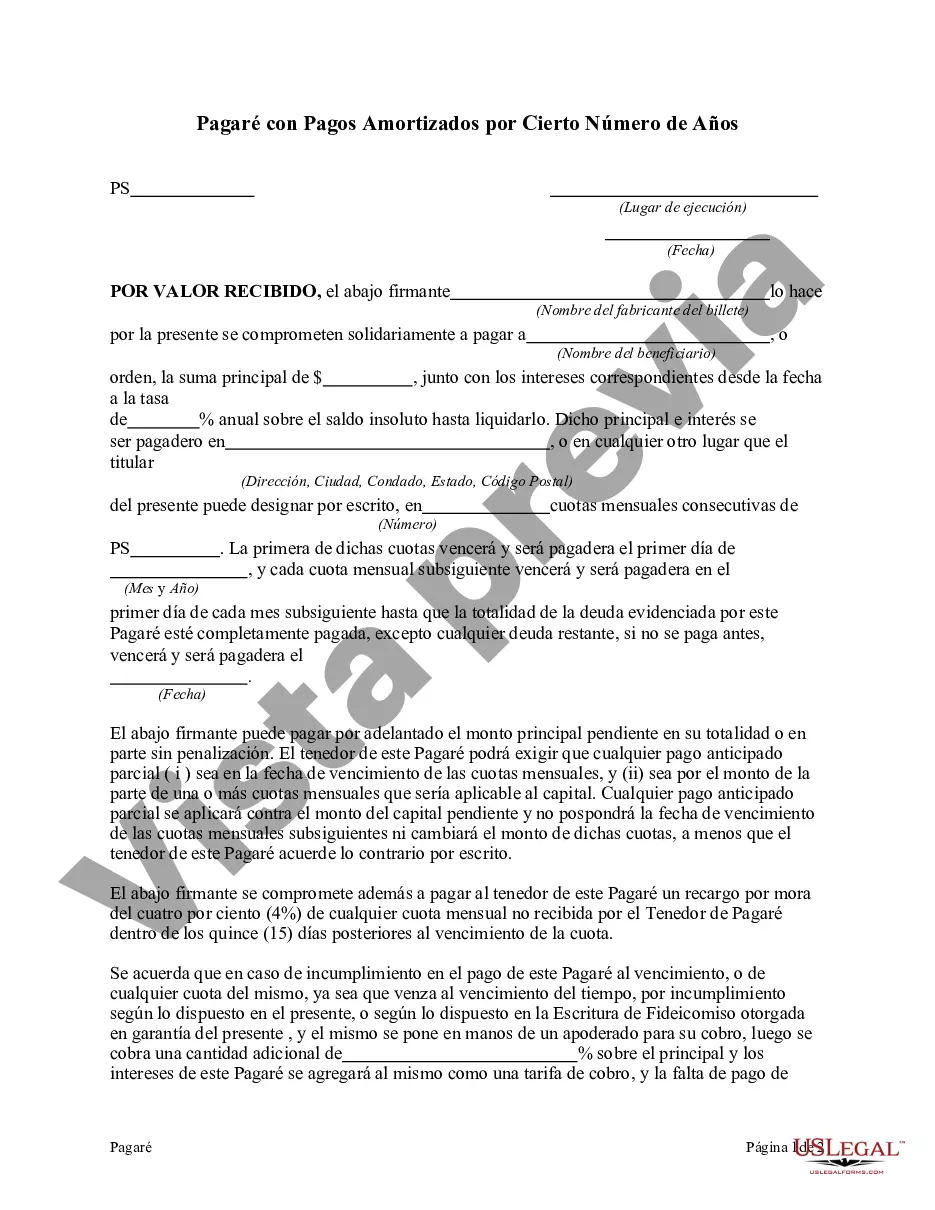

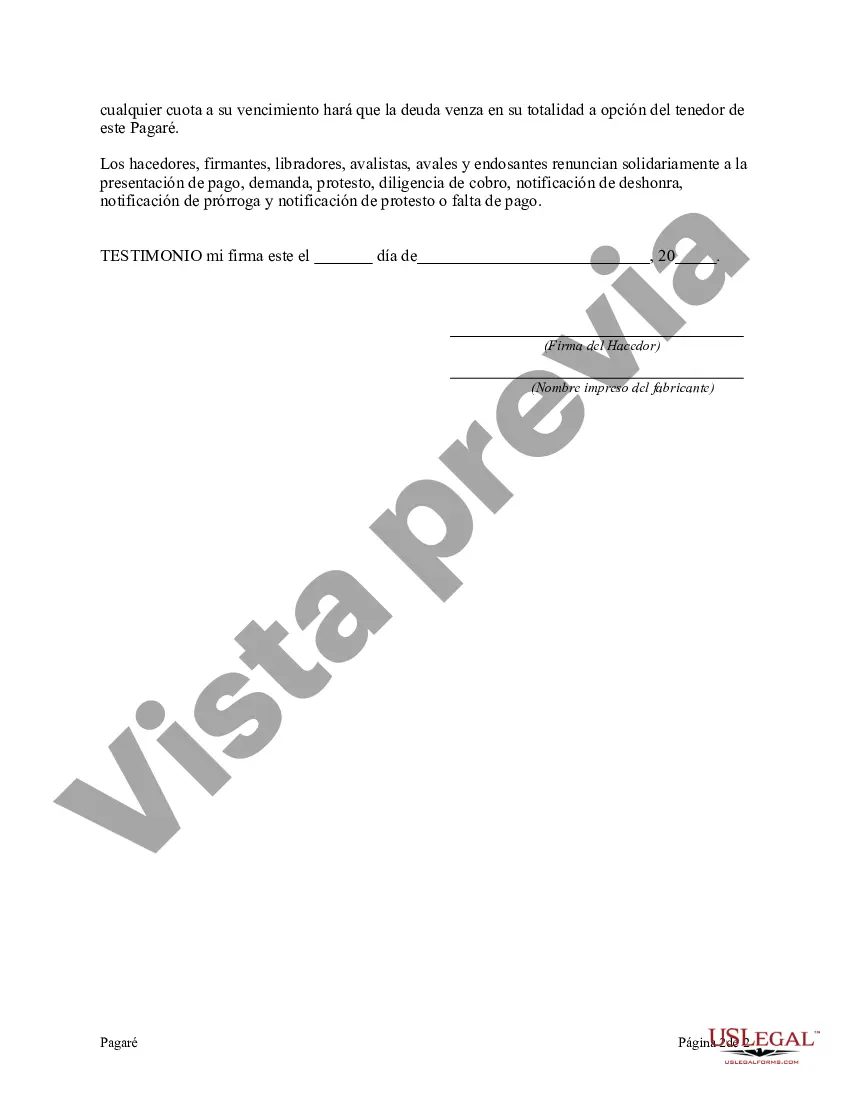

A Montana Promissory Note with Payments Amortized for a Certain Number of Years is a legally binding document that outlines a loan agreement between a lender and a borrower in Montana. This promissory note specifies the terms and conditions of the loan, including the repayment schedule and interest rate, while also providing security to both parties involved. In this type of promissory note, the payments are structured to be amortized over a specific number of years. Amortization refers to the gradual reduction of the loan principal balance through regular installment payments, ensuring that both interest and principal are paid off by the end of the specified period. This arrangement enables borrowers to have a more predictable repayment plan, as they know exactly how much needs to be paid each period. Montana Promissory Notes with payments amortized for a certain number of years can be categorized into two main types: fixed-rate and adjustable-rate promissory notes. 1. Fixed-Rate Promissory Note: In this type, the interest rate remains constant throughout the loan term. The borrower agrees to make regular payments for a specific number of years, with each payment including both principal and interest portions. This stability allows borrowers to plan their finances as the repayment amount remains consistent. 2. Adjustable-Rate Promissory Note: Unlike fixed-rate notes, the interest rate in adjustable-rate promissory notes can fluctuate over time. The initial interest rate is determined by the lender, often based on an index such as the U.S. Prime Rate or the London Interbank Offered Rate (LIBOR). After an initial fixed rate period, the interest rate may adjust periodically, typically annually, based on changes in the chosen index. While this type of promissory note offers potential benefits such as lower initial interest rates, borrowers should be aware that payments may increase if the interest rate rises. Overall, a Montana Promissory Note with Payments Amortized for a Certain Number of Years provides a structured repayment plan for borrowers and lenders alike. It ensures that loan obligations are fulfilled over a set timetable, offering clarity and transparency throughout the loan term. Before entering into any promissory note agreement, it is advisable to consult legal professionals to ensure all legal requirements and obligations are fully understood and adhered to.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.Montana Pagaré con Pagos Amortizados por Cierto Número de Años - Promissory Note with Payments Amortized for a Certain Number of Years

