Statutory provisions in the various jurisdictions specify the formal requisites of a valid will. Also, in the absence of pertinent will provisions, the statutes generally govern the construction of a will and determine the effect of various acts or events on the will, such as the testator's subsequent marriage or divorce, or the birth or adoption of children after the execution of the will.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

When drafting wills, practitioners should beware of the perfunctory use of standard boilerplate language directing that all taxes be paid out of the residue of the estate. Because a number of Internal Revenue Code provisions include non-probate assets in the taxable estate if they pass as a result of the decedent's death, the result of such boilerplate could be to cause the residuary beneficiary to pay taxes on assets that pass to others, often wiping out the residuary estate altogether -- a circumstance probably not intended by the testator. In addition to the problems that may result for beneficiaries, the estate may also suffer if the residuary beneficiary is a charity or spouse, since the marital or charitable deduction can be drastically reduced by the necessity of paying taxes out of the residue, resulting in considerably higher taxes. Attorneys should discuss with their clients the existence of non-probate assets and the distribution of the tax burden.

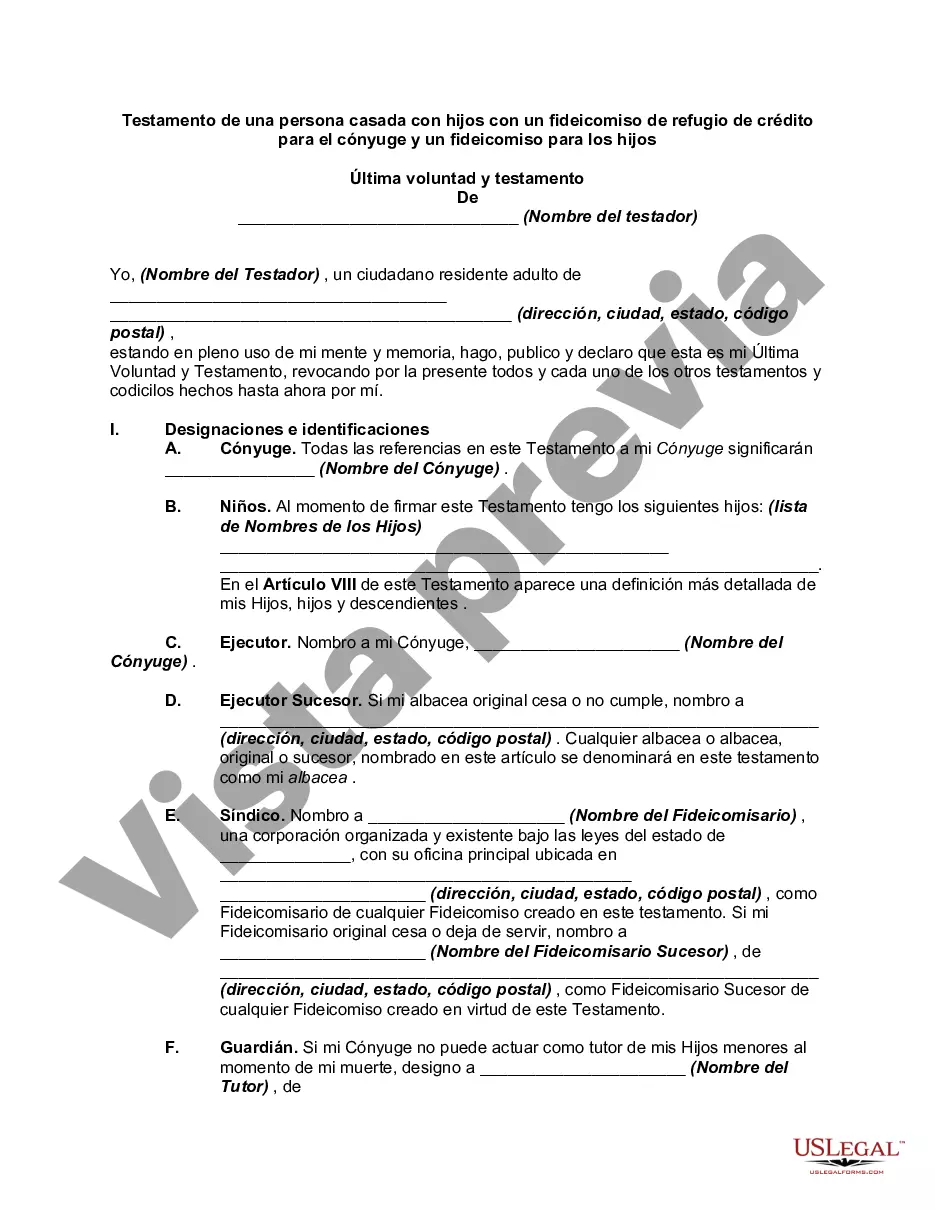

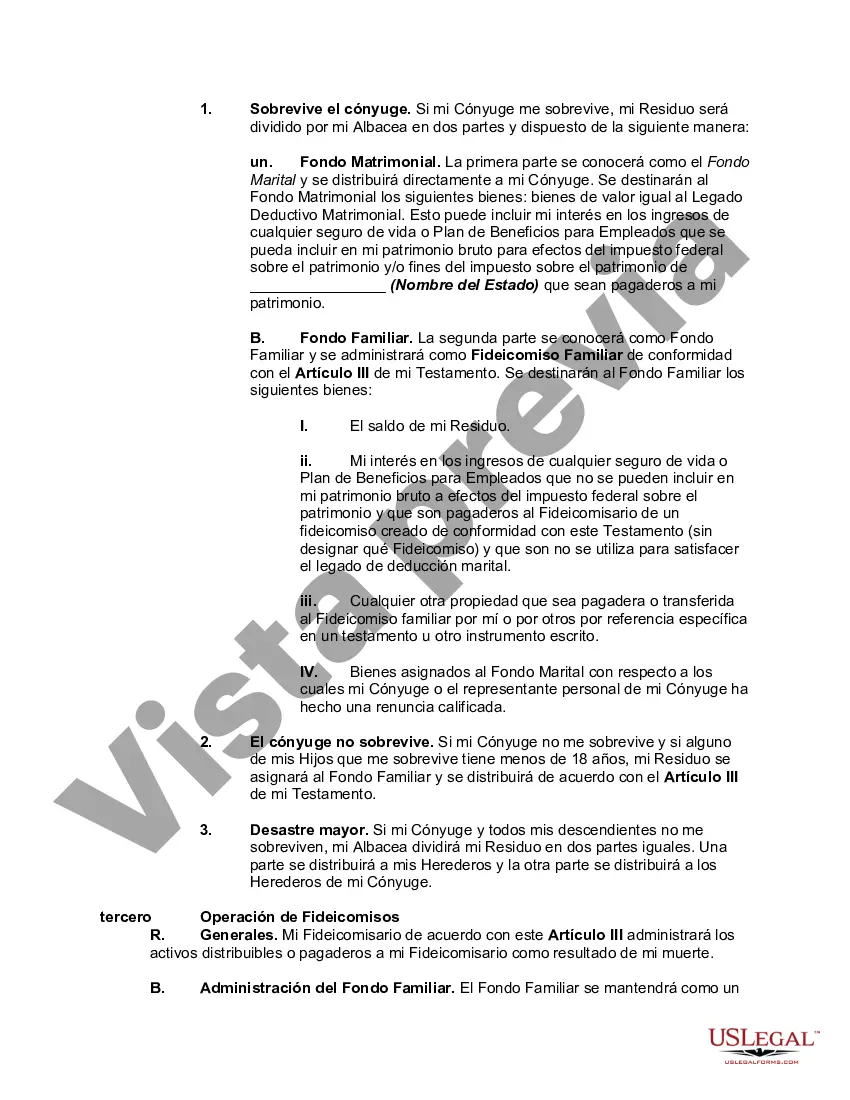

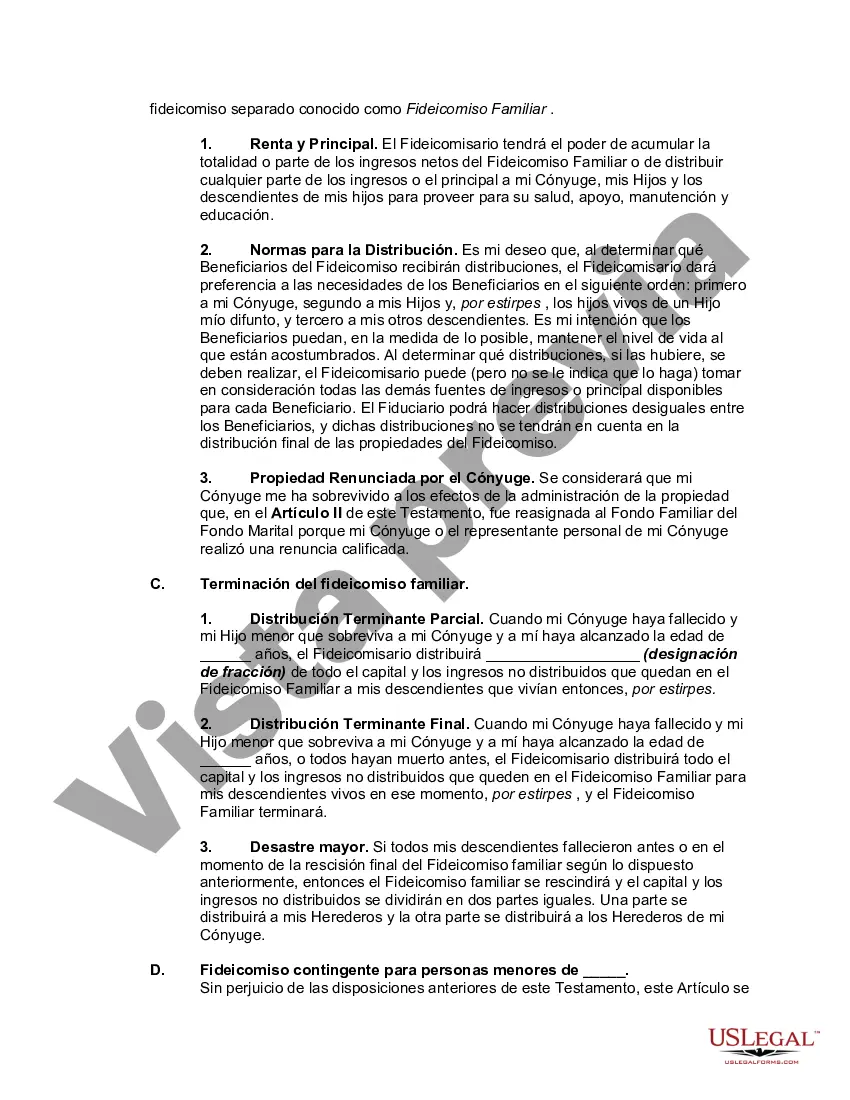

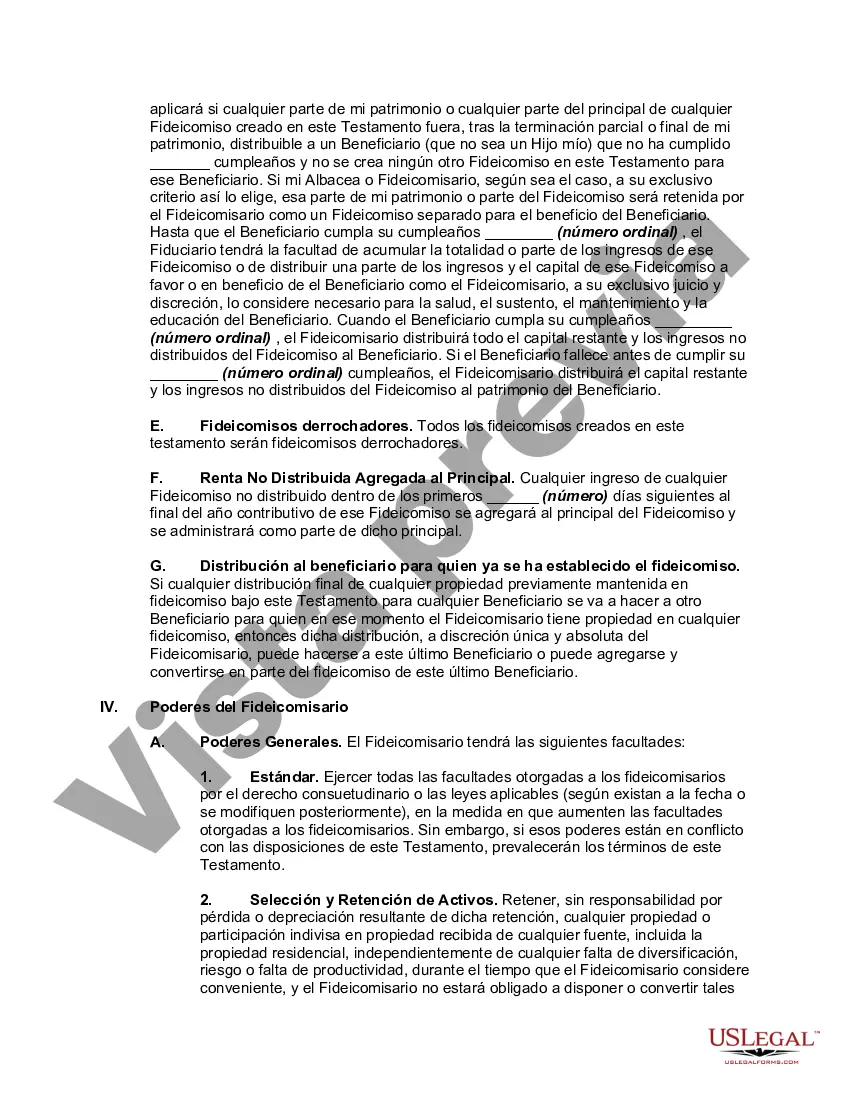

A Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse is a legal document that allows married individuals in Mississippi to ensure the protection and distribution of their assets after their passing while still providing for their spouse and children. This type of will is particularly advantageous for couples who wish to minimize estate taxes and maximize their estate