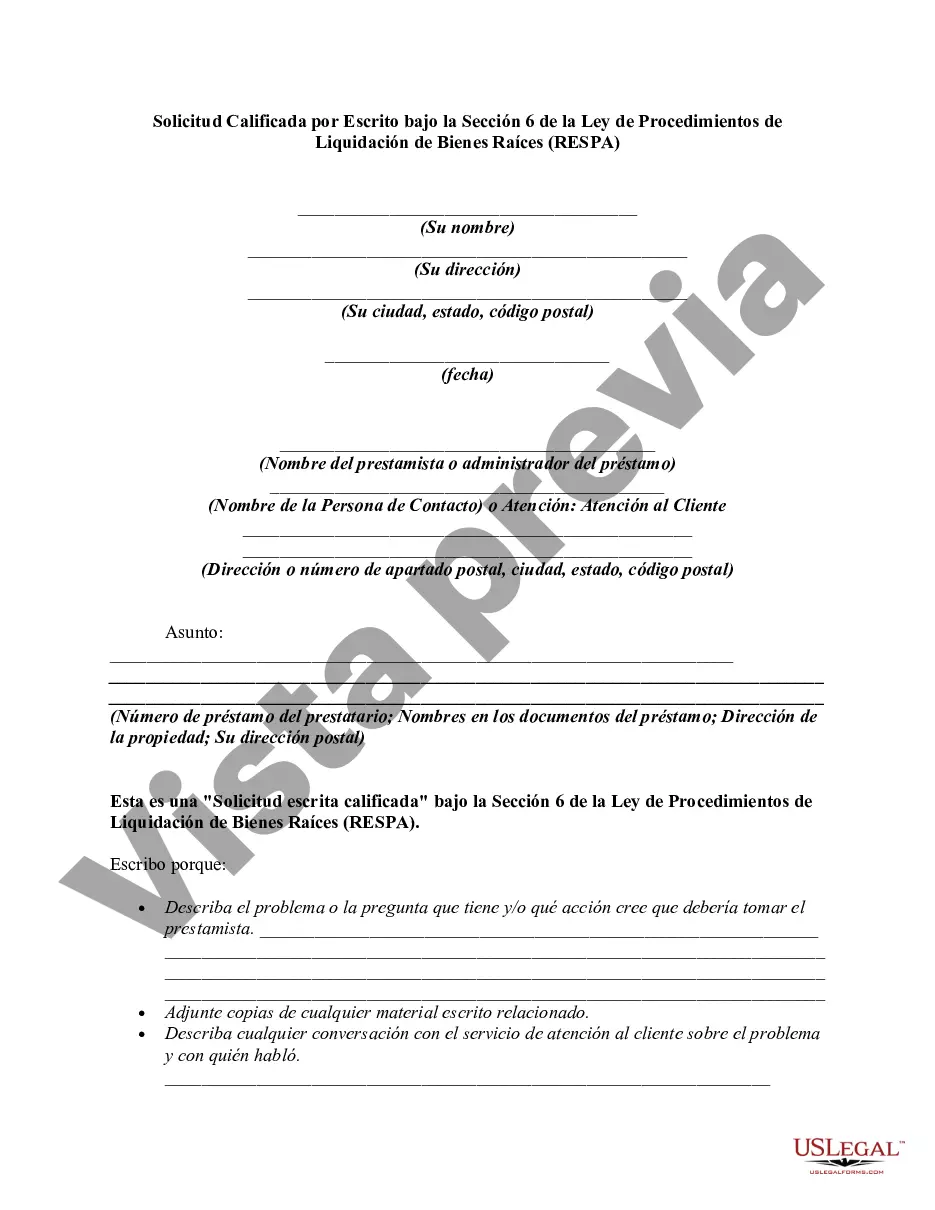

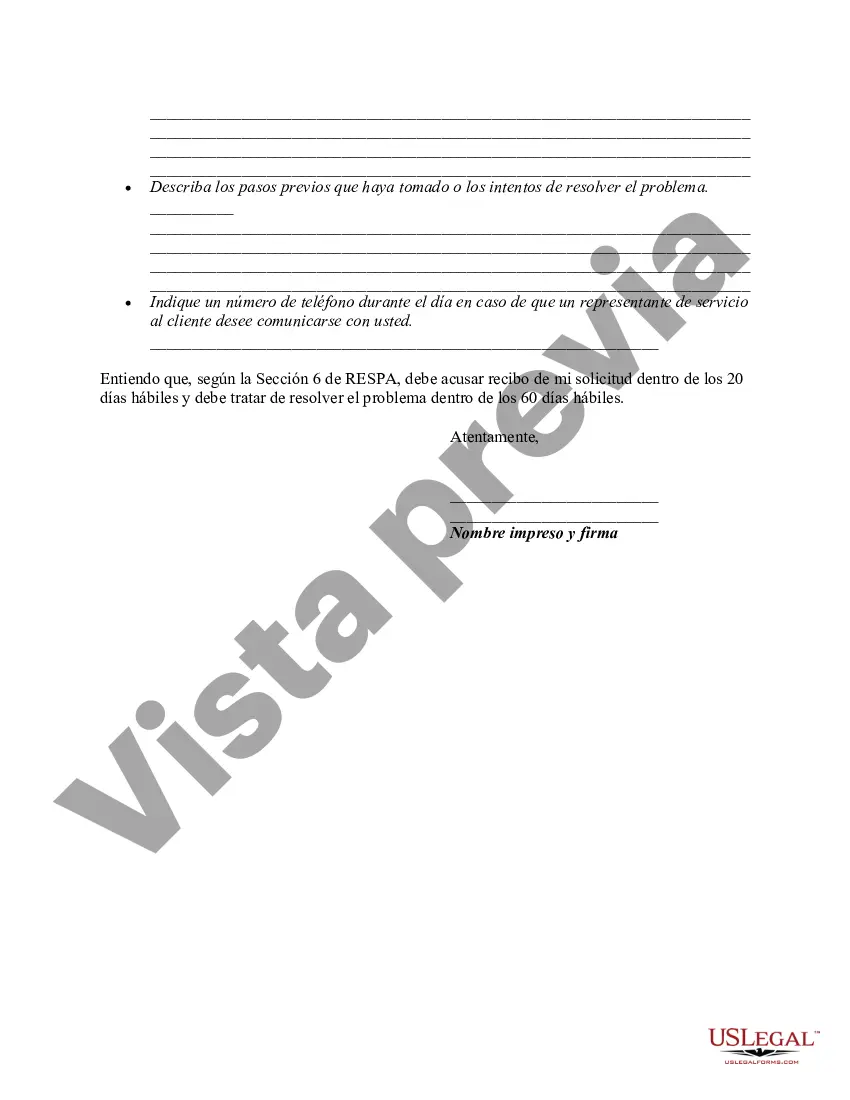

12 USC 2605(e) creates a duty of a loan servicer to respond to the inquiries of borrowers regarding loans covered by RESPA. If the borrower believes there is an error in the mortgage account, he or she can make a "qualified written request" to the loan servicer. The request must be in writing, identify the borrower by name and account, and include a statement of reasons why the borrower believes the account is in error. The request should include the words "qualified written request". It cannot be written on the payment coupon, but must be on a separate piece of paper. The Department of Housing and Urban Development provides a sample letter.

The servicer must acknowledge receipt of the request within 20 days. The servicer then has 60 days (from the request) to take action on the request. The servicer has to either provide a written notification that the error has been corrected, or provide a written explanation as to why the servicer believes the account is correct. Either way, the servicer has to provide the name and telephone number of a person with whom the borrower can discuss the matter.

Missouri Qualified Written Request (BWR) under Section 6 of the Real Estate Settlement Procedures Act (RESP) is a mechanism that allows consumers to request information, clarification, or resolution of issues related to their mortgage loan servicing. A BWR can be submitted by a borrower to their loan service when they have concerns about loan payments, account errors, escrow accounts, or any other specific issues regarding their mortgage. Under Section 6 of RESP, a BWR requires the loan service to provide a timely response to the borrower's inquiry and ensure that the information provided is accurate and complete. The objective of this provision is to protect consumers from unfair practices and ensure transparency in the mortgage loan servicing process. Some key elements of a Missouri BWR under Section 6 of RESP may include: 1. Borrower's Personal Information: The request should begin by providing the borrower's full name, address, contact information, and loan account number. This information is crucial for the loan service to identify the borrower and their loan. 2. Detailed Explanation of the Inquiry: The borrower should clearly and concisely describe the specific issue or concern they wish to address through the BWR. This can include payment discrepancies, improper fees or charges, unclear account statements, or any other issue related to their mortgage loan servicing. 