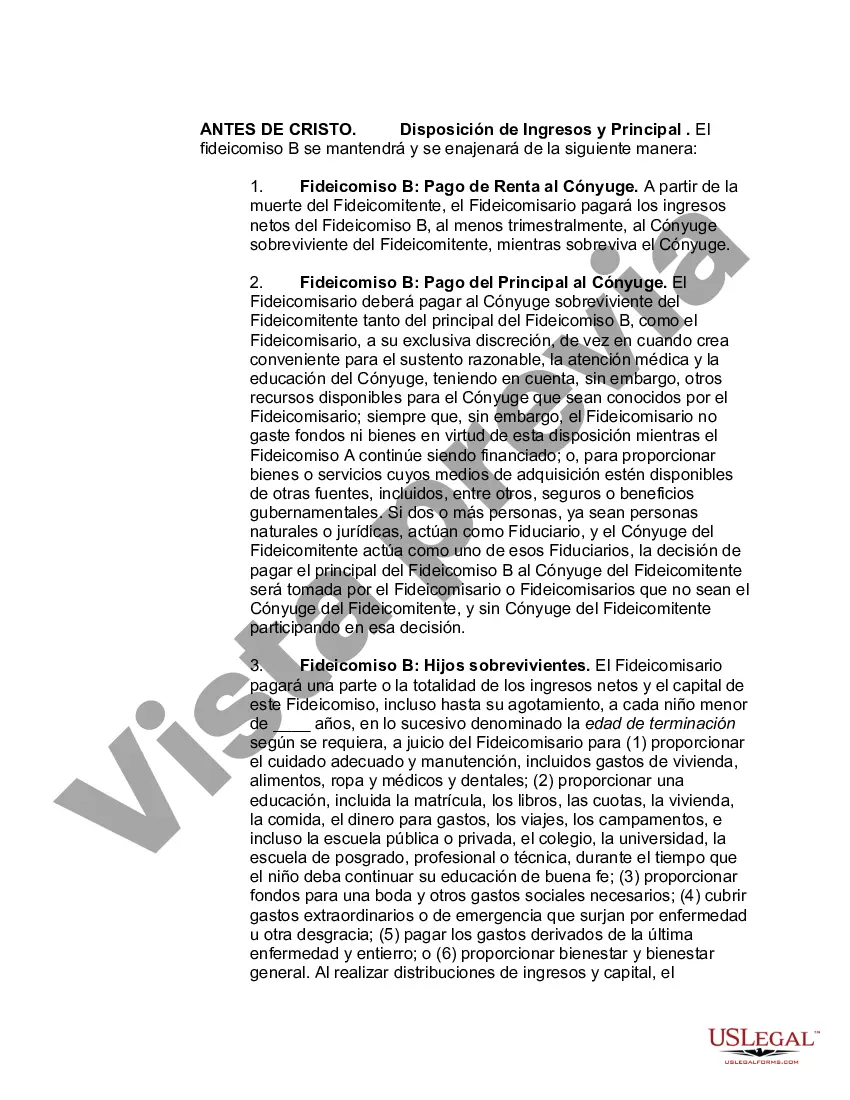

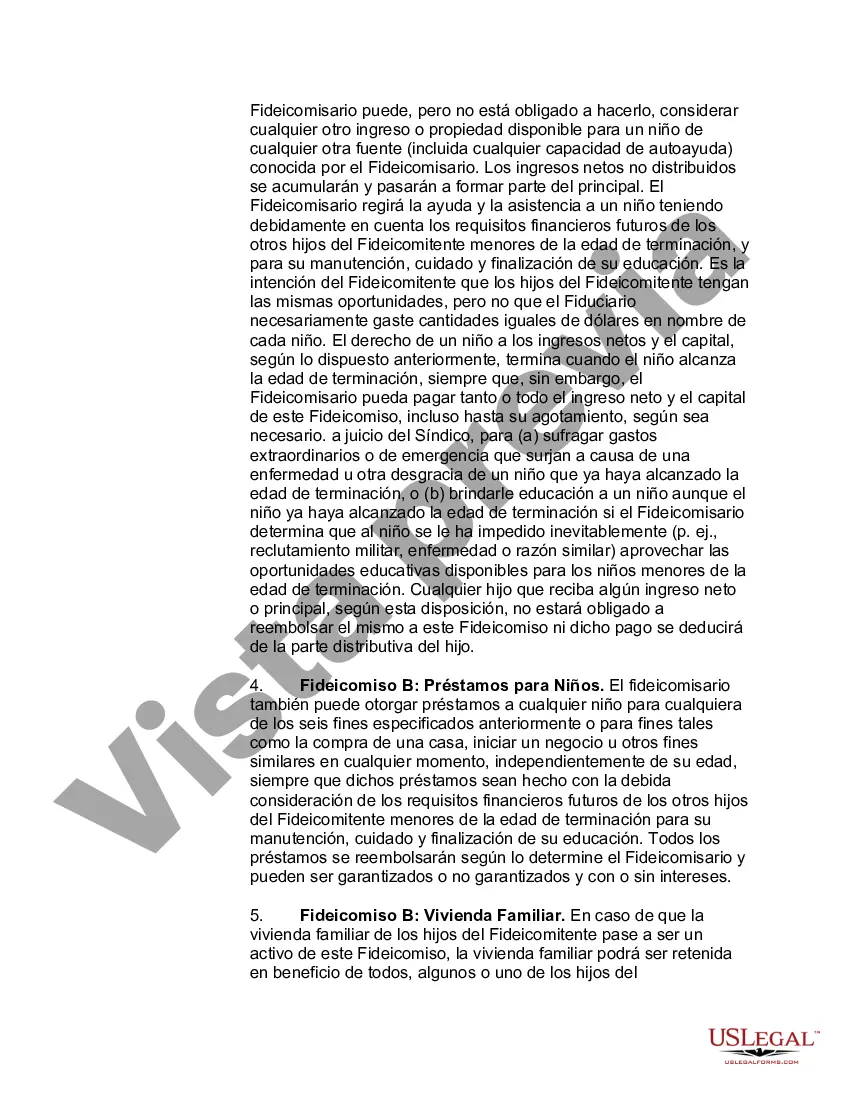

An A-B trust is a revocable living trust which divides into two trusts upon the death of the first spouse. This type of trust makes use of both the estate tax exemption ($3.5 million per person in 2009) and the marital deduction to make it so that no estate taxes are due upon the death of the first spouse. The B Trust is also known as the Bypass trust and it contains the amount of that years applicable exclusion amount. The A trust is the marital deduction trust which will typically contain both the surviving spouse's separate property and one half community property interests but also the residue of the deceased spouse's estate after the estate tax exemption has been utilized by the B trust. The use of an A-B trust ensures that both spouse's applicable exclusion amounts are effectively used, thereby doubling the amount of property which can pass to heirs free of Federal Estate Taxes.

A Maine Marital Deduction Trust, also known as Trust A, is a specific type of trust created to take advantage of the marital deduction in estate planning. It enables a married couple to maximize the amount of assets they can leave to their surviving spouse without incurring estate taxes. Trust A is typically established upon the death of the first spouse. Trust A is funded with an amount equal to or less than the value of the federal estate tax exemption at the time of the first spouse's passing. This threshold is currently $11.7 million in 2021. By utilizing Trust A, the assets placed into the trust are excluded from the taxable estate of the surviving spouse upon their death. The Bypass Trust, also known as Trust B or the credit shelter trust, complements Trust A and is established simultaneously. It is funded with the remaining assets of the deceased spouse's estate after funding Trust A or with any assets that exceed the federal estate tax exemption. Trust B aims to use the deceased spouse's estate tax exemption to minimize estate taxes upon the death of the surviving spouse. The Bypass Trust B offers several benefits, including: 1. Estate Tax Minimization: By utilizing the first spouse's estate tax exemption, Trust B allows the couple to pass a more substantial portion of their wealth to future generations without incurring estate taxes. 2. Asset Protection: Assets placed in Trust B are shielded from estate taxes in both spouses' estates, protecting them from potential creditors and ensuring they pass to designated beneficiaries. 3. Provision for Surviving Spouse: While Trust B focuses on preserving assets for future generations, it can also provide income and support for the surviving spouse during their lifetime. 4. Control over Beneficiaries: Through Trust B, the couple can dictate how their assets will be distributed to beneficiaries, ensuring their wishes are carried out even after both spouses have passed away. It is important to note that tax laws and regulations are subject to change, potentially altering the limits and requirements. Therefore, consulting with a qualified estate planning attorney or financial advisor is crucial to understanding and implementing these trusts effectively. Other variations and combinations of marital