A loan workout is a series of steps taken by a lender with a borrower to resolve the problem of delinquent loan payments. Steps can include rescheduling loan payments into lower installments over a longer period of time so that the entire outstanding principal is eventually repaid. One of the items lenders often ask for during the loan workout or loan modification process is a hardship letter. A hardship letter is a written explanation as to what has caused you to fall behind on your mortgage. Some of the hardships that that lenders consider during the loan workout process are the following: Illness; Loss of Job; Reduced Income; Failed Business; Job Relocation; Death of Spouse or Co-Borrower; Incarceration; Divorce; Military Duty; and Damage to Property (e.g., natural disaster or fire).

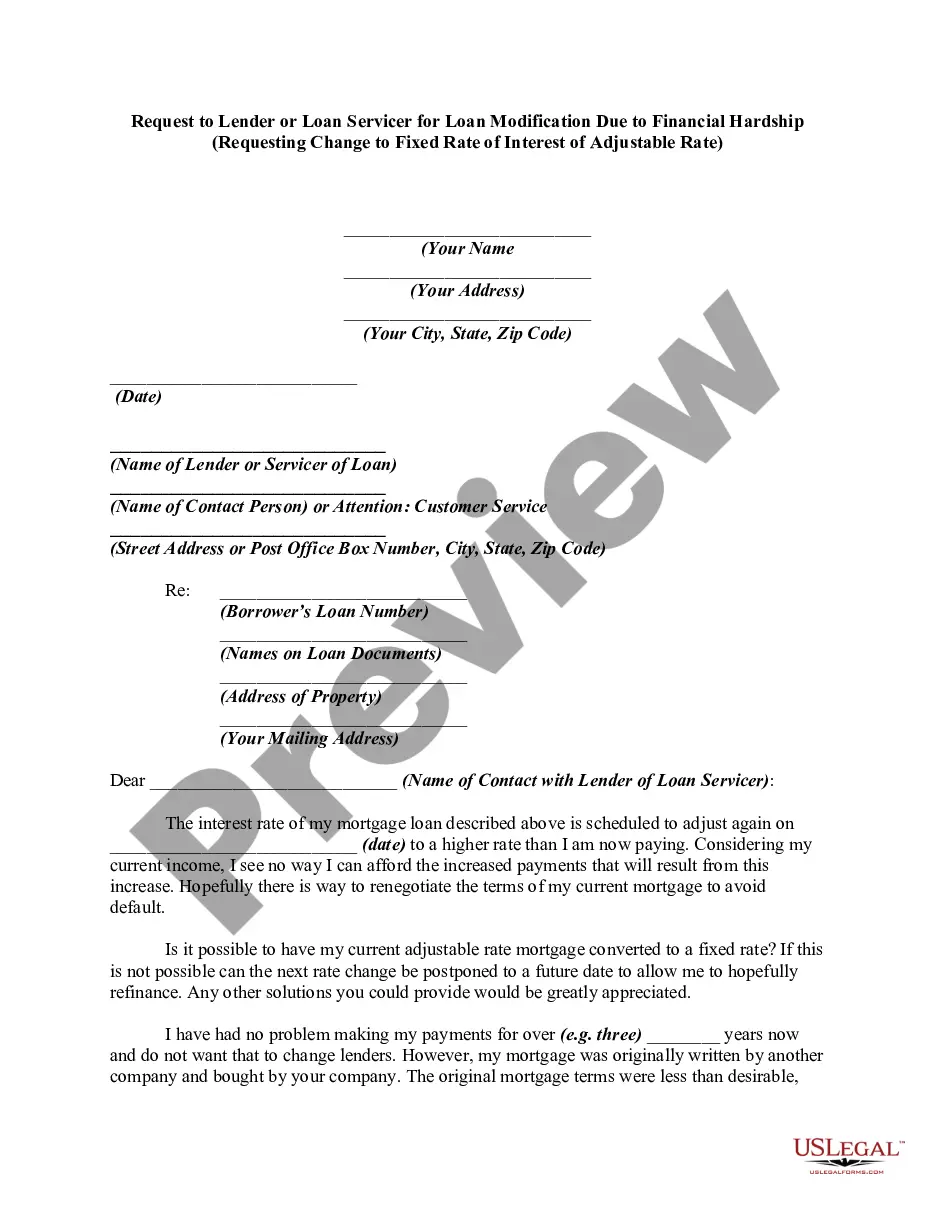

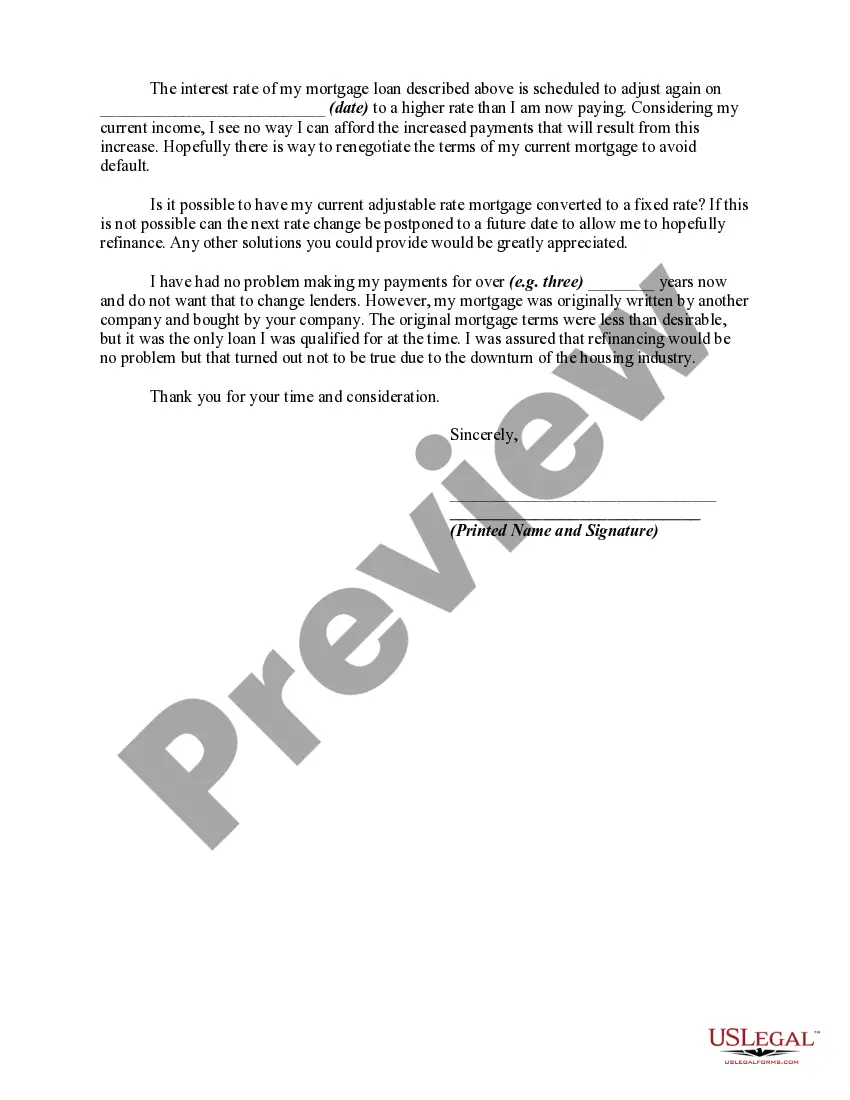

Title: Understanding Minnesota Request for Loan Modification Due to Financial Hardship — Switching from Adjustable Rate to Fixed Rate Introduction: When faced with financial difficulties, homeowners in Minnesota may need to explore different options to make their mortgage more manageable. One possible solution is requesting a loan modification from their lender or loan service. This article aims to provide a detailed description of a Minnesota Request for Loan Modification due to financial hardship, specifically focused on requesting a change from an adjustable rate to a fixed rate of interest. Read on to understand the process, key considerations, and potential outcomes associated with this request. 1. Understanding the Minnesota Loan Modification Process: 1.1 Eligibility Criteria: — Financial hardshiexplanationio— - Reliable income and affordability assessment — Current loan performance evaluation 1.2 Gathering Documentation: — Proof of income such as pay stubs, tax returns, or bank statements — Recent mortgage statements and property appraisal — Supporting documents illustrating financial hardship (e.g., medical bills, termination letters) 1.3 Preparing the Loan Modification Request: — Crafting a detailed hardship letter explaining the financial situation — Detailing the preferred fixed rate of interest — Providing a complete financial statement and budget analysis 1.4 Submitting the Request: — Sending the loan modification package to the lender or loan service (specifically mentioning the request for a change to a fixed interest rate) — Keeping copies of all documents and proof of delivery 1.5 Review and Approval Process: — Lender's evaluation of the financial information and hardship claim — Decision-makintimelinein— - Potential negotiation or counter-offer 2. Key Considerations for Requesting a Change from Adjustable to Fixed Rate: 2.1 Interest Rate Stability and Predictability: — Explaining the benefits of a fixed interest rate and its impact on budgeting — Highlighting concerns regarding the variability of adjustable rates 2.2 