3. Supporting Documentation: Whenever possible, the borrower should provide relevant documentation to support their inquiry. This can include copies of billing statements, receipts, correspondence, or any other documentation that helps to substantiate their claim or clarify the issue. 4. Requested Action: The borrower should clearly state their desired outcome or resolution. It can be a request for an investigation of the issue, correction of an error, clarification of a confusing aspect, or any other specific action required from the loan service. Different types of Missouri Was under Section 6 of RESP may include: 1. Payment Discrepancy BWR: This type of BWR can be submitted when there are concerns about incorrect or inconsistent loan payment calculations, improper application of payments, or irregularities in the payment history. 2. Escrow Account BWR: Borrowers may use this type of BWR to address issues related to their escrow accounts, such as discrepancies in escrow payment calculations, incorrect handling of escrow funds, or improper adjustments made by the loan service. 3. Account Statement BWR: When borrowers encounter difficulties understanding their mortgage loan account statements, they can submit this type of BWR to request clarification, breakdown of charges, or any other information required to comprehend their account status. 4. Loan Modification BWR: If a borrower is seeking a loan modification or has concerns regarding a previously approved modification, this type of BWR can be used to request information, clarification, or resolution on the modification terms and conditions. In conclusion, a Missouri BWR under Section 6 of RESP is a powerful tool for borrowers to safeguard their rights, seek information, and address concerns related to their mortgage loan servicing. By utilizing the BWR process, borrowers can ensure transparency, accuracy, and fairness in their mortgage transactions.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.