Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

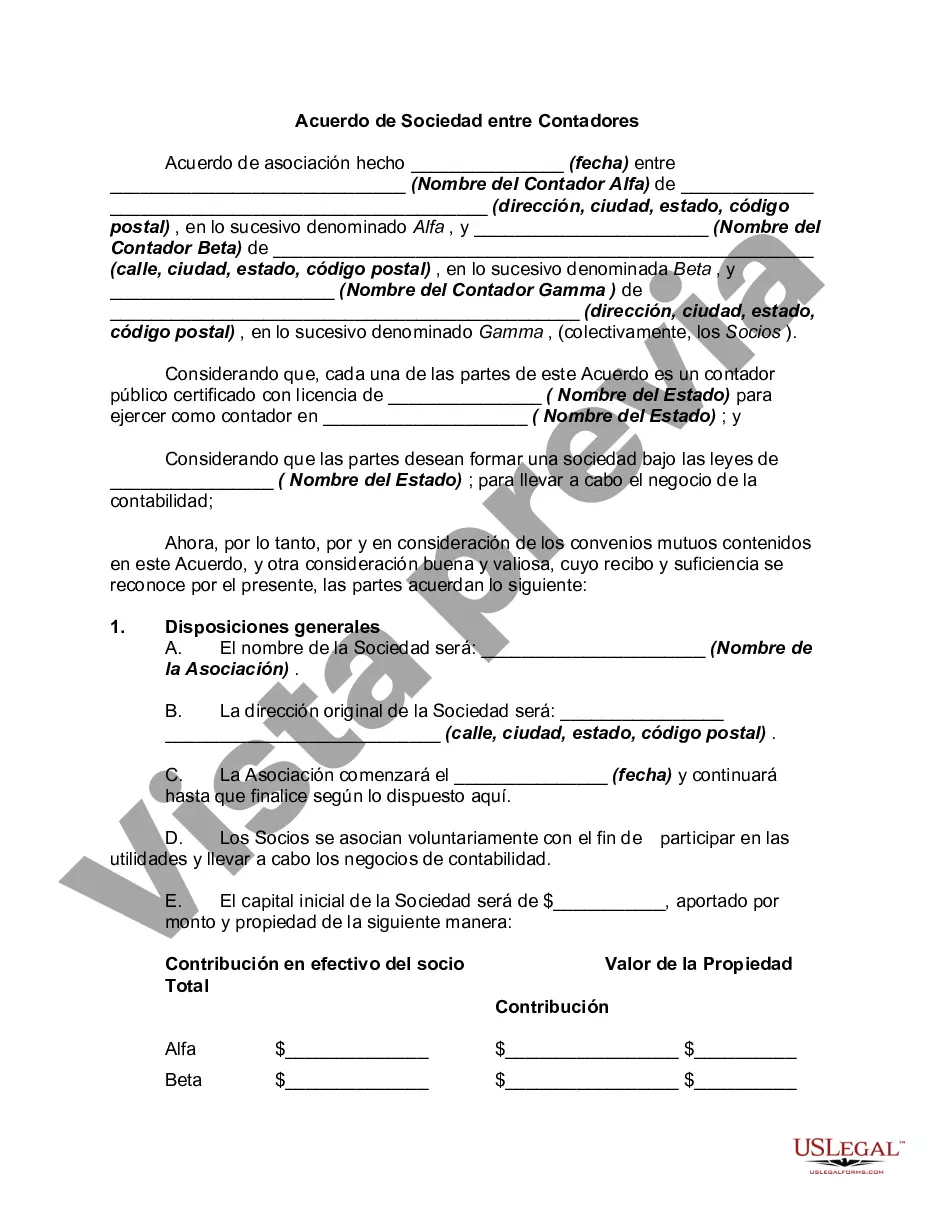

A Minnesota Partnership Agreement between Accountants is a legally binding contract that outlines the terms and conditions for a partnership between two or more accountants who wish to collaborate on business operations and share profits and losses. This agreement sets forth the rights, responsibilities, and obligations of each partner, ensuring a fair and transparent working relationship. The key elements and important clauses included in a Minnesota Partnership Agreement between Accountants typically cover: 1. Name and Purpose: The name of the partnership is stated along with a clear description of its purpose, which can be offering accounting services, tax preparation, financial planning, or any other related service. 2. Capital Contributions: This section outlines the initial capital investments made by each partner, specifying the amount and mode of contribution (cash, equipment, or other assets). 3. Profit and Loss Sharing: It describes the method of distributing profits and allocating losses among partners, which can be equally, based on the ratio of their capital contributions or with another agreed-upon formula. 4. Decision-making and Management: Roles and responsibilities of each partner in decision-making, management, and day-to-day operations are defined. It may establish voting rights, decision thresholds, and the appointment of a managing partner or committee. 5. Partner Withdrawal or Death: Procedures for a partner's voluntary withdrawal, retirement, or death are outlined, including the distribution of their capital, accrued profits, and liabilities. 6. Dissolution: This clause details the process of terminating the partnership, specifying the steps to be followed, such as notifying clients and settling debts. It may also address circumstances like bankruptcy or breach of partnership agreement. 7. Non-compete and Non-solicitation: Restrictions on partners from engaging in competing activities or soliciting clients after leaving the partnership can be established to protect the partnership's interests. 8. Dispute Resolution: This section outlines the mechanism for resolving conflicts or disputes arising among partners, including mediation, arbitration, or litigation, specifying the jurisdiction and venue of filing lawsuits if needed. Types of Minnesota Partnership Agreements between Accountants may include: 1. General Partnership Agreement: A partnership where all partners share equal responsibility for management and personal liability for the partnership's debts. 2. Limited Liability Partnership (LLP) Agreement: This type of partnership provides partners with limited personal liability protection, safeguarding them from each other's malpractice claims, and allowing business continuity in case of a partner's misdeeds. 3. Limited Partnership Agreement (LP): A partnership that consists of at least one general partner responsible for management and personal liability and one or more limited partners who contribute capital but have no involvement in the partnership's management decisions. In conclusion, a Minnesota Partnership Agreement between Accountants is a crucial legal document that helps establish and govern a partnership, promoting clarity, trust, and cooperation between accountants. It defines the partners' rights, obligations, profit-sharing methods, decision-making processes, and procedures for dispute resolution or dissolution. It is important for accountants to carefully consider and draft a comprehensive agreement tailored to their specific partnership