planning strategies. A Credit Shelter Trust, also known as a bypass trust or family trust, is a common provision found within this type of will. It allows the deceased spouse to transfer assets up to the federal estate tax exemption to a trust, the "credit shelter trust," upon their death. This trust provides the surviving spouse with income or other benefits during their lifetime, while preserving the principal for the children or other beneficiaries upon the surviving spouse's death. By utilizing a credit shelter trust, couples can effectively double the estate tax exemption amount and help minimize the tax burden on their estate. There are different variations of the Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse, depending on the specific needs and goals of the couple. Some common types include: 1. Simple Credit Shelter Trust: This option allows the deceased spouse to transfer their assets, up to the estate tax exemption limit, to a trust for the benefit of the surviving spouse and children. The surviving spouse receives income generated by the trust assets and may have the ability to access the principal under certain circumstances. 2. Marital TIP Trust: TIP stands for "Qualified Terminable Interest Property." With this trust, the surviving spouse is entitled to receive income from the trust assets for their lifetime. Upon their death, the remaining trust principal passes to the designated beneficiaries, typically the children. This type of trust offers flexibility and can enable the surviving spouse to benefit from the trust assets while still providing for the children. 3. Irrevocable Life Insurance Trust (IIT): Although not specifically a credit shelter trust, an IIT is often incorporated alongside a Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse. It allows the insured individual to remove the life insurance proceeds from their estate, potentially reducing estate taxes. The IIT owns the life insurance