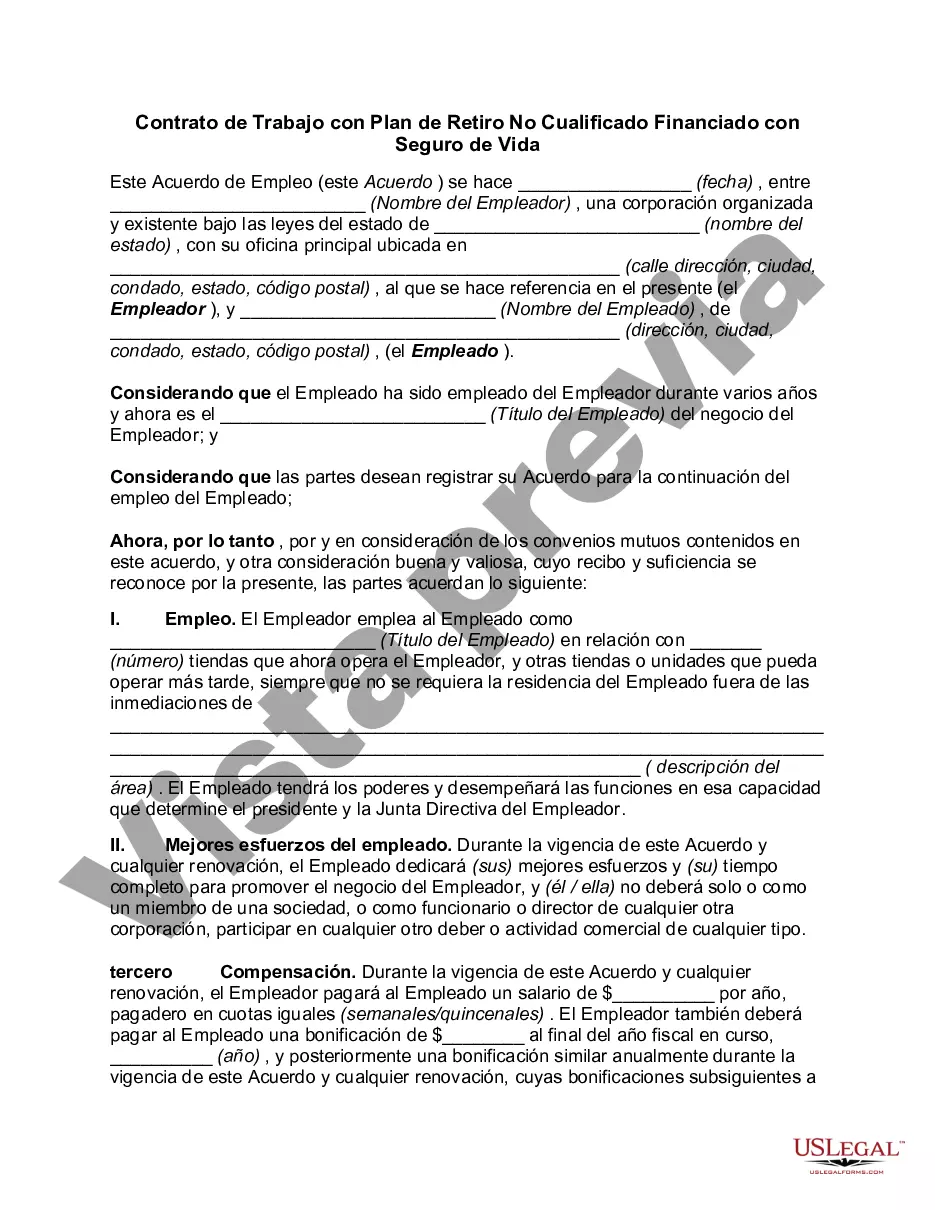

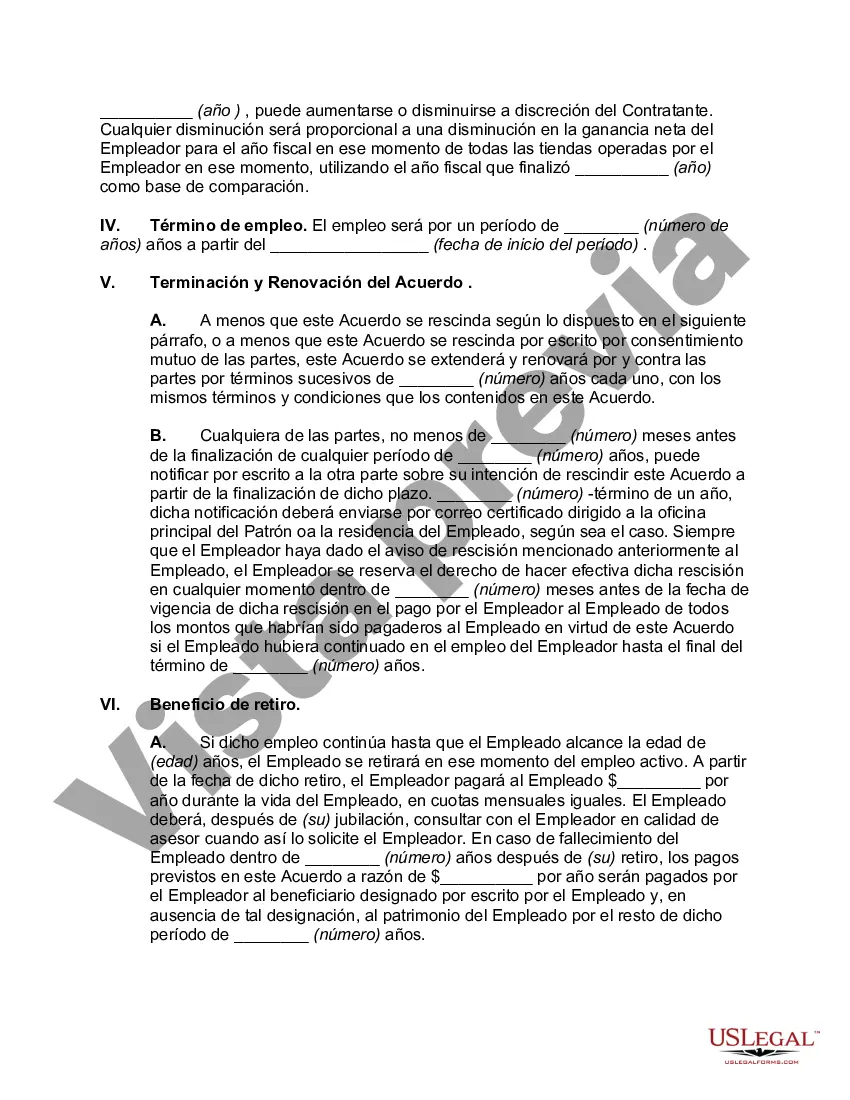

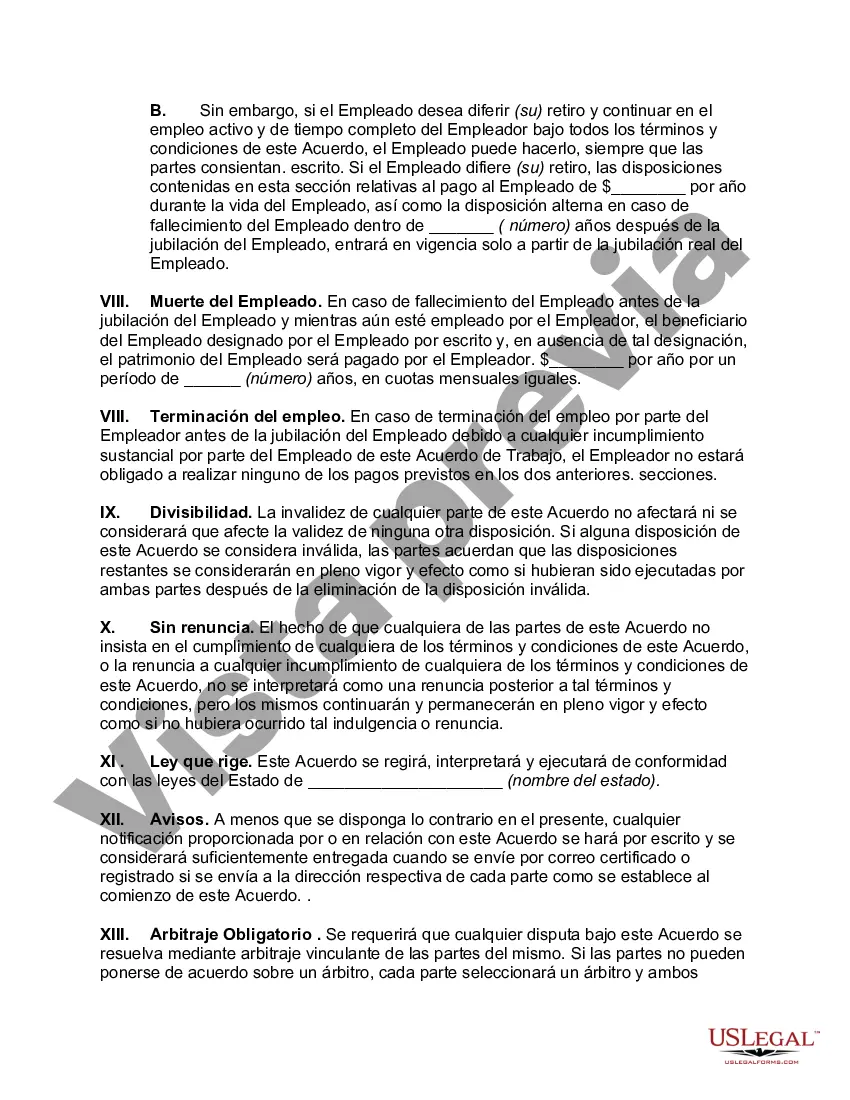

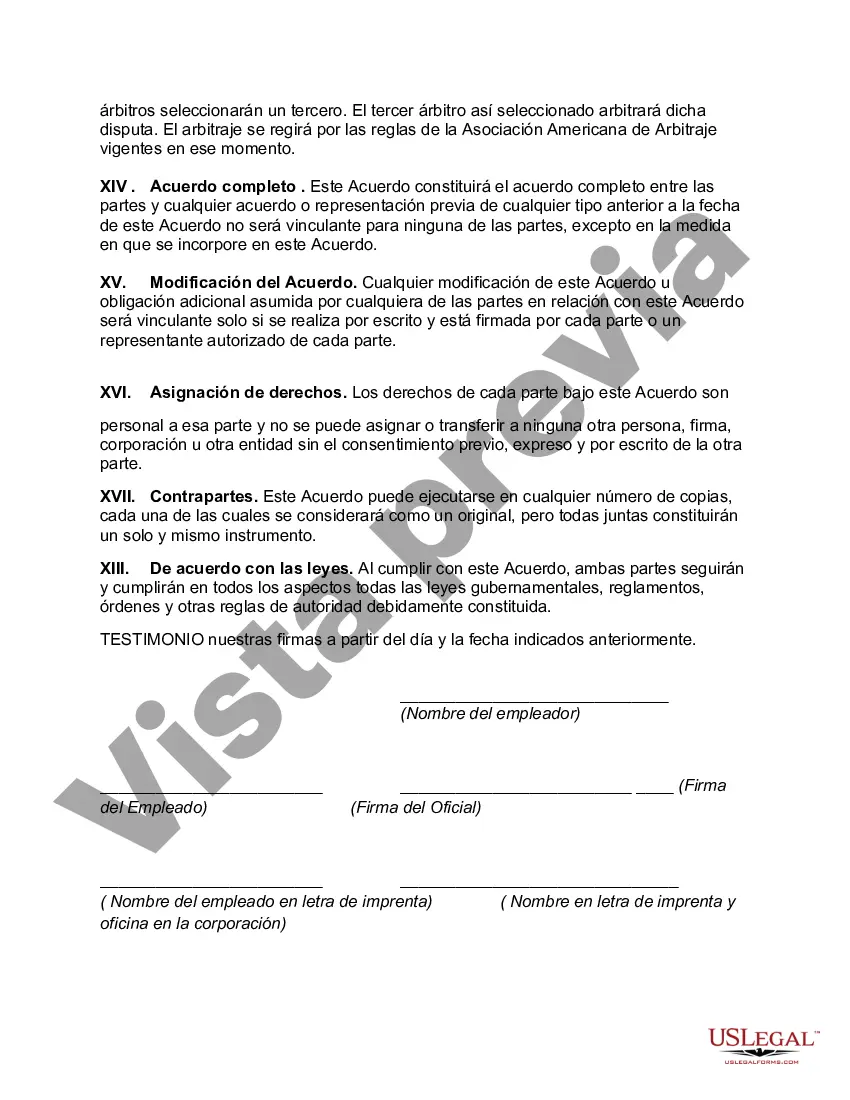

A Michigan Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance is a legally binding document that outlines the terms and conditions of an employment arrangement in the state of Michigan. This agreement specifically includes a nonqualified retirement plan that is funded through a life insurance policy. Keywords: Michigan, Employment Agreement, Nonqualified Retirement Plan, Life Insurance, Funded. In Michigan, there are several types of Employment Agreements with Nonqualified Retirement Plan Funded with Life Insurance: 1. Defined Contribution Nonqualified Retirement Plan: Under this agreement, the employer contributes a specific amount to the employee's retirement plan, which is funded with a life insurance policy. The contributions made by the employer are predetermined, and the employee will receive the accumulated amount upon retirement. 2. Deferred Compensation Nonqualified Retirement Plan: This type of agreement allows employees to defer a portion of their salary or bonus into a nonqualified retirement plan funded with life insurance. The funds grow tax-deferred until retirement, at which point the employee can start receiving payments or a lump sum. 3. Supplemental Executive Retirement Plan (SERP): SERPs are designed for executives and highly compensated employees. This agreement offers additional retirement benefits on top of other plans the employee may have. The funds are typically funded through life insurance policies, ensuring a tax-efficient way to provide retirement benefits. 