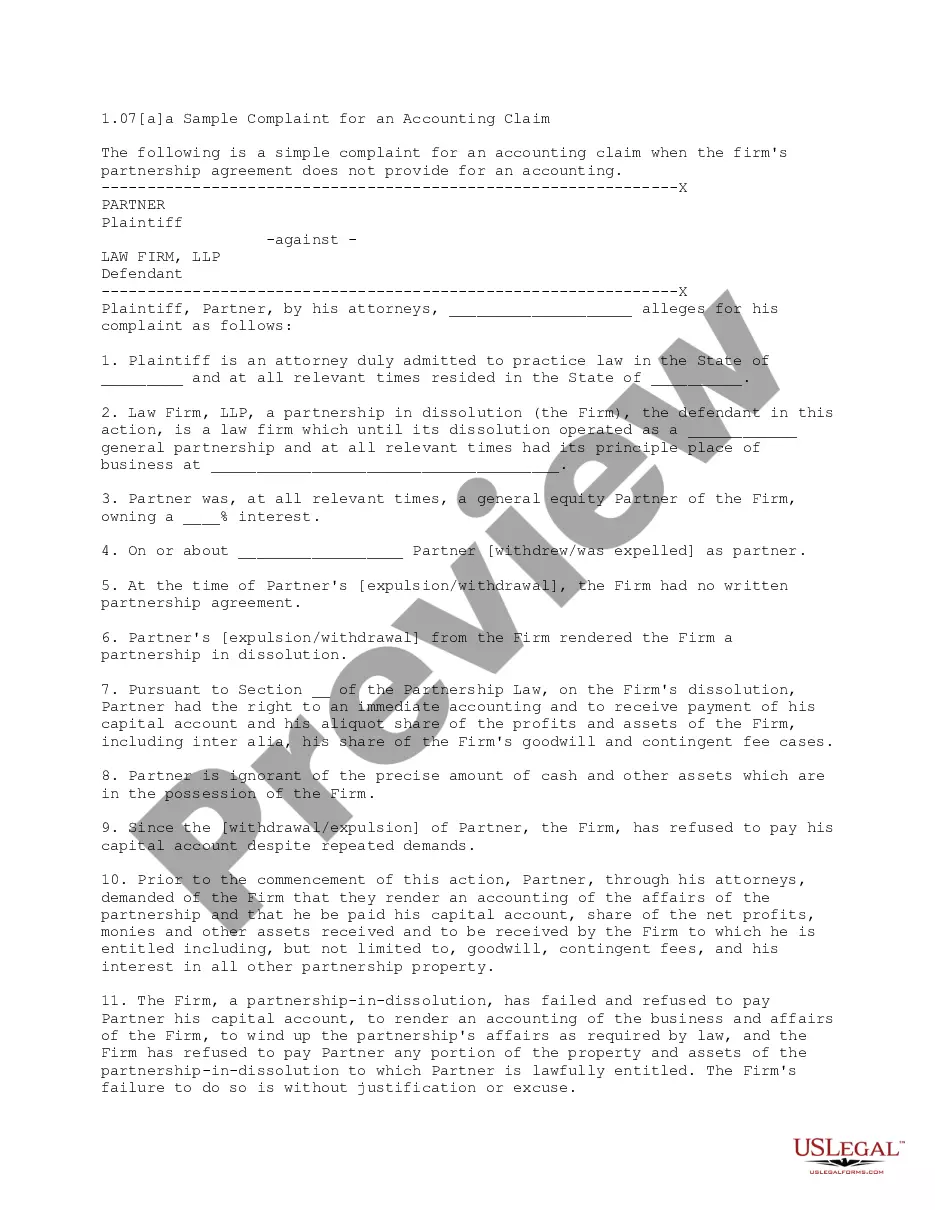

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Massachusetts Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

If you have to comprehensive, down load, or printing authorized file templates, use US Legal Forms, the greatest collection of authorized types, that can be found on the Internet. Utilize the site`s easy and hassle-free search to obtain the files you need. Numerous templates for enterprise and person purposes are sorted by classes and suggests, or search phrases. Use US Legal Forms to obtain the Massachusetts Alternative Complaint for an Accounting which includes Egregious Acts with a few click throughs.

When you are presently a US Legal Forms client, log in to the accounts and click the Obtain option to get the Massachusetts Alternative Complaint for an Accounting which includes Egregious Acts. You can even accessibility types you in the past saved inside the My Forms tab of the accounts.

If you are using US Legal Forms initially, refer to the instructions under:

- Step 1. Be sure you have selected the form for your appropriate area/nation.

- Step 2. Use the Review option to check out the form`s content material. Do not overlook to read the description.

- Step 3. When you are not satisfied using the develop, take advantage of the Look for area on top of the monitor to find other variations in the authorized develop template.

- Step 4. After you have found the form you need, click the Purchase now option. Choose the costs program you prefer and add your references to register to have an accounts.

- Step 5. Approach the purchase. You can use your Мisa or Ьastercard or PayPal accounts to accomplish the purchase.

- Step 6. Choose the format in the authorized develop and down load it on the device.

- Step 7. Total, edit and printing or indicator the Massachusetts Alternative Complaint for an Accounting which includes Egregious Acts.

Each authorized file template you purchase is your own eternally. You have acces to each and every develop you saved inside your acccount. Go through the My Forms portion and pick a develop to printing or down load once again.

Remain competitive and down load, and printing the Massachusetts Alternative Complaint for an Accounting which includes Egregious Acts with US Legal Forms. There are many specialist and condition-specific types you may use for your personal enterprise or person requirements.

Form popularity

FAQ

If you are not a member, you may not be able to participate in union elections or meetings, vote in collective bargaining ratification elections, or participate in other ?internal? union activities. However, you cannot be disciplined by the union for anything you do while not a member.

Employees may choose not to become union members and pay dues, or opt to pay only that share of dues used directly for representation, such as collective bargaining and contract administration. Known as objectors, they are no longer union members, but are still protected by the contract.

Membership in the union is up to you. By law you cannot be forced to join the union. But you will have to pay something to the union for its representation. These are called ?agency fees?.

Massachusetts has a right-to-work law, meaning that employees can choose whether or not they wish to join a union without impacting their ability to be employed. In Massachusetts, 12.6% of the wage and salary workers were union members in 2021, just higher than the federal average of 12%.

G.L. c. 215, § 34 provides: At the hearing of a complaint for civil contempt, the defendant shall have the burden of proving his or her inability to comply with the preexisting order or judgment of which the complaint alleges violation.

Opting out is your constitutional right. However, unions like AFT Massachusetts sometimes place restrictions on when they will accept opt-out requests.

The Massachusetts Law Component (MLC) The outlines will include summaries on 9 areas of law: Access to Justice; Anti-Discrimination Law; Business Organizations; Civil Procedure; Consumer Protection, G.L. c. 93A; Criminal Law and Procedure; Domestic Relations; Estates and Wills; and Evidence.

Right to Work laws do not outlaw labor unions, nor do they prevent any worker from joining a labor union if they voluntarily choose.