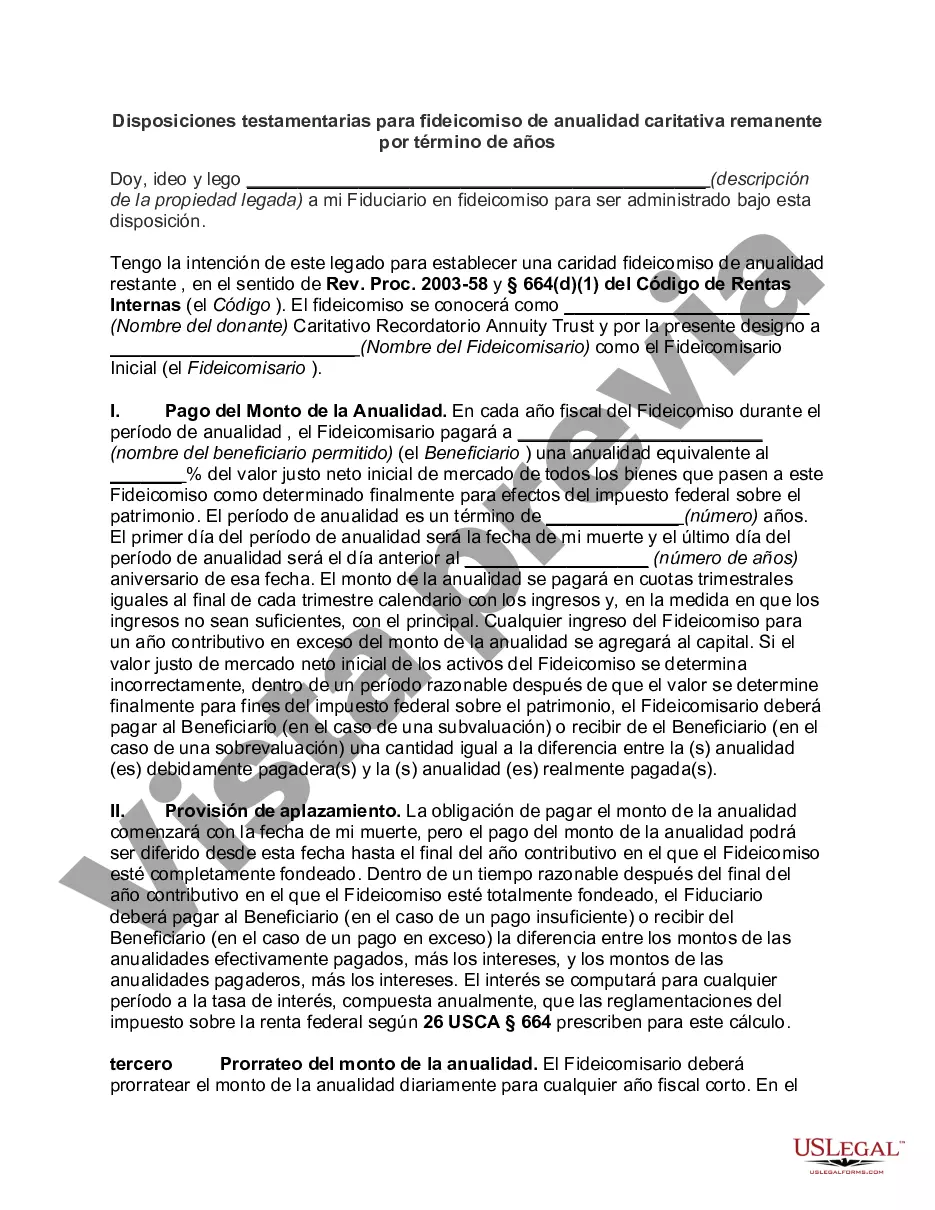

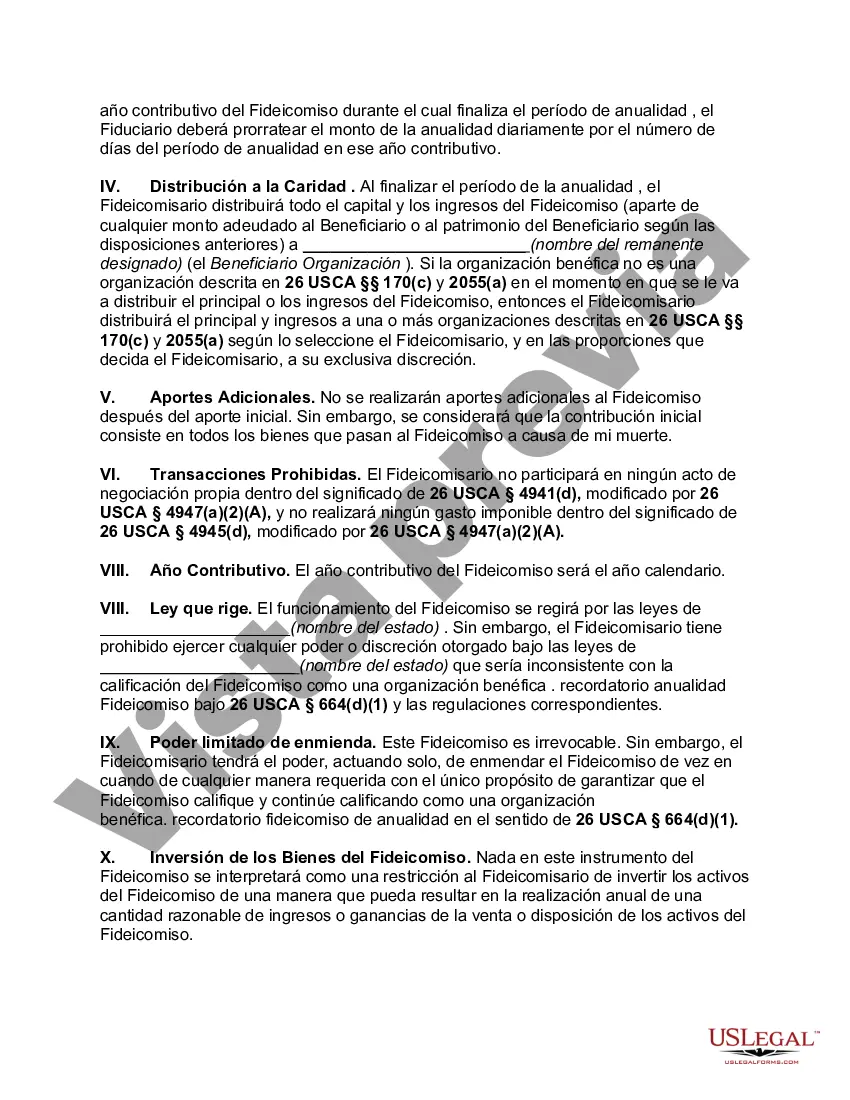

Michigan testamentary provisions refer to the specific guidelines and regulations set forth by the state of Michigan regarding testamentary trusts. In the context of charitable remainder annuity trusts for a term of years, Michigan provides various provisions to ensure the proper administration and distribution of assets to charitable beneficiaries. A charitable remainder annuity trust is a type of irrevocable trust established by a donor in order to provide income to a non-charitable beneficiary for a specified term of years, with the remaining assets passing to a designated charitable organization at the end of the term. Michigan's testamentary provisions for charitable remainder annuity trusts for a term of years includes: 1. Uniform Management of Institutional Funds Act (UMI FA): Michigan adheres to UMI FA, which establishes rules for the investment and management of charitable assets. This act sets guidelines for prudent investment practices, spending rates, and asset allocation to ensure the long-term sustainability of charitable organizations. 2. Charitable Trust Act: Michigan’s Charitable Trust Act provides legal and administrative requirements for establishing and managing charitable trusts, including charitable remainder annuity trusts. This act outlines the trustee’s duties, reporting requirements, and restrictions on the use of charitable assets. 3. Termination Provisions: Michigan allows the establishment of charitable remainder annuity trusts for a term of years, meaning the trust's duration is predefined. At the end of the term, the remaining trust assets are transferred to the designated charitable beneficiary, in accordance with the donor's instructions. 4. Charitable Deductions: Under Michigan law, donors who create charitable remainder annuity trusts may be eligible for certain tax deductions. These deductions can help reduce the donor's taxable income, providing potential benefits for both the donor and the designated charitable organization. 5. Restricted Beneficiaries: Michigan testamentary provisions may allow donors to specify the eligible non-charitable beneficiaries who will receive income payments from the trust during the term of years. These beneficiaries could include family members, friends, or other individuals chosen by the donor. 