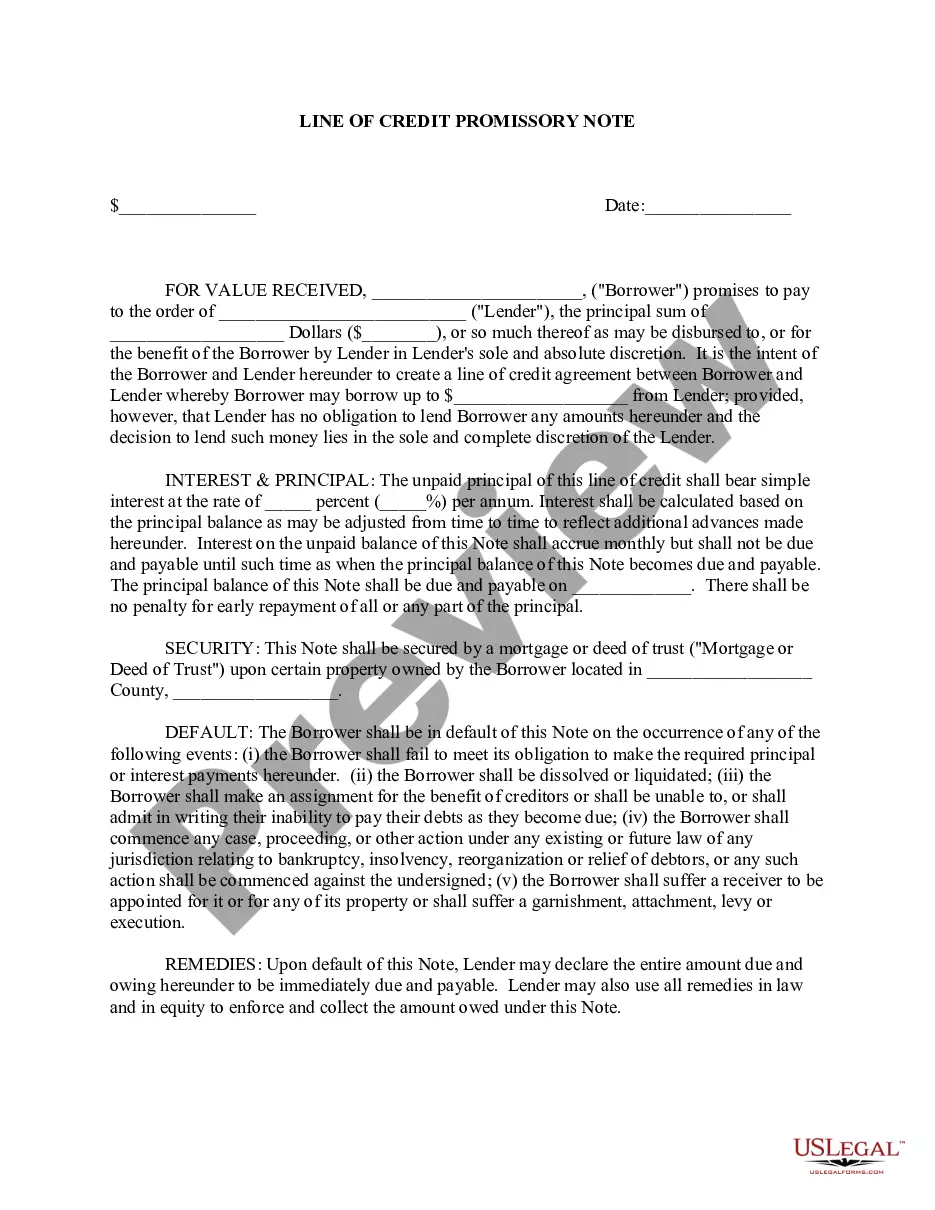

A Minnesota Line of Credit Promissory Note is a legal document that outlines the terms and conditions of a line of credit arrangement between a lender and a borrower in the state of Minnesota. This note serves as evidence of the borrower's promise to repay the borrowed amount along with the agreed-upon interest within a specified period. In Minnesota, there are different types of Line of Credit Promissory Notes, each serving a specific purpose. Here are a few commonly used ones: 1. Revolving Line of Credit Promissory Note: This type of promissory note allows the borrower to borrow and repay funds multiple times within a specific period, often referred to as the draw period. The borrower has the flexibility to use the funds as needed and can repay the borrowed amount to restore the line of credit for future use. 2. Home Equity Line of Credit Promissory Note: Specifically designed for homeowners, this note allows them to borrow money against the equity in their homes. The borrowed money can be used for various purposes such as home improvements, debt consolidation, or other personal expenses. The borrower may draw money from and repay it multiple times within the predefined terms. 3. Commercial Line of Credit Promissory Note: Primarily used by businesses, this note provides access to funds needed for day-to-day operations or for specific business activities. It offers businesses the flexibility to borrow and repay money as required, ensuring a steady cash flow to meet operational needs. 4. Personal Line of Credit Promissory Note: This type of promissory note is applicable to individuals who need ongoing access to a predetermined amount of funds. They can use the borrowed money for personal expenses, emergencies, or other financial needs. Similar to a credit card, the borrower can draw money up to the credit limit and repay it as per the agreement. Regardless of the type, a Minnesota Line of Credit Promissory Note typically includes essential information such as the names and addresses of the lender and borrower, the principal amount to be borrowed, the interest rate, repayment terms, collateral (if any), late payment penalties, default conditions, and governing law. It is crucial for both the lender and the borrower to carefully review and understand the terms and conditions outlined in the Minnesota Line of Credit Promissory Note before signing it. Seeking legal advice or consulting with professionals can help ensure that the document accurately reflects the intentions of both parties and provides clear guidance in case of any disputes or default situations.

Minnesota Line of Credit Promissory Note

Description

How to fill out Minnesota Line Of Credit Promissory Note?

It is possible to commit hrs online trying to find the legal papers web template that fits the federal and state specifications you need. US Legal Forms provides 1000s of legal varieties which are examined by experts. You can actually acquire or printing the Minnesota Line of Credit Promissory Note from your assistance.

If you have a US Legal Forms accounts, you are able to log in and click the Down load switch. Next, you are able to comprehensive, revise, printing, or indication the Minnesota Line of Credit Promissory Note. Every legal papers web template you get is yours forever. To acquire yet another copy associated with a obtained develop, check out the My Forms tab and click the corresponding switch.

Should you use the US Legal Forms internet site for the first time, stick to the straightforward recommendations beneath:

- First, make sure that you have chosen the correct papers web template for the county/city of your choice. Look at the develop description to ensure you have chosen the appropriate develop. If readily available, take advantage of the Preview switch to look through the papers web template too.

- If you would like locate yet another variation from the develop, take advantage of the Research field to find the web template that suits you and specifications.

- Once you have identified the web template you desire, click Get now to continue.

- Choose the pricing prepare you desire, type your qualifications, and sign up for your account on US Legal Forms.

- Comprehensive the deal. You may use your bank card or PayPal accounts to fund the legal develop.

- Choose the file format from the papers and acquire it to your system.

- Make alterations to your papers if required. It is possible to comprehensive, revise and indication and printing Minnesota Line of Credit Promissory Note.

Down load and printing 1000s of papers layouts while using US Legal Forms web site, which provides the biggest variety of legal varieties. Use skilled and status-certain layouts to handle your company or specific requirements.