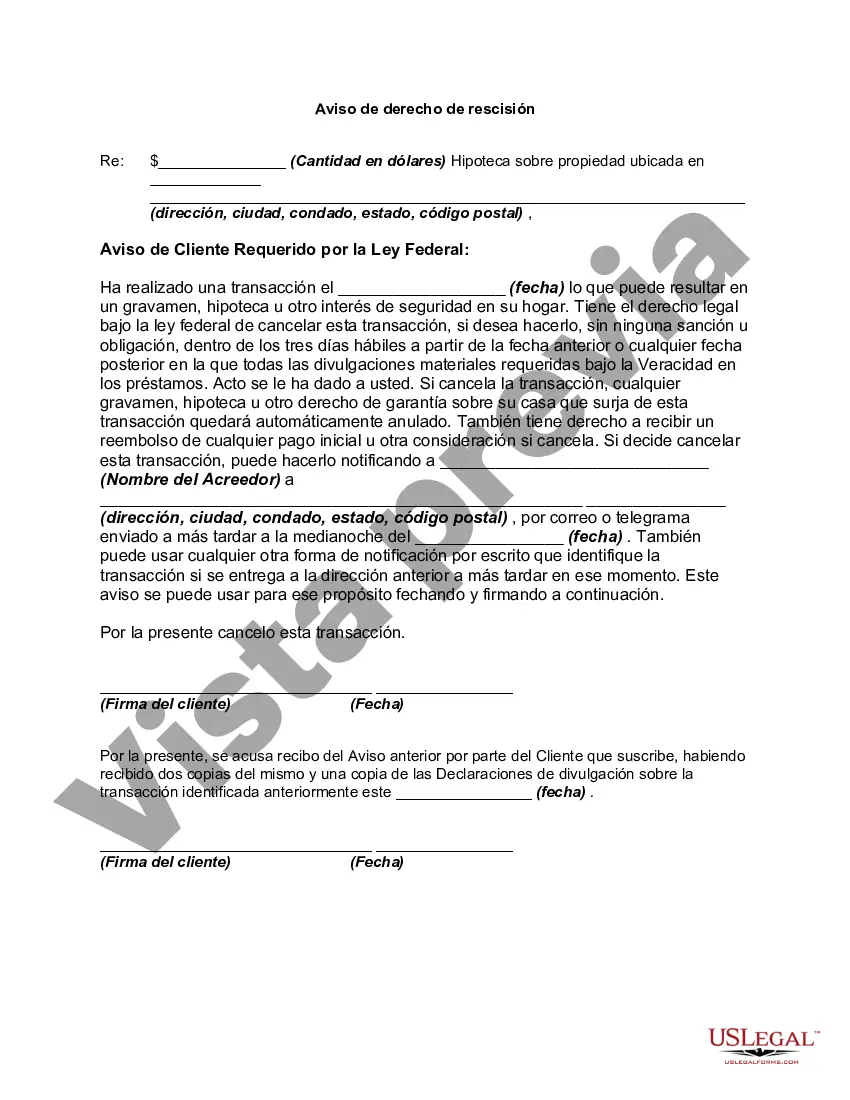

In a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership is or will be subject to the security interest has the right to rescind the transaction. Lenders are required to deliver two copies of the notice of the right to rescind and one copy of the disclosure statement to each consumer entitled to rescind. The notice must be on a separate document that identifies the rescission period on the transaction and must clearly and conspicuously:

" disclose the retention or acquisition of a security interest in the consumer's principal dwelling;

" the consumer's right to rescind the transaction; and

" how the consumer may exercise the right to rescind with a form for that purpose.

The Maryland Right to Rescind is a legal provision that grants consumers the power to cancel a contract or loan agreement when a security interest in their primary residence is at stake. Rescission allows individuals to undo a transaction and return to the status quo before the agreement was signed. This vital safeguard helps protect homeowners from coercive or unfavorable lending practices. When it comes to the different types of Maryland Right to Rescind, they can be categorized based on the circumstances in which they can be exercised: 1. Predatory Lending Rescission: This type of rescission is applicable in situations where homeowners are victims of predatory lending practices, such as false or misleading information, unfair terms, or excessive fees. The Maryland Right to Rescind empowers these consumers to escape these exploitative agreements. 2. Non-Disclosure Rescission: If a lender fails to disclose material information about the loan terms or conditions, the Maryland Right to Rescind enables the borrower to cancel the agreement. Non-disclosure can involve hiding crucial details about interest rates, payment schedules, or prepayment penalties. 3. Unlawful Lending Rescission: In instances where the lender violates Maryland's lending regulations, borrowers have the right to rescind. This includes situations where the lender is unregistered, operates without a license, or engages in fraud. 4. Violation of Truth in Lending Act (TILL) Rescission: In Maryland, borrowers also have the option to rescind if the lender fails to comply with the Truth in Lending Act (TILL). The act mandates that lenders disclose accurate and complete information about loan terms, including annual percentage rates (APR), finance charges, and payment obligations. 5. Home Equity Loan Rescission: Homeowners who enter into home equity loans or lines of credit secured by their principal dwelling also benefit from the Maryland Right to Rescind. If they change their minds within three business days of signing the agreement, they can cancel the loan. Overall, the Maryland Right to rescind when a security interest in a consumer's principal dwelling is involved rescissionio— - provides crucial protection to Maryland residents, ensuring fair and transparent lending practices. It serves as a valuable tool for borrowers to undo agreements marred by predatory behavior, non-disclosure, unlawful lending, violations of TILL, or home equity loan arrangements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.