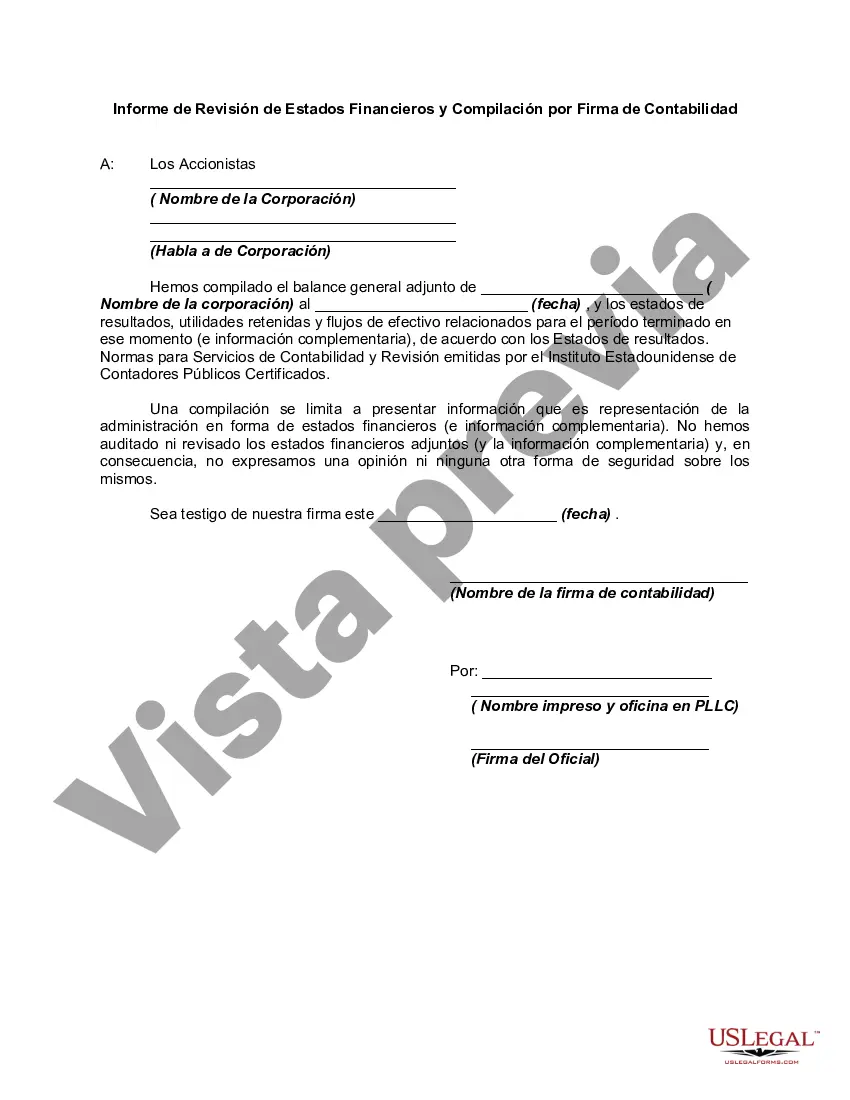

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Title: Understanding Mississippi Reports from Review of Financial Statements and Compilation by Accounting Firm Introduction: Mississippi Reports from Review of Financial Statements and Compilation by Accounting Firm play a crucial role in assessing and ensuring the accuracy and reliability of financial information. In this article, we will provide a detailed description of these reports, their purposes, and highlight different types if applicable. Let's dive in! 1. The Importance of Mississippi Reports from Review of Financial Statements: Mississippi Reports from Review of Financial Statements by Accounting Firm serve as critical tools for businesses and organizations in evaluating the accuracy of their financial statements. They go through an in-depth examination, testing, and analysis of the financial data to provide reasonable assurance about its accuracy. 2. Purpose of Mississippi Reports from Review of Financial Statements: The main objective of the Mississippi Reports from Review of Financial Statements is to ensure that financial statements fairly represent the entity's financial position, financial performance, cash flows, and related disclosures. They serve as a vital resource for stakeholders, shareholders, management, lenders, investors, and regulatory bodies to make informed decisions. 3. Components of Mississippi Reports from Review of Financial Statements: While the specific components may vary depending on the accounting firm and the requirements of the engagement, typically, Mississippi Reports from Review of Financial Statements comprise: a. Management Representations: The accounting firm obtains written representations from the management confirming the accuracy of the financial statements and its compliance with applicable accounting standards. b. Inquiry and Analytical Procedures: The accounting firm conducts inquiries with management and performs analytical procedures to identify any inconsistencies or potential errors in the financial statements. c. Assessing Risk of Material Misstatement: The accounting firm evaluates the risks of material misstatement, focusing on significant accounts, transactions, and relevant internal controls. d. Limited Assurance Report: The accounting firm issues a report providing limited assurance that they have not become aware of any material modifications required in the financial statements to comply with the applicable accounting standards. 4. Types of Mississippi Reports from Review of Financial Statements (if applicable): It is important to note that Mississippi laws may not explicitly classify different types of reports resulting from the review of financial statements. Nevertheless, accounting firms may utilize terminology such as "unqualified review report," "qualified review report," or "adverse review report" to indicate the level of assurance provided. a. Unqualified Review Report: This report is issued when the accounting firm concludes that the financial statements present fairly, in all material respects, the entity's financial position, results of operations, and cash flows, in accordance with the applicable accounting standards. b. Qualified Review Report: A qualified review report is generated when the accounting firm concludes that the financial statements present fairly, except specific areas or issues where material misstatements may exist. c. Adverse Review Report: An adverse review report is issued when the accounting firm concludes that the financial statements are materially misstated and do not present fairly the entity's financial position, results of operations, and cash flows. Conclusion: Mississippi Reports from Review of Financial Statements and Compilation by Accounting Firm offer stakeholders a reliable assessment of the accuracy and reliability of financial information. They serve as critical tools for decision-making processes. Understanding the components and potential types of these reports allows businesses and organizations to better interpret and utilize the information they provide for their financial management and