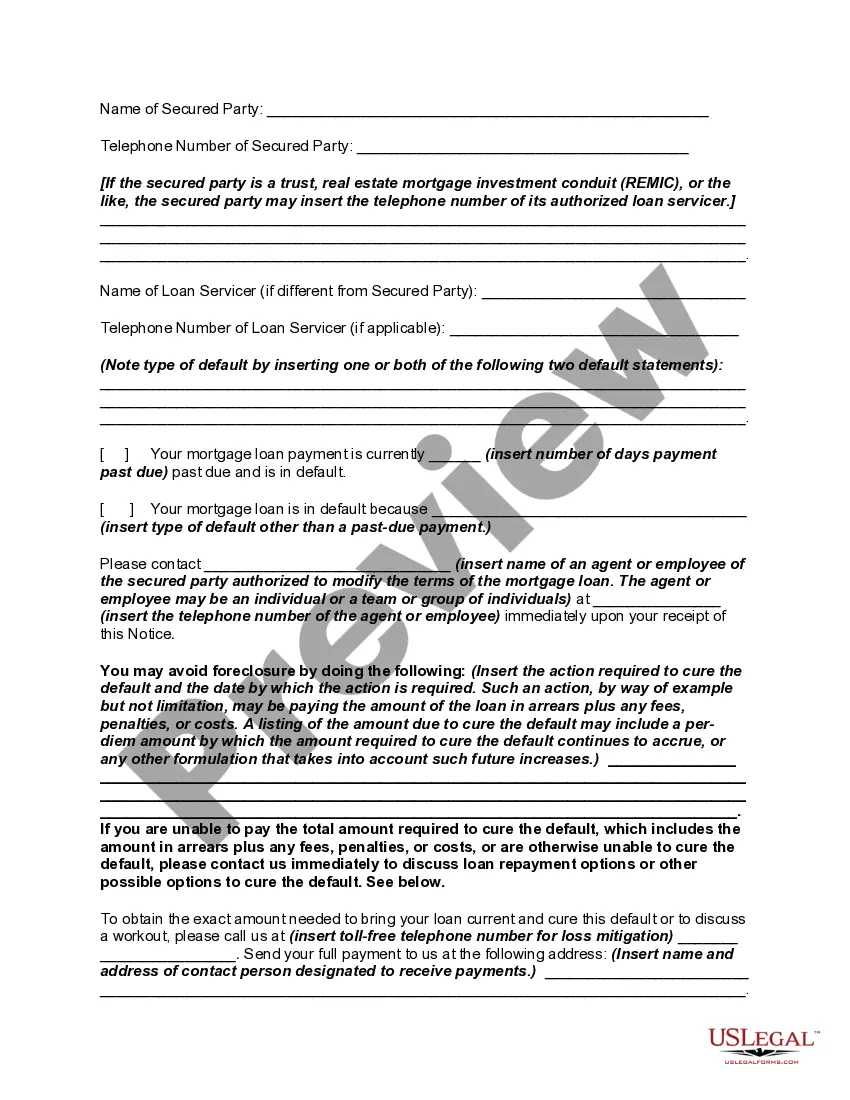

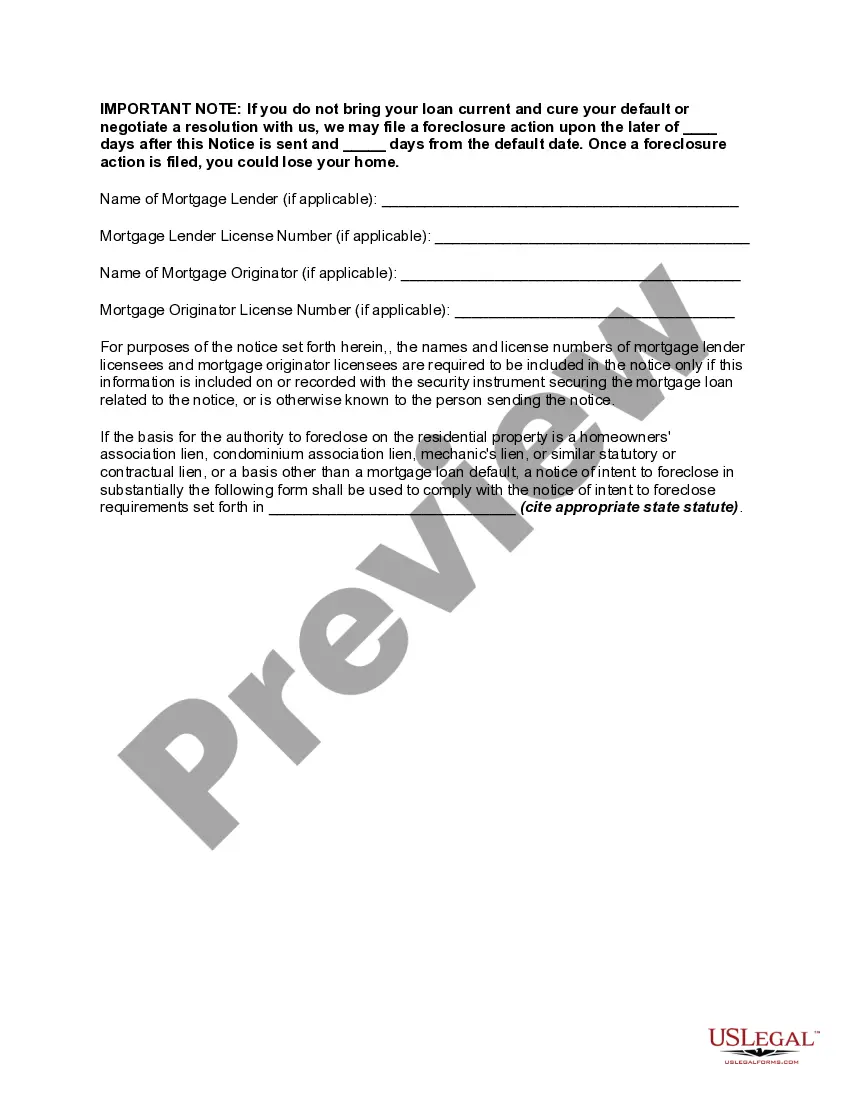

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

A Minnesota Notice of Intent to Foreclose — Mortgage Loan Default is an essential legal document that signifies the initiation of the foreclosure process due to the default on a mortgage loan in the state of Minnesota. This notice serves as a formal communication from the mortgage lender or their assigned representative to the borrower, informing them of their failure to comply with the terms and conditions of their mortgage agreement. Keywords: Minnesota, Notice of Intent to Foreclose, Mortgage Loan Default, foreclosure process, mortgage lender, borrower, terms and conditions, mortgage agreement. In Minnesota, the Notice of Intent to Foreclose — Mortgage Loan Default may vary depending on the specific circumstances of the default. Here are some common types of notices related to mortgage loan default in Minnesota: 1. Pre-Foreclosure Notice: This notice is typically issued by the mortgage lender after the borrower misses several consecutive mortgage payments. It informs the borrower of their default status and serves as a warning that foreclosure proceedings may begin if the delinquency is not resolved within a specified timeframe. 2. Notice of Sheriff's Sale: If the borrower fails to rectify the default after receiving the pre-foreclosure notice, the mortgage lender may proceed with filing a Notice of Sheriff's Sale. This notice indicates that the property will be sold at a public auction to recover the outstanding mortgage debt. 3. Notice of Li's Pendent: This notice is filed by the mortgage lender to provide public notice of pending legal action against the borrower. It serves as a warning to potential buyers or interested parties that the property is facing foreclosure and should be approached with caution. 4. Notice of Redemption Period: In Minnesota, after the foreclosure sale, the borrower has a right to redeem the property by repaying the outstanding debt within a specific redemption period. The Notice of Redemption Period informs the borrower of this option, including the length of the redemption period and the redemption amount required to regain ownership of the property. 5. Notice of Eviction: If the borrower fails to redeem the property within the designated redemption period, the mortgage lender may proceed with the eviction process. The Notice of Eviction is a final notice served to the borrower, informing them of the eviction date and the necessity to vacate the premises. Understanding the various types of Minnesota Notice of Intent to Foreclose — Mortgage Loan Default is crucial for both borrowers and lenders involved in the foreclosure process. It is important for borrowers to carefully review and respond to these notices promptly, as each notice signifies a critical stage in the foreclosure timeline. Likewise, lenders must ensure compliance with Minnesota foreclosure