As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

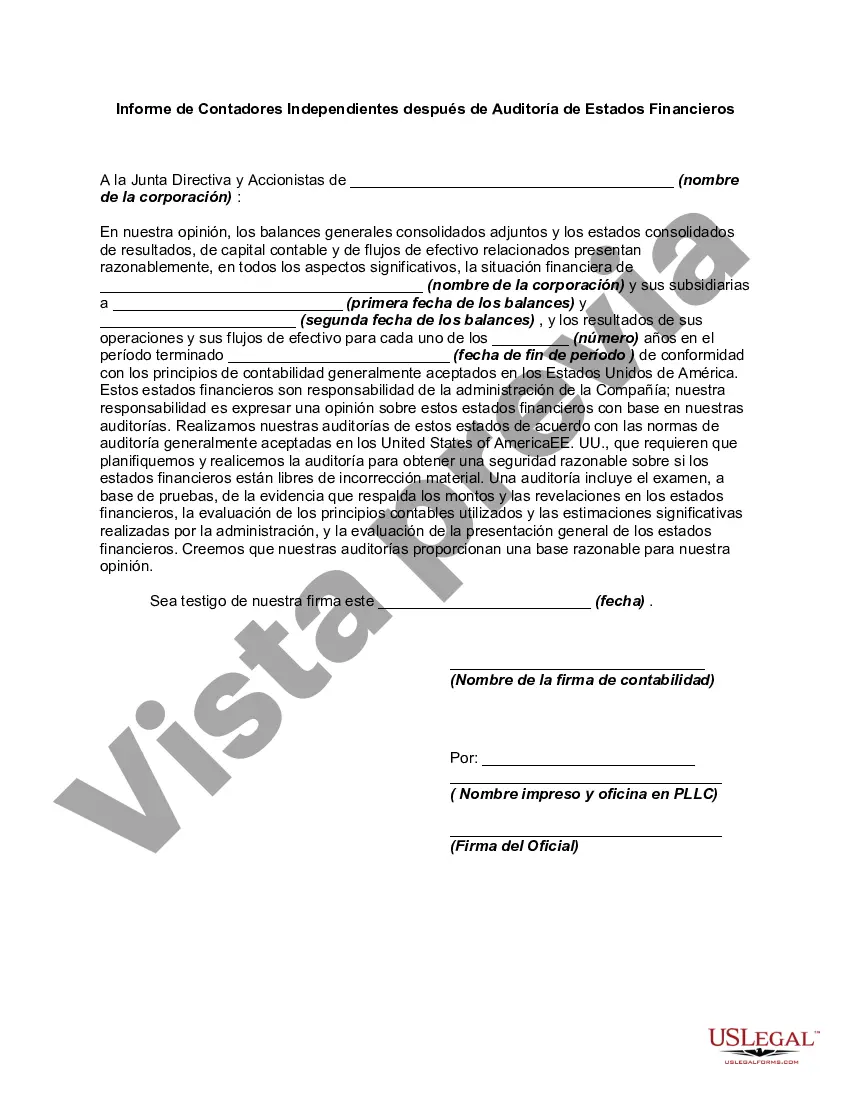

Maryland Report of Independent Accountants after Audit of Financial Statements is a comprehensive document prepared by independent accountants to give an authoritative assessment of the financial statements of an organization based in Maryland. This report is crucial for various stakeholders including shareholders, investors, lenders, and regulatory bodies to gain confidence in the financial health and integrity of the audited entity. The Maryland Report of Independent Accountants after Audit of Financial Statements contains a detailed analysis of the audited financial statements, providing a clear picture of the organization's financial position, performance, and cash flows. The report is prepared in accordance with generally accepted auditing standards (GAS) and often complies with relevant regulatory requirements such as the Maryland Business Corporation Act. Key components of the report typically include: 1. Introductory Paragraph: This section states the name of the audited organization, the period covered by the audit, and the responsibilities of management and the independent accountants. 2. Management's Responsibility: This part outlines management's responsibility for the preparation and fair presentation of the financial statements, as well as the design, implementation, and maintenance of internal controls. 3. Auditor's Responsibility: Here, the report highlights the independent accountants' responsibility to express an opinion on the fairness of the financial statements and the performance of the audit in accordance with GAS. 4. Opinion: The most crucial part of the report, this section presents the independent accountants' opinion on the financial statements. If the financial statements provide reliable and accurate information, the typical opinion is an "Unqualified Opinion," indicating that the statements are presented fairly and conform to accounting principles. Different types of Maryland Reports of Independent Accountants after Audit of Financial Statements can be classified based on the nature of the opinion expressed: 1. Unqualified Opinion: This is the most common and desirable opinion, indicating that the financial statements are presented fairly and provide a true and fair view of the audited entity's financial position. 2. Qualified Opinion: A qualified opinion suggests that the financial statements contain material misstatements or limitations in scope, but are otherwise fairly presented. The auditors detail the specific reasons for the qualification. 3. Adverse Opinion: An adverse opinion is issued when the financial statements are not presented fairly, have significant misstatements, or depart from generally accepted accounting principles to a degree that impacts the overall understanding of the statements. 