Financial Risk Mitigation: — Discussing potential financial challenges due to rate increases — Emphasizing the desire for a stable and sustainable mortgage payment 2.3 Comparing Interest Rates: — Analyzing historical trends in interest rates — Providing data on the current interest rates and market volatility 2.4 Potential Long-Term Savings: — Stating the potential long-term savings by obtaining a fixed rate — Demonstrating the financial advantage of a longer-term mortgage plan 3. Possible Outcomes and Alternatives: 3.1 Approval of Loan Modification Request: — Lender's agreement to switch from adjustable to fixed rate — Confirmation of modified terms and monthly payment adjustment 3.2 Counteroffers or Negotiations: — Potential counteroffers by the lender, such as alternatives to the requested fixed rate — Considering the lender's proposed modifications and their impact 3.3 Consideration of Other Loan Modification Programs: — Mentioning other available programs specific to Minnesota, such as the Home Affordable Modification Program (CAMP) — Exploring additional options, such as principal forbearance or loan term extension In conclusion, submitting a Minnesota Request for Loan Modification is a critical step for homeowners facing financial hardship. When seeking to transition from an adjustable rate to a fixed rate, careful presentation of the request and its associated benefits is crucial. Understanding the process, considerations, and potential outcomes will greatly assist in navigating this loan modification journey effectively. Keywords: Minnesota, loan modification, financial hardship, adjustable rate, fixed rate, request, lender, loan service, interest rate, eligibility criteria, documentation, hardship letter, financial statement, budget analysis, submission, review process, approval, negotiation, savings, alternatives, Home Affordable Modification Program, principal forbearance.Title: Understanding Minnesota Request for Loan Modification Due to Financial Hardship — Switching from Adjustable Rate to Fixed Rate Introduction: When faced with financial difficulties, homeowners in Minnesota may need to explore different options to make their mortgage more manageable. One possible solution is requesting a loan modification from their lender or loan service. This article aims to provide a detailed description of a Minnesota Request for Loan Modification due to financial hardship, specifically focused on requesting a change from an adjustable rate to a fixed rate of interest. Read on to understand the process, key considerations, and potential outcomes associated with this request. 