laws when issuing these notices to protect their rights and interests.A Minnesota Notice of Intent to Foreclose — Mortgage Loan Default is an essential legal document that signifies the initiation of the foreclosure process due to the default on a mortgage loan in the state of Minnesota. This notice serves as a formal communication from the mortgage lender or their assigned representative to the borrower, informing them of their failure to comply with the terms and conditions of their mortgage agreement. Keywords: Minnesota, Notice of Intent to Foreclose, Mortgage Loan Default, foreclosure process, mortgage lender, borrower, terms and conditions, mortgage agreement. In Minnesota, the Notice of Intent to Foreclose — Mortgage Loan Default may vary depending on the specific circumstances of the default. Here are some common types of notices related to mortgage loan default in Minnesota: 1. Pre-Foreclosure Notice: This notice is typically issued by the mortgage lender after the borrower misses several consecutive mortgage payments. It informs the borrower of their default status and serves as a warning that foreclosure proceedings may begin if the delinquency is not resolved within a specified timeframe. 2. Notice of Sheriff's Sale: If the borrower fails to rectify the default after receiving the pre-foreclosure notice, the mortgage lender may proceed with filing a Notice of Sheriff's Sale. This notice indicates that the property will be sold at a public auction to recover the outstanding mortgage debt. 3. Notice of Li's Pendent: This notice is filed by the mortgage lender to provide public notice of pending legal action against the borrower. It serves as a warning to potential buyers or interested parties that the property is facing foreclosure and should be approached with caution. 4. Notice of Redemption Period: In Minnesota, after the foreclosure sale, the borrower has a right to redeem the property by repaying the outstanding debt within a specific redemption period. The Notice of Redemption Period informs the borrower of this option, including the length of the redemption period and the redemption amount required to regain ownership of the property. 5. Notice of Eviction: If the borrower fails to redeem the property within the designated redemption period, the mortgage lender may proceed with the eviction process. The Notice of Eviction is a final notice served to the borrower, informing them of the eviction date and the necessity to vacate the premises. Understanding the various types of Minnesota Notice of Intent to Foreclose — Mortgage Loan Default is crucial for both borrowers and lenders involved in the foreclosure process. It is important for borrowers to carefully review and respond to these notices promptly, as each notice signifies a critical stage in the foreclosure timeline. Likewise, lenders must ensure compliance with Minnesota foreclosure laws when issuing these notices to protect their rights and interests.