North Carolina Credit Inquiry: Understanding Different Types and their Significance In the world of finance and credit, a North Carolina Credit Inquiry refers to the process of accessing an individual's credit information by authorized entities. This inquiry provides a comprehensive overview of a person's credit history, allowing potential lenders, employers, or landlords to assess creditworthiness and make informed decisions. It plays a crucial role in determining whether the individual is a responsible borrower and capable of managing financial obligations. There are primarily two types of North Carolina Credit Inquiries: hard inquiries and soft inquiries. Understanding the distinctions between these inquiries is essential to comprehend their impact on credit scores and overall financial well-being. 1. Hard Inquiries: Hard inquiries are typically initiated by lenders when an individual applies for credit, such as a mortgage, auto loan, or credit card. These inquiries require the applicant's consent and involve accessing detailed credit reports from one or more credit bureaus, including Experian, Equifax, and TransUnion. Hard inquiries usually occur when someone actively seeks new credit, implying potential financial obligations. The significance of hard inquiries lies in their impact on credit scores. Each hard inquiry can slightly lower the credit score, usually by a few points. Frequent and multiple hard inquiries within a short span can indicate higher credit risk to potential lenders, potentially making it challenging to secure favorable credit terms in the future. However, it is important to note that credit scoring models recognize that consumers often shop around for the best rates on loans, such as mortgages or auto loans, and treat multiple inquiries for a single type of loan as a single inquiry if done within a specific timeframe (typically 14-45 days). 2. Soft Inquiries: Unlike hard inquiries, soft inquiries have no direct impact on credit scores. These inquiries occur when individuals or institutions access credit reports for purposes other than the extension of credit. For instance, soft inquiries may occur when an individual checks their own credit report, when employers conduct background checks, or when credit card companies perform pre-screening for potential customers. Soft inquiries provide a general overview of an individual's credit history without going into as much detail as hard inquiries. Soft inquiries are significantly less stressful than hard inquiries since they don't affect creditworthiness or future credit opportunities. However, individuals should still monitor their credit reports regularly, as observing any unauthorized soft inquiries may indicate potential identity theft or fraud attempts. In conclusion, North Carolina Credit Inquiry encompasses the process of evaluating an individual's credit information. While hard inquiries impact credit scores and reflect active credit-seeking behavior, soft inquiries offer general overviews for various purposes without affecting creditworthiness. By understanding these distinctions and monitoring credit reports, individuals can make well-informed financial decisions and ensure the accuracy and security of their credit profiles.

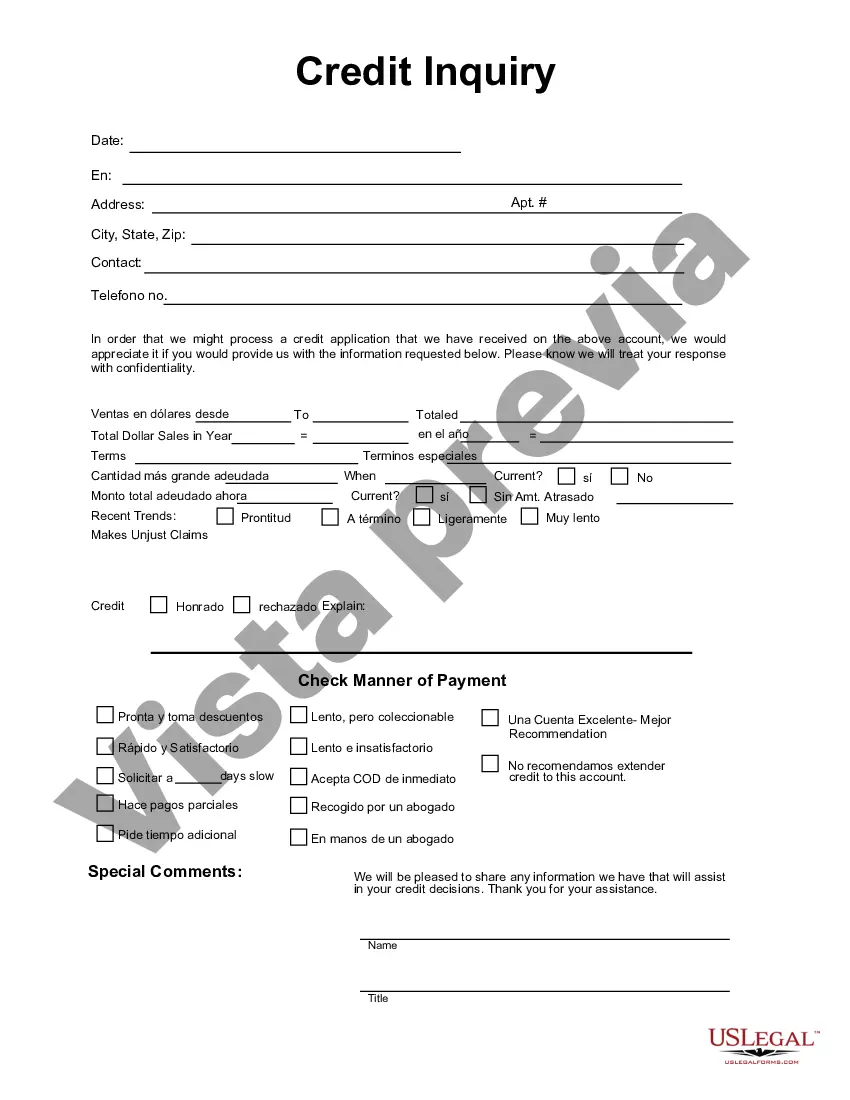

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.North Carolina Consulta de crédito - Credit Inquiry

Description

How to fill out North Carolina Consulta De Crédito?

Are you presently within a place where you require documents for sometimes organization or specific uses just about every day time? There are tons of lawful record web templates accessible on the Internet, but discovering kinds you can rely on isn`t simple. US Legal Forms gives a large number of form web templates, like the North Carolina Credit Inquiry, which are published to satisfy federal and state requirements.

In case you are currently knowledgeable about US Legal Forms site and possess an account, just log in. Next, you are able to down load the North Carolina Credit Inquiry format.

Should you not offer an bank account and want to start using US Legal Forms, follow these steps:

- Obtain the form you need and ensure it is for that appropriate city/region.

- Use the Review option to check the form.

- Look at the explanation to ensure that you have selected the correct form.

- If the form isn`t what you`re seeking, use the Lookup discipline to discover the form that meets your needs and requirements.

- If you find the appropriate form, simply click Purchase now.

- Opt for the costs prepare you want, submit the required information to create your account, and purchase your order using your PayPal or charge card.

- Choose a handy paper structure and down load your backup.

Get each of the record web templates you possess purchased in the My Forms food selection. You can aquire a further backup of North Carolina Credit Inquiry anytime, if needed. Just go through the essential form to down load or print out the record format.

Use US Legal Forms, probably the most substantial selection of lawful varieties, in order to save time as well as stay away from errors. The service gives professionally created lawful record web templates which you can use for an array of uses. Create an account on US Legal Forms and start generating your life a little easier.