The "look through" trust can affords long term IRA deferrals and special protection or tax benefits for the family. But, as with all specialized tools, you must use it only in the right situation. If the IRA participant names a trust as beneficiary, and the trust meets certain requirements, for purposes of calculating minimum distributions after death, one can "look through" the trust and treat the trust beneficiary as the designated beneficiary of the IRA. You can then use the beneficiary's life expectancy to calculate minimum distributions. Were it not for this "look through" rule, the IRA or plan assets would have to be paid out over a much shorter period after the owner's death, thereby losing long term deferral.

Michigan Irrevocable Trust as Designated Beneficiary of an Individual Retirement Account: A Michigan Irrevocable Trust as a Designated Beneficiary of an Individual Retirement Account (IRA) is a legal arrangement where an Irrevocable Trust based in the state of Michigan is named as the beneficiary of an individual's IRA. An IRA is a type of retirement account that provides individuals with tax advantages for their savings. By naming an Irrevocable Trust as the beneficiary of an IRA, individuals can ensure that their retirement savings are distributed and managed according to their wishes, even after their passing. This trust arrangement allows for long-term control and protection of the assets within the IRA while granting flexibility and benefits to the designated beneficiaries. There are different types of Michigan Irrevocable Trusts that can be named as beneficiaries of an IRA, including: 1. Charitable Remainder Trusts: These trusts allow individuals to leave a portion or all of their IRA assets to a charity of their choice while providing income payments to beneficiaries for a specified period. 2. Special Needs Trusts: These trusts are designed to benefit individuals with disabilities by preserving their eligibility for government assistance programs while providing supplemental support from the IRA assets. 3. Life Insurance Trusts: These trusts use the proceeds from the IRA to fund life insurance policies, allowing individuals to provide for their beneficiaries' financial needs after their passing. 4. Family Trusts: These trusts focus on providing financial stability and asset protection for future generations of a family. They can include provisions for distributing IRA assets to family members based on specific criteria or conditions. It is important to note that creating and managing a Michigan Irrevocable Trust as a Designated Beneficiary of an IRA requires careful consideration and guidance from legal and financial professionals. This ensures compliance with Michigan state laws, tax regulations, and individual goals for asset distribution and protection. By utilizing a Michigan Irrevocable Trust as the designated beneficiary of an IRA, individuals can better control the distribution of their retirement savings, protect the assets from creditors or lawsuits, reduce estate taxes, and leave a lasting legacy for their loved ones or chosen charitable organizations.Michigan Irrevocable Trust as Designated Beneficiary of an Individual Retirement Account: A Michigan Irrevocable Trust as a Designated Beneficiary of an Individual Retirement Account (IRA) is a legal arrangement where an Irrevocable Trust based in the state of Michigan is named as the beneficiary of an individual's IRA. An IRA is a type of retirement account that provides individuals with tax advantages for their savings. By naming an Irrevocable Trust as the beneficiary of an IRA, individuals can ensure that their retirement savings are distributed and managed according to their wishes, even after their passing. This trust arrangement allows for long-term control and protection of the assets within the IRA while granting flexibility and benefits to the designated beneficiaries. There are different types of Michigan Irrevocable Trusts that can be named as beneficiaries of an IRA, including: 1. Charitable Remainder Trusts: These trusts allow individuals to leave a portion or all of their IRA assets to a charity of their choice while providing income payments to beneficiaries for a specified period. 2. Special Needs Trusts: These trusts are designed to benefit individuals with disabilities by preserving their eligibility for government assistance programs while providing supplemental support from the IRA assets. 3. Life Insurance Trusts: These trusts use the proceeds from the IRA to fund life insurance policies, allowing individuals to provide for their beneficiaries' financial needs after their passing. 4. Family Trusts: These trusts focus on providing financial stability and asset protection for future generations of a family. They can include provisions for distributing IRA assets to family members based on specific criteria or conditions. It is important to note that creating and managing a Michigan Irrevocable Trust as a Designated Beneficiary of an IRA requires careful consideration and guidance from legal and financial professionals. This ensures compliance with Michigan state laws, tax regulations, and individual goals for asset distribution and protection. By utilizing a Michigan Irrevocable Trust as the designated beneficiary of an IRA, individuals can better control the distribution of their retirement savings, protect the assets from creditors or lawsuits, reduce estate taxes, and leave a lasting legacy for their loved ones or chosen charitable organizations.