policy, and upon the insured's death, the trust receives the insurance proceeds, which can then be distributed to the surviving spouse or children according to the terms outlined in the trust. In summary, a Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse is a comprehensive estate planning tool that enables married individuals to provide for their loved ones while minimizing estate taxes. Depending on specific circumstances, different types of trusts can be incorporated within the will to achieve the desired goals of asset distribution and protection. It is essential to consult with an experienced estate planning attorney to ensure that the document accurately reflects your intentions and meets the legal requirements of Mississippi law.A Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse is a legal document that allows married individuals in Mississippi to ensure the protection and distribution of their assets after their passing while still providing for their spouse and children. This type of will is particularly advantageous for couples who wish to minimize estate taxes and maximize their estate planning strategies. A Credit Shelter Trust, also known as a bypass trust or family trust, is a common provision found within this type of will. It allows the deceased spouse to transfer assets up to the federal estate tax exemption to a trust, the "credit shelter trust," upon their death. This trust provides the surviving spouse with income or other benefits during their lifetime, while preserving the principal for the children or other beneficiaries upon the surviving spouse's death. By utilizing a credit shelter trust, couples can effectively double the estate tax exemption amount and help minimize the tax burden on their estate. There are different variations of the Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse, depending on the specific needs and goals of the couple. Some common types include: 1. Simple Credit