deduction trusts may exist, such as Qualified Terminable Interest Property (TIP) trusts and Charitable Remainder Unit rusts (Cuts). These trusts cater to specific estate planning goals, such as providing income for a surviving spouse or charitable giving while still benefiting from the marital deduction. As always, seeking professional advice tailored to individual circumstances is essential for making informed decisions regarding estate planning strategies.A Maine Marital Deduction Trust, also known as Trust A, is a specific type of trust created to take advantage of the marital deduction in estate planning. It enables a married couple to maximize the amount of assets they can leave to their surviving spouse without incurring estate taxes. Trust A is typically established upon the death of the first spouse. Trust A is funded with an amount equal to or less than the value of the federal estate tax exemption at the time of the first spouse's passing. This threshold is currently $11.7 million in 2021. By utilizing Trust A, the assets placed into the trust are excluded from the taxable estate of the surviving spouse upon their death. The Bypass Trust, also known as Trust B or the credit shelter trust, complements Trust A and is established simultaneously. It is funded with the remaining assets of the deceased spouse's estate after funding Trust A or with any assets that exceed the federal estate tax exemption. Trust B aims to use the deceased spouse's estate tax exemption to minimize estate taxes upon the death of the surviving spouse. The Bypass Trust B offers several benefits, including: 1. Estate Tax Minimization: By utilizing the first spouse's estate tax exemption, Trust B allows the couple to pass a more substantial portion of their wealth to future generations without incurring estate taxes. 2. Asset Protection: Assets placed in Trust B are shielded from estate taxes in both spouses' estates, protecting them from potential creditors and ensuring they pass to designated beneficiaries. 3. Provision for Surviving Spouse: While Trust B focuses on preserving assets for future generations, it can also provide income and support for the surviving spouse during their lifetime. 4. Control over Beneficiaries: Through Trust B, the couple can dictate how their assets will be distributed to beneficiaries, ensuring their wishes are carried out even after both spouses have passed away. It is important to note that tax laws and regulations are subject to change, potentially altering the limits and requirements. Therefore, consulting with a qualified estate planning attorney or financial advisor is crucial to understanding and implementing these trusts effectively. Other variations and combinations of marital deduction trusts may exist, such as Qualified Terminable Interest Property (TIP) trusts and Charitable Remainder Unit rusts (Cuts). These trusts cater to specific estate planning goals, such as providing income for a surviving spouse or charitable giving while still benefiting from the marital deduction. As always, seeking professional advice tailored to individual circumstances is essential for making informed decisions regarding estate planning strategies.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.