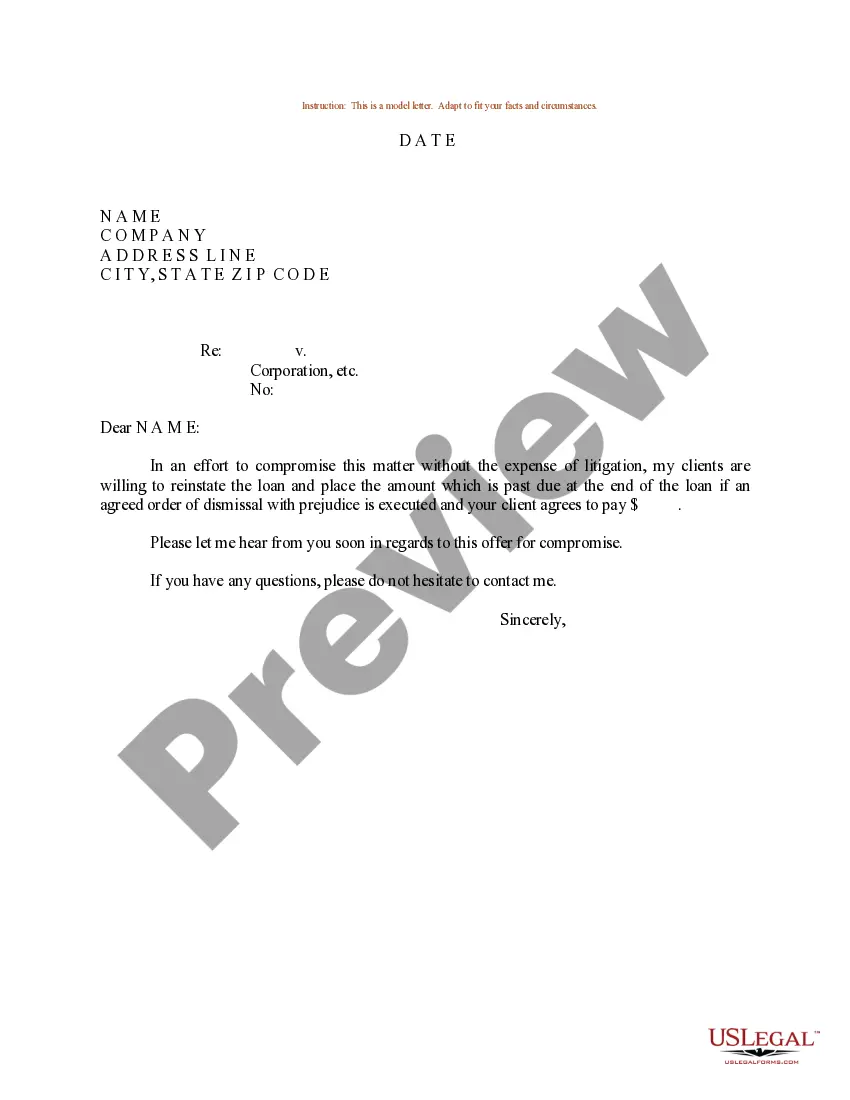

North Dakota Sample Letter for Insufficient Amount to Reinstate Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter For Insufficient Amount To Reinstate Loan?

You can spend several hours online searching for the legal document template that meets the federal and state requirements you will need.

US Legal Forms offers an extensive collection of legal documents that can be reviewed by professionals.

You can conveniently obtain or print the North Dakota Sample Letter for Insufficient Amount to Reinstate Loan with my assistance.

If available, use the Review button to scan the document template simultaneously.

- If you already possess a US Legal Forms account, you can Log In and click the Acquire button.

- After that, you can complete, modify, print, or sign the North Dakota Sample Letter for Insufficient Amount to Reinstate Loan.

- Every legal document template you obtain is yours permanently.

- To retrieve another copy of any obtained form, visit the My documents tab and click on the appropriate button.

- If you're visiting the US Legal Forms site for the first time, follow the simple instructions below.

- First, ensure you've selected the correct document template for the area/city of your choice.

- Review the document description to confirm you've chosen the appropriate template.

Form popularity

FAQ

Issuing a debt validation letter is often a wise decision, as it helps protect your rights as a consumer. By requesting proof of the debt, you verify its legitimacy and allow yourself time to gather necessary information. Utilizing a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan can aid in this process, ensuring that your letter is both professional and assertive.

To compose a validation of debt letter, begin with your contact information at the top of the page. Clearly state that you are requesting verification of the outstanding debt, and include details about the debt itself. Using a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan can help provide a clear framework for your letter, making sure you request all necessary information effectively.

In North Dakota, most debts become uncollectible after a period of six years. This period begins from the date of the last payment or acknowledgment of the debt. Knowing this timeframe is crucial for consumers; you may want to reference a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan if you seek to negotiate or dispute the debt before it reaches this limit.

When creating a debt validation letter, be sure to include your name, address, and account details. Clearly state that you dispute the debt and request verification. Using a template or a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan can streamline this process, ensuring you cover all necessary components while presenting your case effectively.

To complete a creditor proof of debt form, start by providing basic information about the debtor, such as their name and address. Next, specify the total debt amount and include relevant dates related to the debt. You may find it easier to organize this information by using a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan as a guide when preparing your documentation.

The 7 7 7 rule relates to debt collection practices. It states that creditors must provide specific information about the debt within seven days after first contacting you. This includes details about the amount owed, the creditor's name, and a notice of your rights. Understanding this rule can empower you to seek a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan, should you need to communicate with creditors.

In North Dakota, a judgment typically lasts for ten years before it can expire. However, a creditor may renew the judgment, effectively extending the time frame for collection. If you find yourself facing a judgment, a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan may provide a structured way to negotiate payments or address the judgment directly.

The eleven-word phrase to stop debt collectors is straightforward: 'Please cease all communication with me regarding this debt immediately.' Using this phrase can inform debt collectors that you do not wish to hear from them anymore. If you're dealing with overwhelming debt, consider drafting a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan to formalize your communication.

To craft a forgiveness letter for credit, start by addressing the creditor directly and stating your purpose clearly. Provide context for the request, such as changes in your financial circumstances, and affirm your commitment to resolve the issue. Mention any supporting documents that justify your request and consider referring to a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan for formatting guidance.

When writing a debt relief letter, begin by outlining your current financial situation. Clearly explain why you are unable to meet your obligations and request a specific debt relief solution. Use a respectful tone and include any supporting documents that may strengthen your case. For inspiration, a North Dakota Sample Letter for Insufficient Amount to Reinstate Loan can serve as a helpful template.