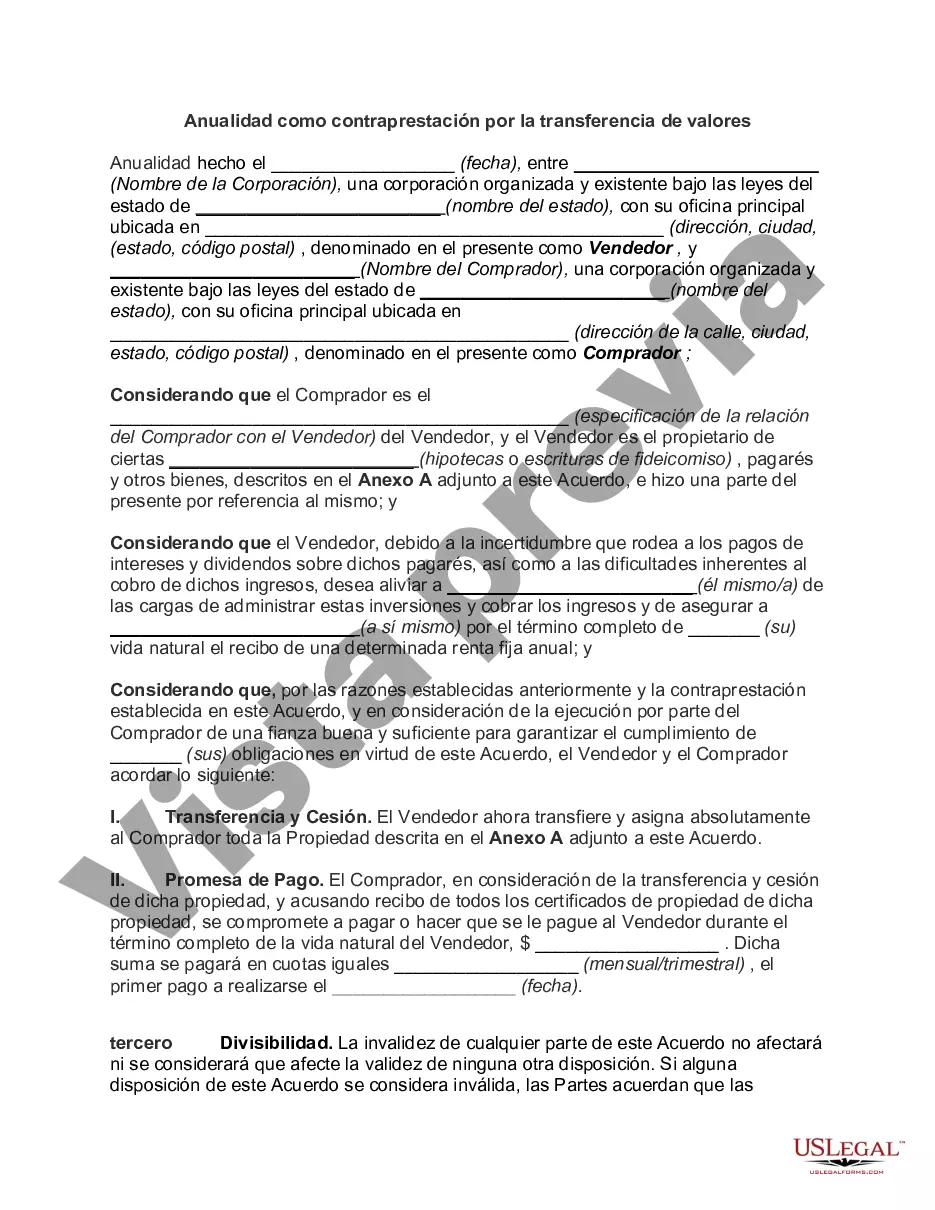

Minnesota Annuity as Consideration for Transfer of Securities refers to a specific type of financial arrangement in the state of Minnesota where an annuity is utilized as consideration, or payment, for the transfer of securities. This arrangement typically involves the transfer of securities, such as stocks or bonds, from one party to another in exchange for an annuity contract. An annuity is a financial product offered by insurance companies, which provides a stream of income payments to the annuity holder, or annuitant, over a specified period of time or for the annuitant's lifetime. In the context of the Minnesota Annuity as Consideration for Transfer of Securities, the annuity contract forms the basis for the payment made by the transferee of securities to the transferor. There are several types of Minnesota Annuities as Consideration for Transfer of Securities, distinguished by their specific features and terms. These types include: 1. Fixed annuity: This type of annuity guarantees a fixed rate of return or interest over the life of the contract. The annuitant will receive a consistent income stream throughout the annuity's term, providing stability and predictability. 2. Variable annuity: Unlike a fixed annuity, a variable annuity offers investment options where the annuitant can allocate the funds across a range of investment options, such as stocks, bonds, or mutual funds. The annuity's performance is directly linked to the investment performance of the chosen options. 3. Equity-indexed annuity: This type of annuity provides a return based on the performance of a particular stock market index, such as the S&P 500. The annuity's value will fluctuate based on the index's performance, offering the potential for higher returns while also providing downside protection. 4. Immediate annuity: An immediate annuity begins making income payments shortly after the annuity is purchased. This can be an attractive option for those seeking immediate income in retirement or to convert securities into a steady income stream. By utilizing a Minnesota Annuity as Consideration for Transfer of Securities, parties can efficiently transfer securities while also organizing a secure income stream. It provides benefits for both parties involved, with the transferor gaining a guaranteed income source and the transferee acquiring securities to diversify their investment portfolio. In conclusion, Minnesota Annuity as Consideration for Transfer of Securities involves the exchange of securities for an annuity contract. With various types of annuities available, individuals can select the most suitable option based on their financial goals and risk tolerance. This arrangement facilitates the transfer of securities while ensuring a steady income flow, and it can be a valuable tool in the realm of financial planning and asset management.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Minnesota Anualidad como contraprestación por la transferencia de valores - Annuity as Consideration for Transfer of Securities