1. Understanding the Minnesota Loan Modification Process: 1.1 Eligibility Criteria: — Financial hardshiexplanationio— - Reliable income and affordability assessment — Current loan performance evaluation 1.2 Gathering Documentation: — Proof of income such as pay stubs, tax returns, or bank statements — Recent mortgage statements and property appraisal — Supporting documents illustrating financial hardship (e.g., medical bills, termination letters) 1.3 Preparing the Loan Modification Request: — Crafting a detailed hardship letter explaining the financial situation — Detailing the preferred fixed rate of interest — Providing a complete financial statement and budget analysis 1.4 Submitting the Request: — Sending the loan modification package to the lender or loan service (specifically mentioning the request for a change to a fixed interest rate) — Keeping copies of all documents and proof of delivery 1.5 Review and Approval Process: — Lender's evaluation of the financial information and hardship claim — Decision-makintimelinein— - Potential negotiation or counter-offer 2. Key Considerations for Requesting a Change from Adjustable to Fixed Rate: 2.1 Interest Rate Stability and Predictability: — Explaining the benefits of a fixed interest rate and its impact on budgeting — Highlighting concerns regarding the variability of adjustable rates 2.2 Financial Risk Mitigation: — Discussing potential financial challenges due to rate increases — Emphasizing the desire for a stable and sustainable mortgage payment 2.3 Comparing Interest Rates: — Analyzing historical trends in interest rates — Providing data on the current interest rates and market volatility 2.4 Potential Long-Term Savings: — Stating the potential long-term savings by obtaining a fixed rate — Demonstrating the financial advantage of a longer-term mortgage plan 3. Possible Outcomes and Alternatives: 3.1 Approval of Loan Modification Request: — Lender's agreement to switch from adjustable to fixed rate — Confirmation of modified terms and monthly payment adjustment 3.2 Counteroffers or Negotiations: — Potential counteroffers by the lender, such as alternatives to the requested fixed rate — Considering the lender's proposed modifications and their impact 3.3 Consideration of Other Loan Modification Programs: — Mentioning other available programs specific to Minnesota, such as the Home Affordable Modification Program (CAMP) — Exploring additional options, such as principal forbearance or loan term extension In conclusion, submitting a Minnesota Request for Loan Modification is a critical step for homeowners facing financial hardship. When seeking to transition from an adjustable rate to a fixed rate, careful presentation of the request and its associated benefits is crucial. Understanding the process, considerations, and potential outcomes will greatly assist in navigating this loan modification journey effectively. Keywords: Minnesota, loan modification, financial hardship, adjustable rate, fixed rate, request, lender, loan service, interest rate, eligibility criteria, documentation, hardship letter, financial statement, budget analysis, submission, review process, approval, negotiation, savings, alternatives, Home Affordable Modification Program, principal forbearance.