6. Trustee Requirements: Michigan's provisions require the appointment of a trustee to oversee the administration of the charitable remainder annuity trust. The trustee has fiduciary duties, including managing the trust assets, making income distributions to the non-charitable beneficiaries, and ensuring compliance with relevant laws and regulations. By adhering to Michigan's testamentary provisions for charitable remainder annuity trusts for a term of years, donors can ensure that their philanthropic intentions are honored, while also providing financial security for their chosen non-charitable beneficiaries. It is crucial to consult with legal and financial professionals to better understand the specific laws and regulations applicable to these types of trusts in Michigan.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Michigan Disposiciones testamentarias para fideicomiso de anualidad caritativa remanente por término de años - Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years

Description

How to fill out Michigan Disposiciones Testamentarias Para Fideicomiso De Anualidad Caritativa Remanente Por Término De Años?

Choosing the right authorized file web template might be a have a problem. Needless to say, there are a variety of themes available online, but how will you obtain the authorized type you will need? Make use of the US Legal Forms internet site. The support gives 1000s of themes, like the Michigan Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years, which can be used for business and private requires. Every one of the types are checked by specialists and fulfill state and federal needs.

In case you are currently authorized, log in in your profile and click the Obtain key to have the Michigan Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years. Utilize your profile to look throughout the authorized types you have acquired earlier. Proceed to the My Forms tab of your respective profile and acquire another copy of your file you will need.

In case you are a whole new user of US Legal Forms, here are basic recommendations that you should stick to:

- Very first, make sure you have selected the right type for the metropolis/region. You are able to look through the shape using the Review key and read the shape description to guarantee it is the right one for you.

- In the event the type fails to fulfill your expectations, make use of the Seach field to get the appropriate type.

- When you are sure that the shape is proper, click the Acquire now key to have the type.

- Opt for the prices program you want and enter the needed information and facts. Design your profile and pay for the order utilizing your PayPal profile or charge card.

- Select the data file format and download the authorized file web template in your product.

- Comprehensive, modify and print out and indicator the attained Michigan Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years.

US Legal Forms is definitely the greatest collection of authorized types where you can discover various file themes. Make use of the service to download appropriately-manufactured documents that stick to status needs.