Maine Senior Debt Term Sheet

Description

How to fill out Senior Debt Term Sheet?

If you want to total, acquire, or produce authorized document templates, use US Legal Forms, the biggest collection of authorized varieties, which can be found on the web. Utilize the site`s basic and practical search to get the paperwork you need. Various templates for company and person purposes are categorized by categories and suggests, or keywords. Use US Legal Forms to get the Maine Senior Debt Term Sheet with a handful of mouse clicks.

Should you be currently a US Legal Forms consumer, log in for your bank account and then click the Acquire switch to get the Maine Senior Debt Term Sheet. You can also entry varieties you in the past delivered electronically inside the My Forms tab of your bank account.

Should you use US Legal Forms for the first time, follow the instructions beneath:

- Step 1. Ensure you have chosen the form to the correct area/country.

- Step 2. Use the Review choice to examine the form`s content material. Do not neglect to see the outline.

- Step 3. Should you be unhappy using the develop, use the Look for area near the top of the display screen to get other models of your authorized develop format.

- Step 4. When you have identified the form you need, select the Get now switch. Pick the pricing strategy you like and add your references to register for the bank account.

- Step 5. Method the transaction. You may use your bank card or PayPal bank account to perform the transaction.

- Step 6. Select the formatting of your authorized develop and acquire it on your system.

- Step 7. Complete, edit and produce or signal the Maine Senior Debt Term Sheet.

Every single authorized document format you purchase is the one you have permanently. You may have acces to every develop you delivered electronically in your acccount. Go through the My Forms area and decide on a develop to produce or acquire once more.

Compete and acquire, and produce the Maine Senior Debt Term Sheet with US Legal Forms. There are many specialist and express-specific varieties you may use for your personal company or person requirements.