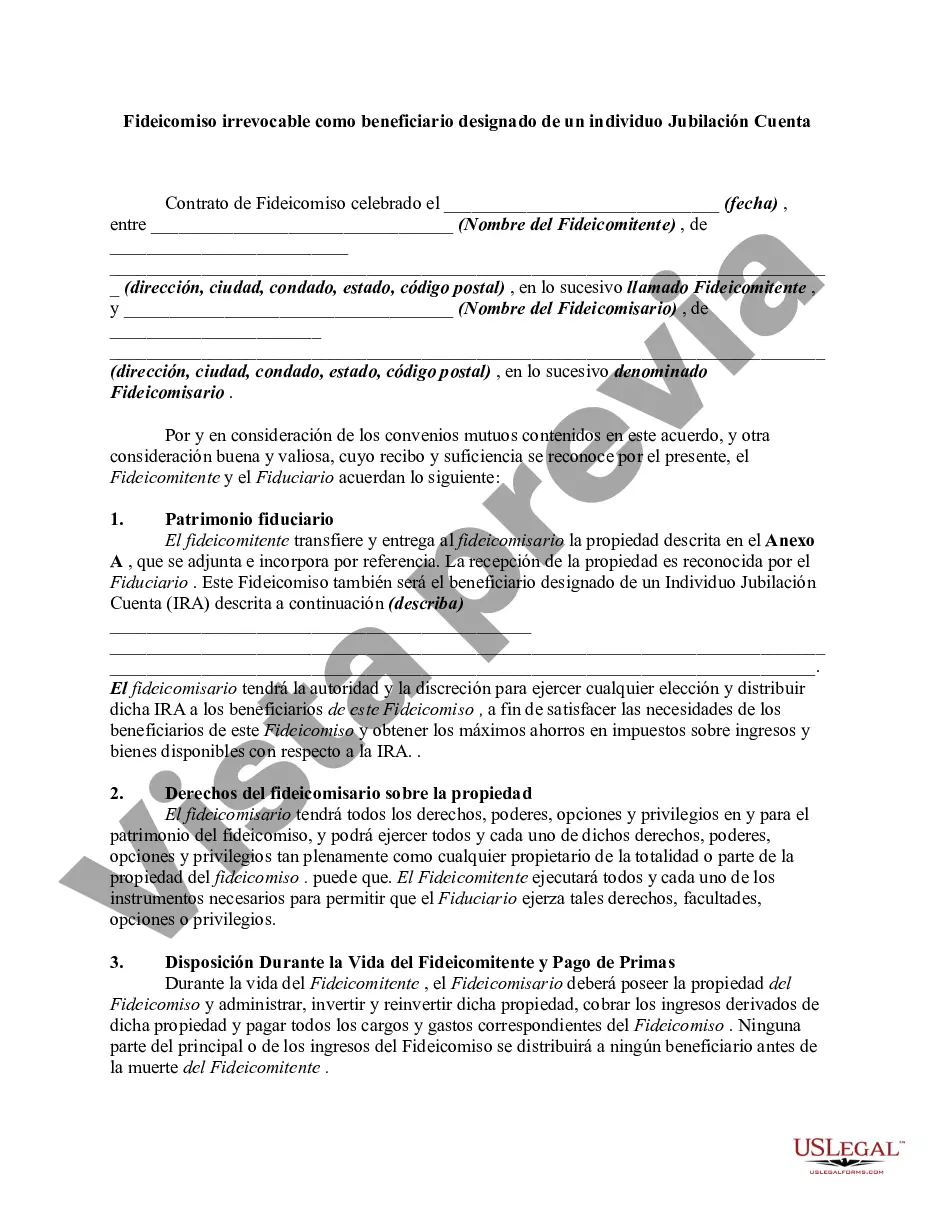

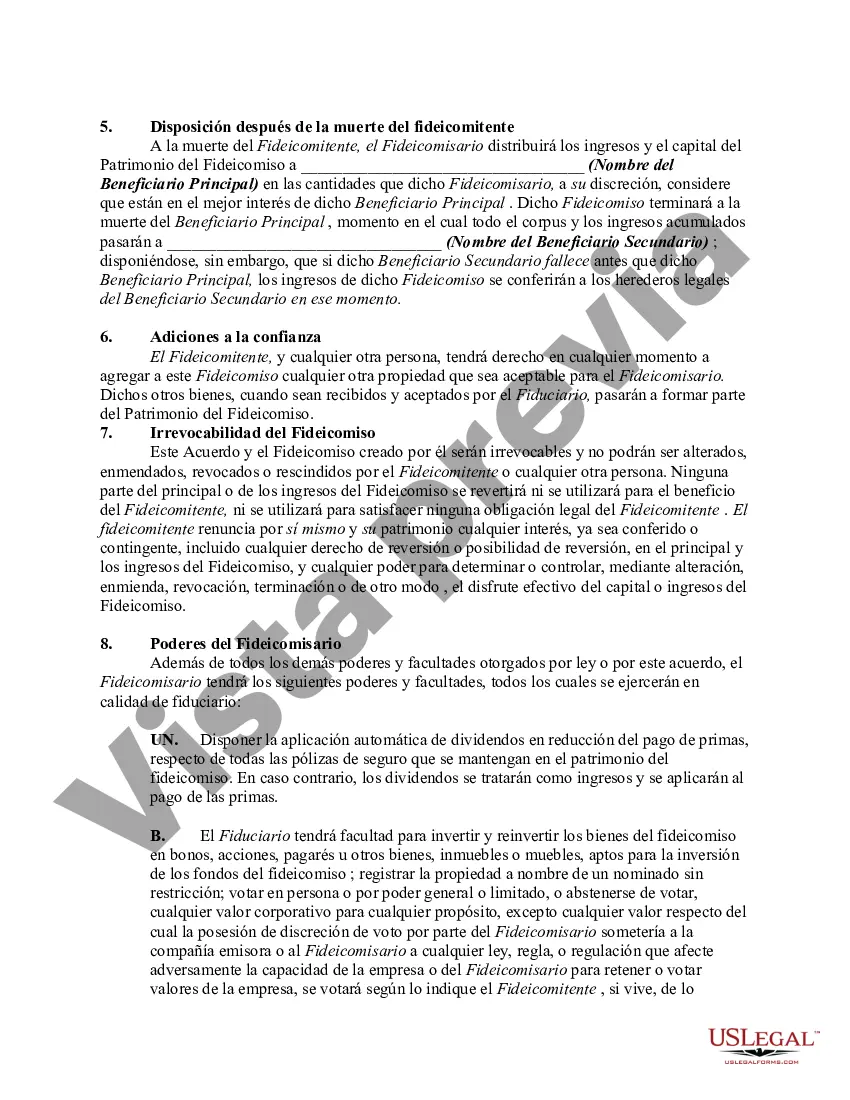