4. Split-Dollar Nonqualified Retirement Plan: In this type of plan, the employer and employee share the cost and benefit of a life insurance policy. The employer pays the premiums, while the policy's cash value grows tax-deferred. Upon retirement, the split-dollar agreement determines how the benefits are allocated between the employer and the employee. The Michigan Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance typically includes the following key provisions: 1. Identification of the parties involved, including the employer and employee's names and addresses. 2. Employment terms, including start date, compensation structure, and duties and responsibilities. 3. Description of the nonqualified retirement plan, specifying the type of plan and funding method. 4. Contribution details, such as the employer's contribution percentage, frequency of contributions, and any employee deferrals. 5. Vesting schedule, outlining when the employee becomes entitled to the accumulated retirement benefits. 6. Retirement distribution options, including lump-sum payments, periodic payments, or a combination of both. 7. Tax implications, explaining the tax treatment of contributions, growth, and distributions. 8. Death benefits, clarifying how the life insurance component of the plan impacts beneficiaries in case of the employee's death. 9. Termination provisions, outlining the conditions under which the agreement can be terminated by either party. 10. Dispute resolution, specifying the process for resolving any disagreements or claims related to the agreement. It is essential to consult with legal and financial advisors when drafting or entering into a Michigan Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance to ensure compliance with state laws and to address specific circumstances and individual needs.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Michigan Contrato de Trabajo con Plan de Retiro No Cualificado Financiado con Seguro de Vida - Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance

Description

How to fill out Michigan Contrato De Trabajo Con Plan De Retiro No Cualificado Financiado Con Seguro De Vida?

Choosing the best legal papers web template can be quite a have difficulties. Needless to say, there are a variety of layouts available on the net, but how do you get the legal develop you require? Make use of the US Legal Forms web site. The assistance delivers 1000s of layouts, like the Michigan Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance, which you can use for company and personal demands. All of the varieties are inspected by pros and fulfill state and federal requirements.

Should you be currently registered, log in for your bank account and click on the Acquire switch to get the Michigan Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance. Use your bank account to check through the legal varieties you may have ordered previously. Visit the My Forms tab of the bank account and obtain yet another backup from the papers you require.

Should you be a brand new user of US Legal Forms, allow me to share easy instructions so that you can comply with:

- Very first, make sure you have chosen the proper develop for the metropolis/region. You may look over the form making use of the Review switch and look at the form information to ensure it will be the best for you.

- When the develop does not fulfill your expectations, make use of the Seach area to discover the proper develop.

- Once you are certain that the form is suitable, click the Purchase now switch to get the develop.

- Select the rates prepare you need and enter the essential details. Design your bank account and pay for an order making use of your PayPal bank account or Visa or Mastercard.

- Choose the data file format and down load the legal papers web template for your gadget.

- Total, revise and printing and indicator the obtained Michigan Employment Agreement with Nonqualified Retirement Plan Funded with Life Insurance.

US Legal Forms may be the most significant collection of legal varieties where you can see different papers layouts. Make use of the service to down load skillfully-created files that comply with condition requirements.