type and objectives.A Minnesota Partnership Agreement between Accountants is a legally binding contract that outlines the terms and conditions for a partnership between two or more accountants who wish to collaborate on business operations and share profits and losses. This agreement sets forth the rights, responsibilities, and obligations of each partner, ensuring a fair and transparent working relationship. The key elements and important clauses included in a Minnesota Partnership Agreement between Accountants typically cover: 1. Name and Purpose: The name of the partnership is stated along with a clear description of its purpose, which can be offering accounting services, tax preparation, financial planning, or any other related service. 2. Capital Contributions: This section outlines the initial capital investments made by each partner, specifying the amount and mode of contribution (cash, equipment, or other assets). 3. Profit and Loss Sharing: It describes the method of distributing profits and allocating losses among partners, which can be equally, based on the ratio of their capital contributions or with another agreed-upon formula. 4. Decision-making and Management: Roles and responsibilities of each partner in decision-making, management, and day-to-day operations are defined. It may establish voting rights, decision thresholds, and the appointment of a managing partner or committee. 5. Partner Withdrawal or Death: Procedures for a partner's voluntary withdrawal, retirement, or death are outlined, including the distribution of their capital, accrued profits, and liabilities. 6. Dissolution: This clause details the process of terminating the partnership, specifying the steps to be followed, such as notifying clients and settling debts. It may also address circumstances like bankruptcy or breach of partnership agreement. 7. Non-compete and Non-solicitation: Restrictions on partners from engaging in competing activities or soliciting clients after leaving the partnership can be established to protect the partnership's interests. 8. Dispute Resolution: This section outlines the mechanism for resolving conflicts or disputes arising among partners, including mediation, arbitration, or litigation, specifying the jurisdiction and venue of filing lawsuits if needed. Types of Minnesota Partnership Agreements between Accountants may include: 1. General Partnership Agreement: A partnership where all partners share equal responsibility for management and personal liability for the partnership's debts. 2. Limited Liability Partnership (LLP) Agreement: This type of partnership provides partners with limited personal liability protection, safeguarding them from each other's malpractice claims, and allowing business continuity in case of a partner's misdeeds. 3. Limited Partnership Agreement (LP): A partnership that consists of at least one general partner responsible for management and personal liability and one or more limited partners who contribute capital but have no involvement in the partnership's management decisions. In conclusion, a Minnesota Partnership Agreement between Accountants is a crucial legal document that helps establish and govern a partnership, promoting clarity, trust, and cooperation between accountants. It defines the partners' rights, obligations, profit-sharing methods, decision-making processes, and procedures for dispute resolution or dissolution. It is important for accountants to carefully consider and draft a comprehensive agreement tailored to their specific partnership type and objectives.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.