Shelter Trust: This option allows the deceased spouse to transfer their assets, up to the estate tax exemption limit, to a trust for the benefit of the surviving spouse and children. The surviving spouse receives income generated by the trust assets and may have the ability to access the principal under certain circumstances. 2. Marital TIP Trust: TIP stands for "Qualified Terminable Interest Property." With this trust, the surviving spouse is entitled to receive income from the trust assets for their lifetime. Upon their death, the remaining trust principal passes to the designated beneficiaries, typically the children. This type of trust offers flexibility and can enable the surviving spouse to benefit from the trust assets while still providing for the children. 3. Irrevocable Life Insurance Trust (IIT): Although not specifically a credit shelter trust, an IIT is often incorporated alongside a Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse. It allows the insured individual to remove the life insurance proceeds from their estate, potentially reducing estate taxes. The IIT owns the life insurance policy, and upon the insured's death, the trust receives the insurance proceeds, which can then be distributed to the surviving spouse or children according to the terms outlined in the trust. In summary, a Mississippi Married Person's Will with Children with a Credit Shelter Trust for Spouse is a comprehensive estate planning tool that enables married individuals to provide for their loved ones while minimizing estate taxes. Depending on specific circumstances, different types of trusts can be incorporated within the will to achieve the desired goals of asset distribution and protection. It is essential to consult with an experienced estate planning attorney to ensure that the document accurately reflects your intentions and meets the legal requirements of Mississippi law.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.