4. Disclaimer of Opinion: In rare cases, the auditor may disclaim providing an opinion due to significant scope limitations, lack of supporting evidence, or uncertainties that prevent them from forming an opinion. These different types of opinions reflect the auditors' assessment of the reliability and accuracy of the financial statements and should be carefully considered by users of the report when making informed decisions related to the audited entity.Maryland Report of Independent Accountants after Audit of Financial Statements is a comprehensive document prepared by independent accountants to give an authoritative assessment of the financial statements of an organization based in Maryland. This report is crucial for various stakeholders including shareholders, investors, lenders, and regulatory bodies to gain confidence in the financial health and integrity of the audited entity. The Maryland Report of Independent Accountants after Audit of Financial Statements contains a detailed analysis of the audited financial statements, providing a clear picture of the organization's financial position, performance, and cash flows. The report is prepared in accordance with generally accepted auditing standards (GAS) and often complies with relevant regulatory requirements such as the Maryland Business Corporation Act. Key components of the report typically include: 1. Introductory Paragraph: This section states the name of the audited organization, the period covered by the audit, and the responsibilities of management and the independent accountants. 2. Management's Responsibility: This part outlines management's responsibility for the preparation and fair presentation of the financial statements, as well as the design, implementation, and maintenance of internal controls. 3. Auditor's Responsibility: Here, the report highlights the independent accountants' responsibility to express an opinion on the fairness of the financial statements and the performance of the audit in accordance with GAS. 4. Opinion: The most crucial part of the report, this section presents the independent accountants' opinion on the financial statements. If the financial statements provide reliable and accurate information, the typical opinion is an "Unqualified Opinion," indicating that the statements are presented fairly and conform to accounting principles. Different types of Maryland Reports of Independent Accountants after Audit of Financial Statements can be classified based on the nature of the opinion expressed: 1. Unqualified Opinion: This is the most common and desirable opinion, indicating that the financial statements are presented fairly and provide a true and fair view of the audited entity's financial position. 2. Qualified Opinion: A qualified opinion suggests that the financial statements contain material misstatements or limitations in scope, but are otherwise fairly presented. The auditors detail the specific reasons for the qualification. 3. Adverse Opinion: An adverse opinion is issued when the financial statements are not presented fairly, have significant misstatements, or depart from generally accepted accounting principles to a degree that impacts the overall understanding of the statements. 4. Disclaimer of Opinion: In rare cases, the auditor may disclaim providing an opinion due to significant scope limitations, lack of supporting evidence, or uncertainties that prevent them from forming an opinion. These different types of opinions reflect the auditors' assessment of the reliability and accuracy of the financial statements and should be carefully considered by users of the report when making informed decisions related to the audited entity.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.