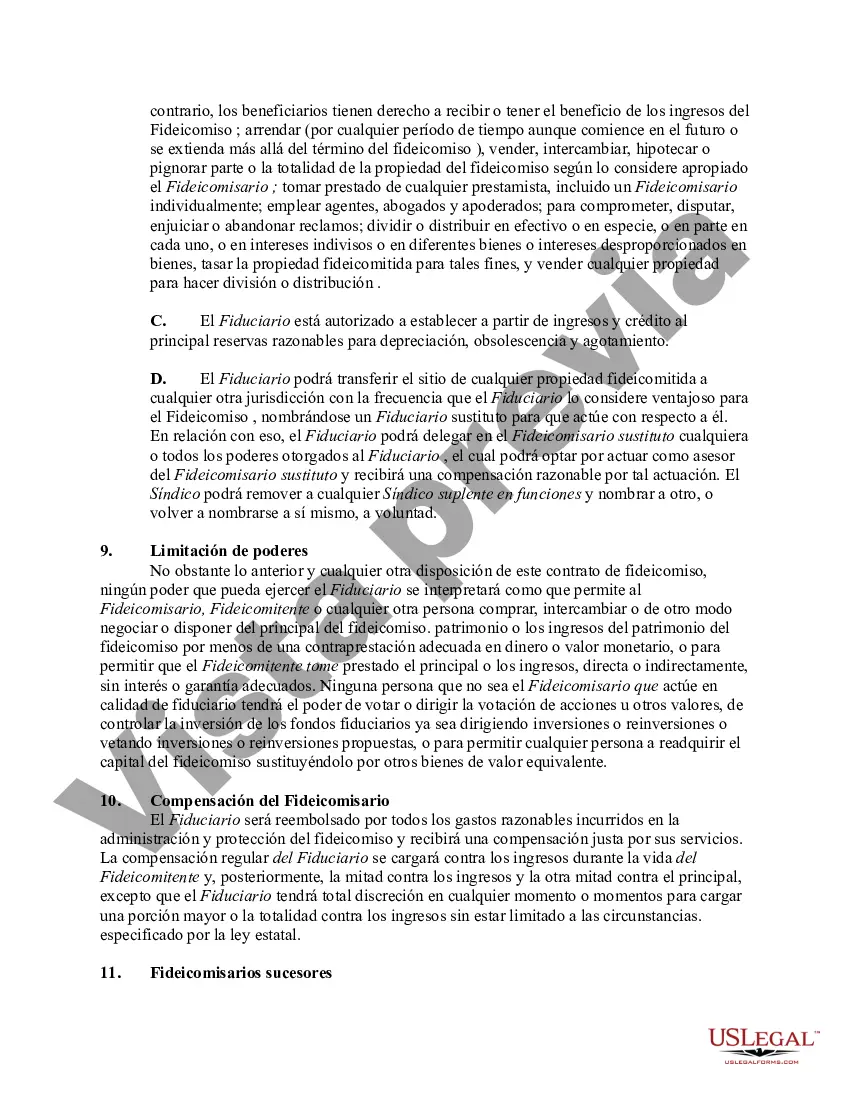

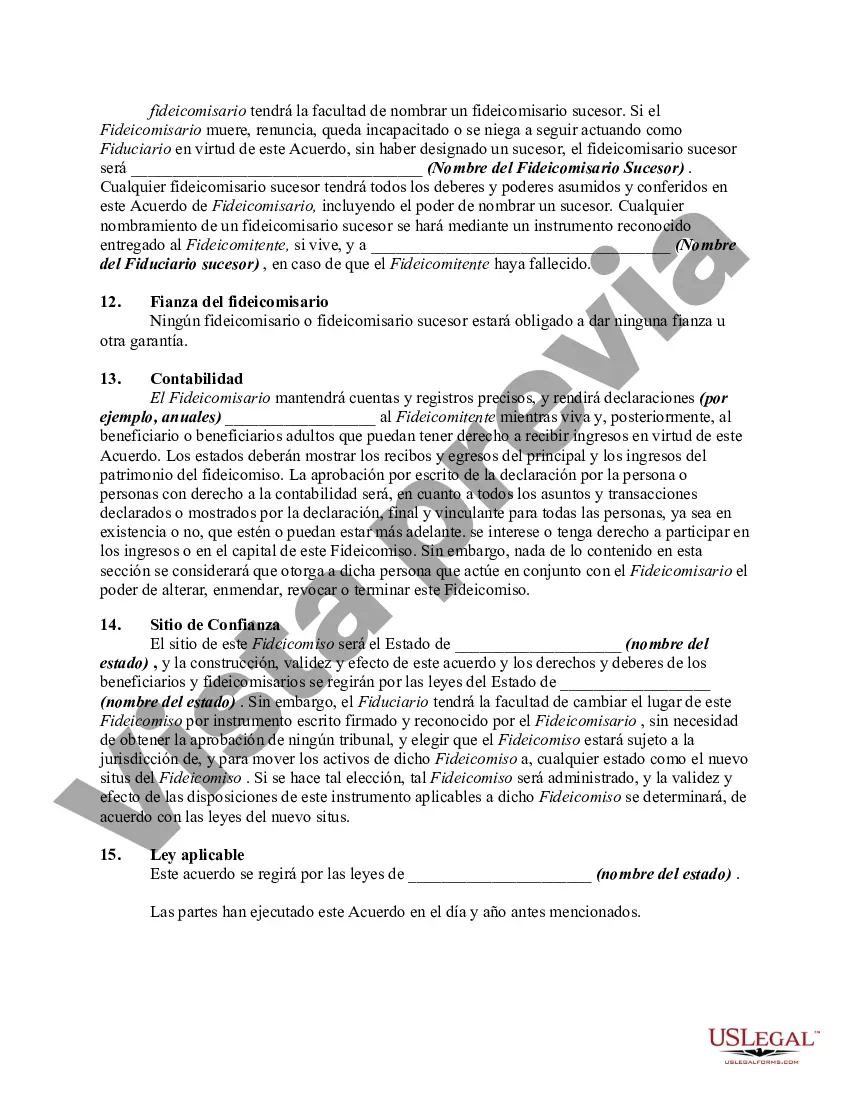

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.