Description

How to fill out Minnesota Anualidad Como Contraprestación Por La Transferencia De Valores?

US Legal Forms - among the most significant libraries of legal forms in America - offers a wide range of legal record web templates it is possible to obtain or produce. While using web site, you can get 1000s of forms for business and personal uses, sorted by types, claims, or keywords and phrases.You can get the latest models of forms such as the Minnesota Annuity as Consideration for Transfer of Securities within minutes.

If you already have a membership, log in and obtain Minnesota Annuity as Consideration for Transfer of Securities through the US Legal Forms catalogue. The Down load key can look on each type you look at. You have accessibility to all previously acquired forms in the My Forms tab of the bank account.

In order to use US Legal Forms initially, listed below are simple instructions to help you started off:

- Ensure you have picked the correct type for the metropolis/region. Click the Review key to review the form`s articles. Browse the type explanation to actually have chosen the proper type.

- In the event the type does not fit your demands, utilize the Research area at the top of the screen to discover the one that does.

- If you are content with the shape, confirm your selection by clicking the Get now key. Then, opt for the pricing program you want and give your qualifications to sign up for the bank account.

- Approach the purchase. Make use of charge card or PayPal bank account to perform the purchase.

- Find the format and obtain the shape in your gadget.

- Make modifications. Complete, change and produce and indication the acquired Minnesota Annuity as Consideration for Transfer of Securities.

Every single format you included with your money lacks an expiration day and is the one you have for a long time. So, if you wish to obtain or produce another version, just check out the My Forms segment and then click around the type you require.

Obtain access to the Minnesota Annuity as Consideration for Transfer of Securities with US Legal Forms, by far the most considerable catalogue of legal record web templates. Use 1000s of expert and status-distinct web templates that fulfill your business or personal requires and demands.