duplicate of Massachusetts Promissory Note in Connection with a Sale and Purchase of a Mobile Home at any time, if possible. Just click the necessary kind to acquire or print the file web template.

Use US Legal Forms, the most considerable variety of legitimate forms, in order to save efforts and stay away from errors. The support offers skillfully produced legitimate file layouts that can be used for an array of functions. Generate a free account on US Legal Forms and begin generating your way of life a little easier.