compliance requirements.Title: Understanding Mississippi Reports from Review of Financial Statements and Compilation by Accounting Firm Introduction: Mississippi Reports from Review of Financial Statements and Compilation by Accounting Firm play a crucial role in assessing and ensuring the accuracy and reliability of financial information. In this article, we will provide a detailed description of these reports, their purposes, and highlight different types if applicable. Let's dive in! 1. The Importance of Mississippi Reports from Review of Financial Statements: Mississippi Reports from Review of Financial Statements by Accounting Firm serve as critical tools for businesses and organizations in evaluating the accuracy of their financial statements. They go through an in-depth examination, testing, and analysis of the financial data to provide reasonable assurance about its accuracy. 2. Purpose of Mississippi Reports from Review of Financial Statements: The main objective of the Mississippi Reports from Review of Financial Statements is to ensure that financial statements fairly represent the entity's financial position, financial performance, cash flows, and related disclosures. They serve as a vital resource for stakeholders, shareholders, management, lenders, investors, and regulatory bodies to make informed decisions. 3. Components of Mississippi Reports from Review of Financial Statements: While the specific components may vary depending on the accounting firm and the requirements of the engagement, typically, Mississippi Reports from Review of Financial Statements comprise: a. Management Representations: The accounting firm obtains written representations from the management confirming the accuracy of the financial statements and its compliance with applicable accounting standards. b. Inquiry and Analytical Procedures: The accounting firm conducts inquiries with management and performs analytical procedures to identify any inconsistencies or potential errors in the financial statements. c. Assessing Risk of Material Misstatement: The accounting firm evaluates the risks of material misstatement, focusing on significant accounts, transactions, and relevant internal controls. d. Limited Assurance Report: The accounting firm issues a report providing limited assurance that they have not become aware of any material modifications required in the financial statements to comply with the applicable accounting standards. 4. Types of Mississippi Reports from Review of Financial Statements (if applicable): It is important to note that Mississippi laws may not explicitly classify different types of reports resulting from the review of financial statements. Nevertheless, accounting firms may utilize terminology such as "unqualified review report," "qualified review report," or "adverse review report" to indicate the level of assurance provided. a. Unqualified Review Report: This report is issued when the accounting firm concludes that the financial statements present fairly, in all material respects, the entity's financial position, results of operations, and cash flows, in accordance with the applicable accounting standards. b. Qualified Review Report: A qualified review report is generated when the accounting firm concludes that the financial statements present fairly, except specific areas or issues where material misstatements may exist. c. Adverse Review Report: An adverse review report is issued when the accounting firm concludes that the financial statements are materially misstated and do not present fairly the entity's financial position, results of operations, and cash flows. Conclusion: Mississippi Reports from Review of Financial Statements and Compilation by Accounting Firm offer stakeholders a reliable assessment of the accuracy and reliability of financial information. They serve as critical tools for decision-making processes. Understanding the components and potential types of these reports allows businesses and organizations to better interpret and utilize the information they provide for their financial management and compliance requirements.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.