Form popularity

FAQ

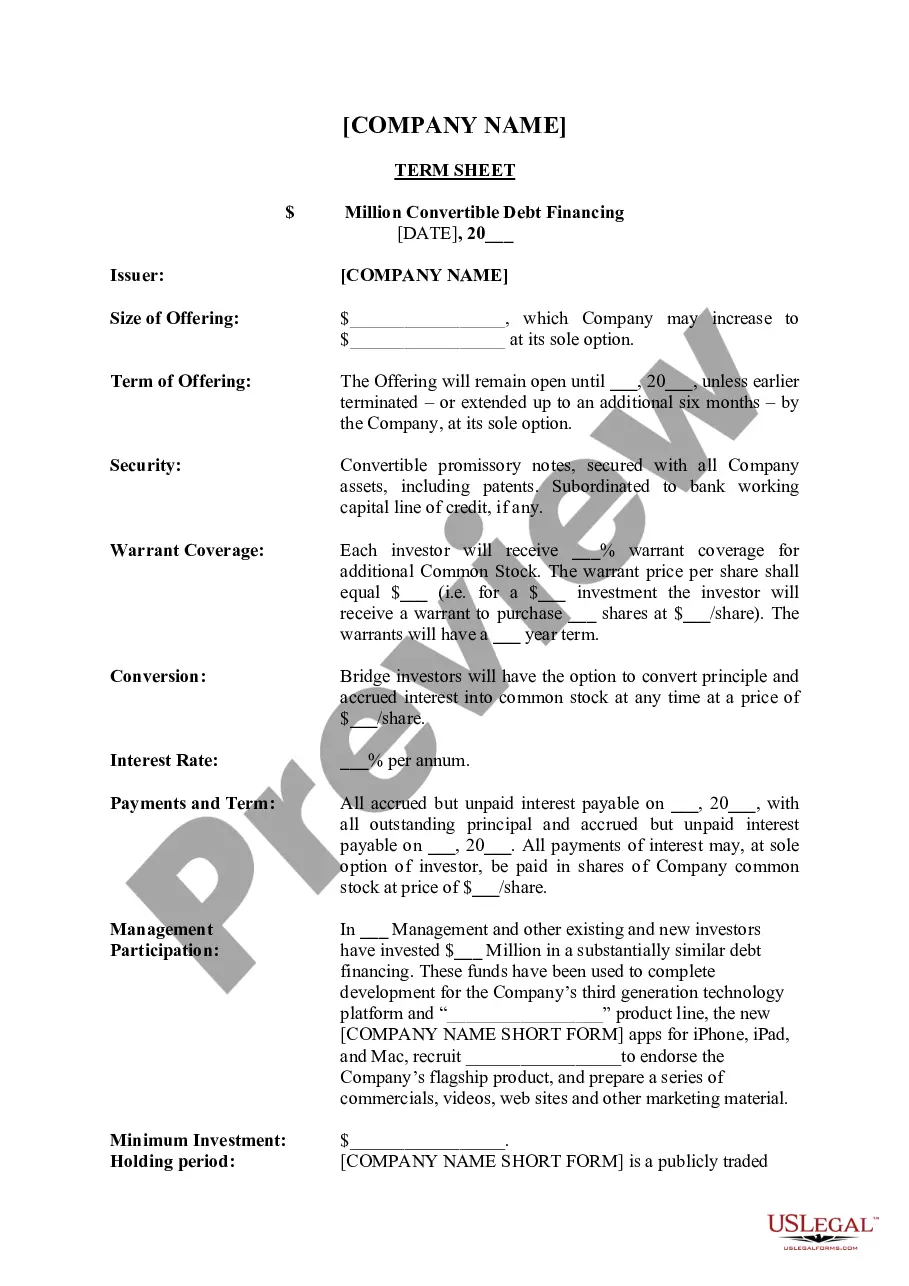

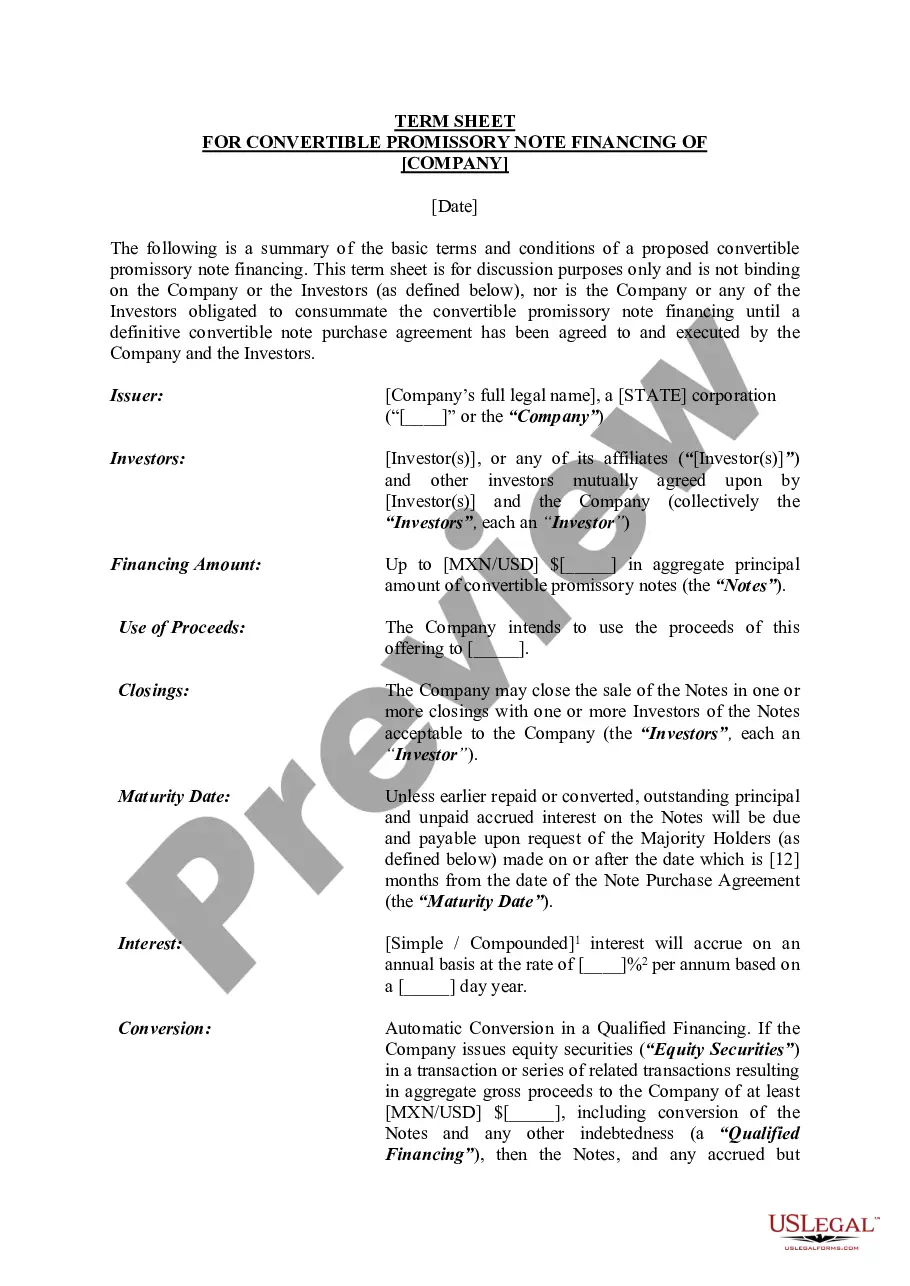

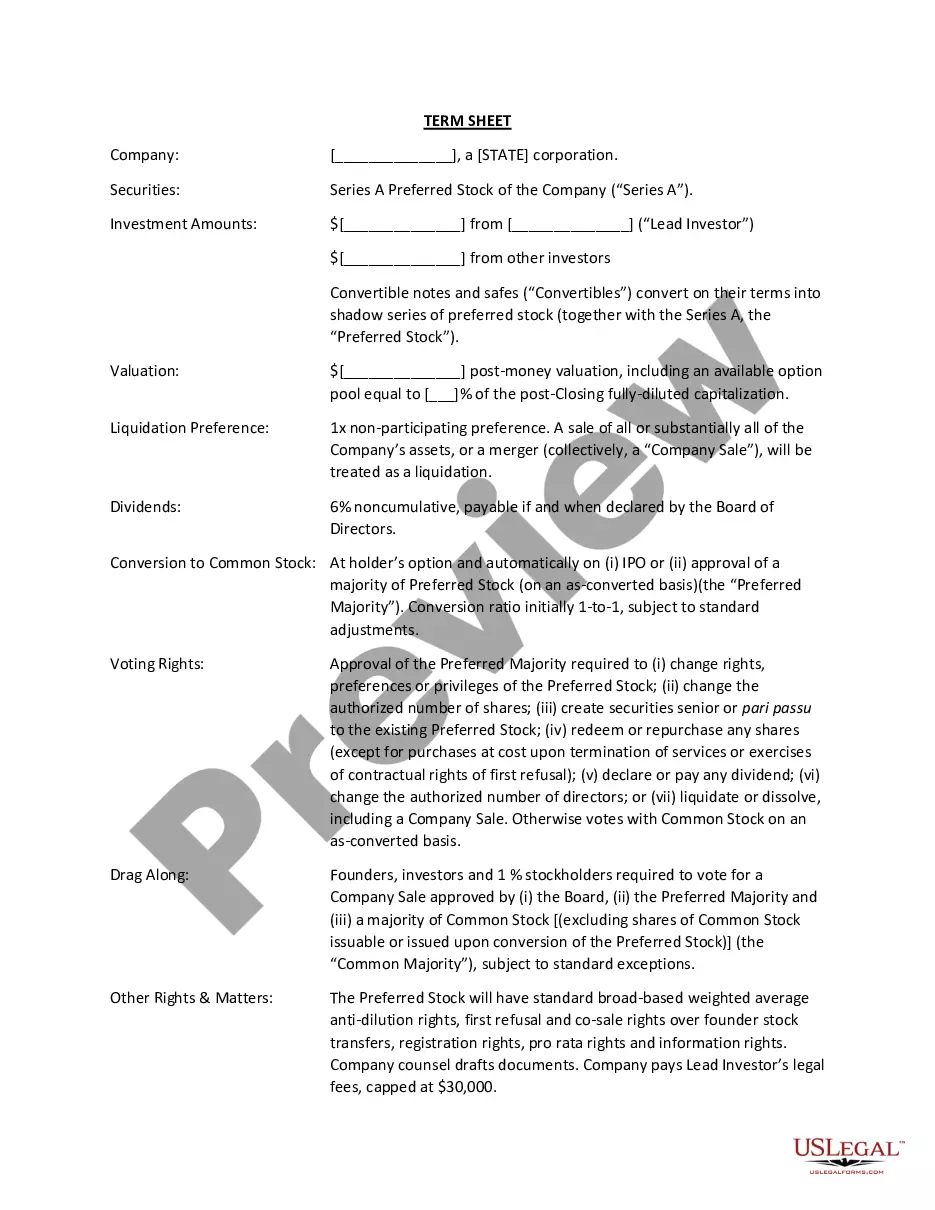

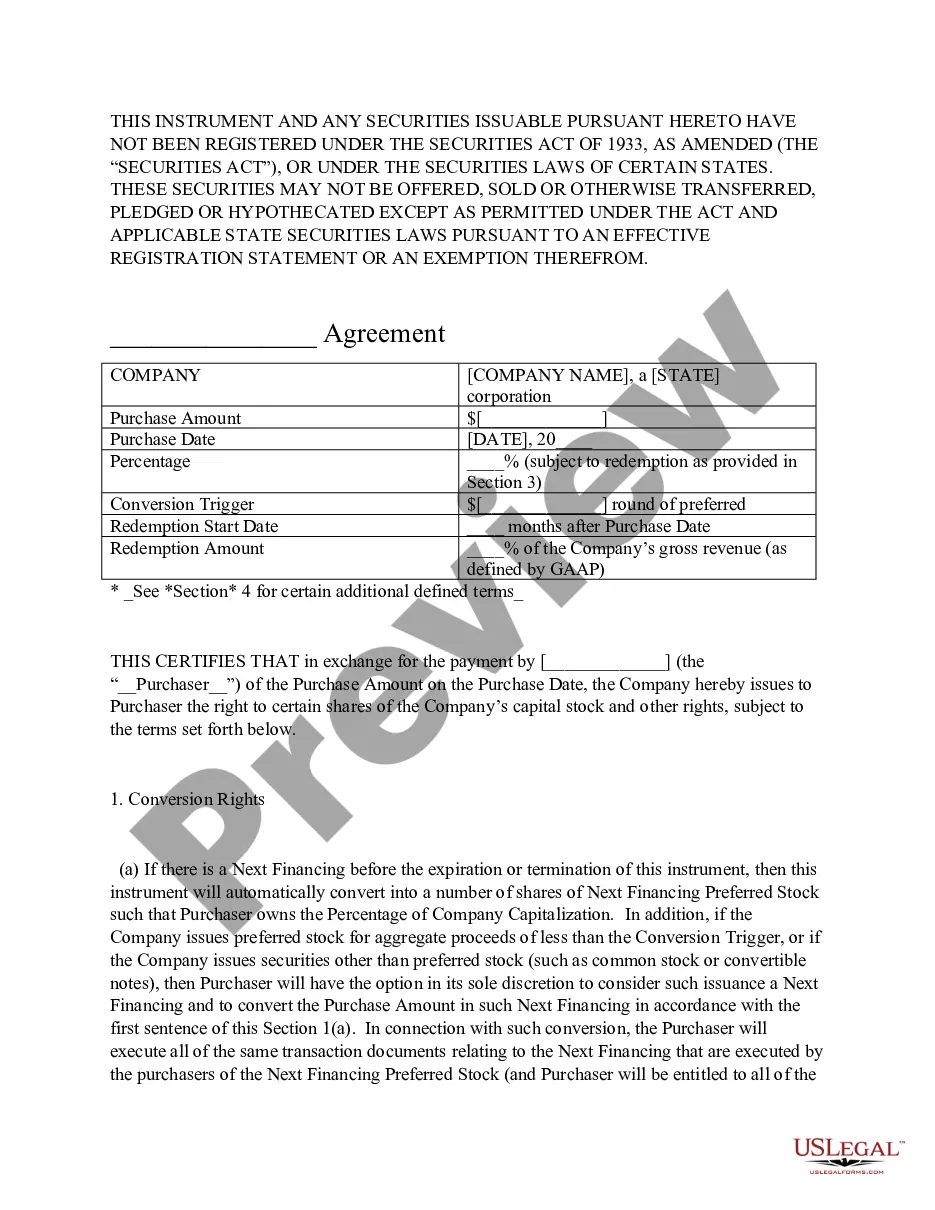

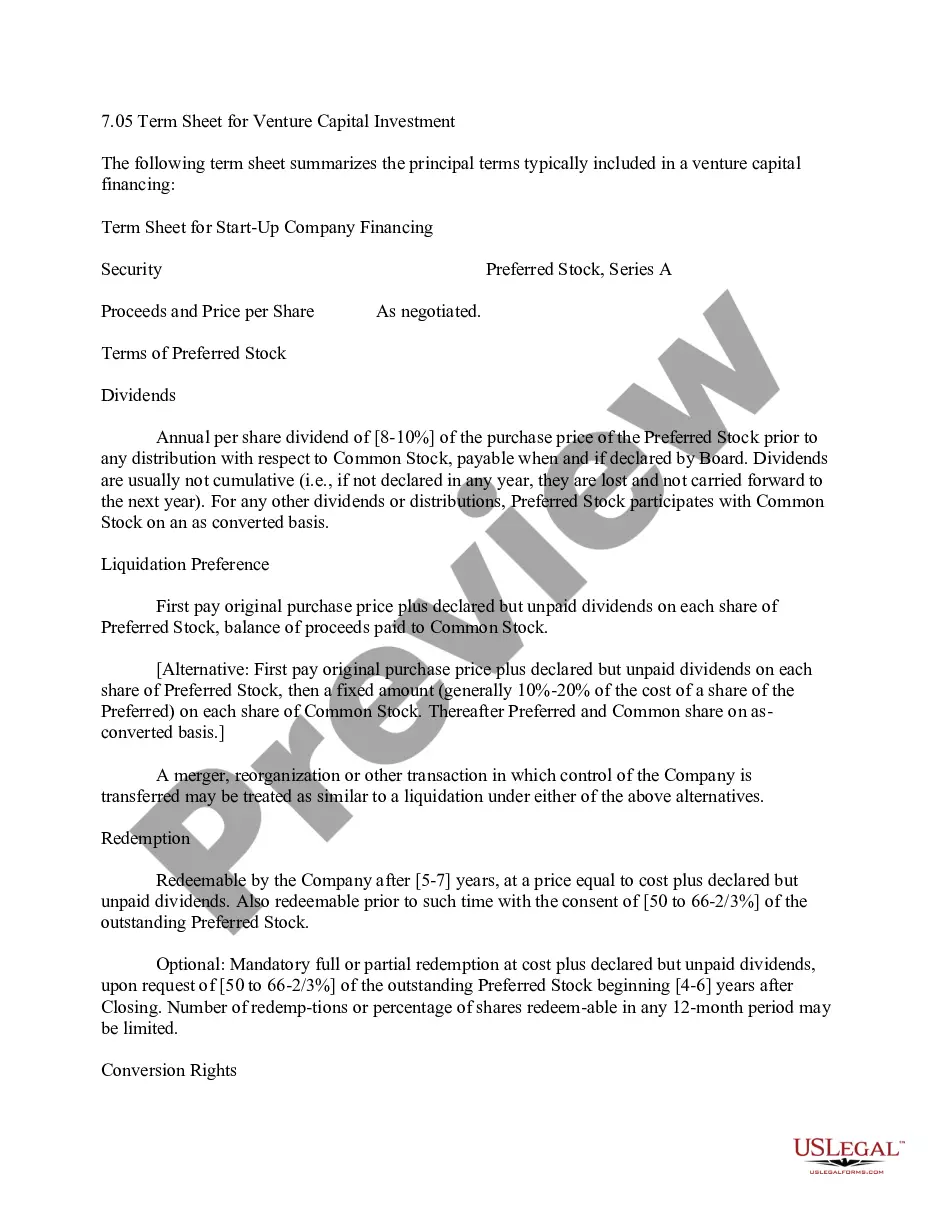

Elements of a Term Sheet General Information. The top of a term sheet will outline general information such as the company name, investor name, date, and currency of the transaction. Amount. This section provides the amount of funding the investor and investee have tentatively agreed upon. ... Structure. ... Interest Rate.

Hear this out loud PauseVenture debt is a term loan typically structured over a four-to-five-year amortization period, usually with a period of time to draw the loan down, such as 9-12 months. Interest-only periods of 3-12 months are common.

Most venture debt takes the form of a growth capital term loan. These loans usually have to be repaid within three to four years, but they often start out with a 6- to 12-month interest-only (I/O) period. During the I/O period, the company pays accrued interest, but not principal.

VC term sheets typically include the amount of money being raised, the types of securities involved, the company's valuation before and after the investment, the investor's liquidation preferences, voting rights, board representation, and so much more.

If you are, you might see a term sheet soon. This is a nonbinding agreement that a venture debt lender will give you when they're considering an investment in your company. This sheet will set the terms of your deal, including the size of your loan, your interest rate, and the warrants that your lender will take.

Covenants: A Promise of Performance If you accept venture debt financing with a covenant arrangement, you may be required to maintain a certain level of new subscribers or monthly recurring revenue while also keeping your burn and churn rates down. These metrics might be evaluated on a monthly or quarterly basis.