Description

How to fill out Montana Pagaré Con Pagos Amortizados Por Cierto Número De Años?

Choosing the right legal document design could be a struggle. Naturally, there are plenty of layouts available on the net, but how do you find the legal form you will need? Make use of the US Legal Forms web site. The support provides a huge number of layouts, like the Montana Promissory Note with Payments Amortized for a Certain Number of Years, that you can use for business and personal demands. All the varieties are checked out by professionals and meet state and federal specifications.

Should you be already authorized, log in to your bank account and then click the Acquire option to find the Montana Promissory Note with Payments Amortized for a Certain Number of Years. Utilize your bank account to check through the legal varieties you might have ordered previously. Check out the My Forms tab of the bank account and acquire another copy of your document you will need.

Should you be a new end user of US Legal Forms, here are basic directions so that you can stick to:

- Very first, ensure you have chosen the correct form for your city/area. You may examine the form using the Preview option and study the form information to make sure it will be the best for you.

- In the event the form does not meet your preferences, utilize the Seach area to obtain the correct form.

- When you are positive that the form would work, click on the Buy now option to find the form.

- Select the pricing strategy you want and enter in the necessary information and facts. Make your bank account and pay for an order using your PayPal bank account or bank card.

- Pick the document formatting and acquire the legal document design to your system.

- Total, revise and printing and indication the received Montana Promissory Note with Payments Amortized for a Certain Number of Years.

US Legal Forms is definitely the greatest collection of legal varieties in which you will find a variety of document layouts. Make use of the service to acquire professionally-produced papers that stick to condition specifications.