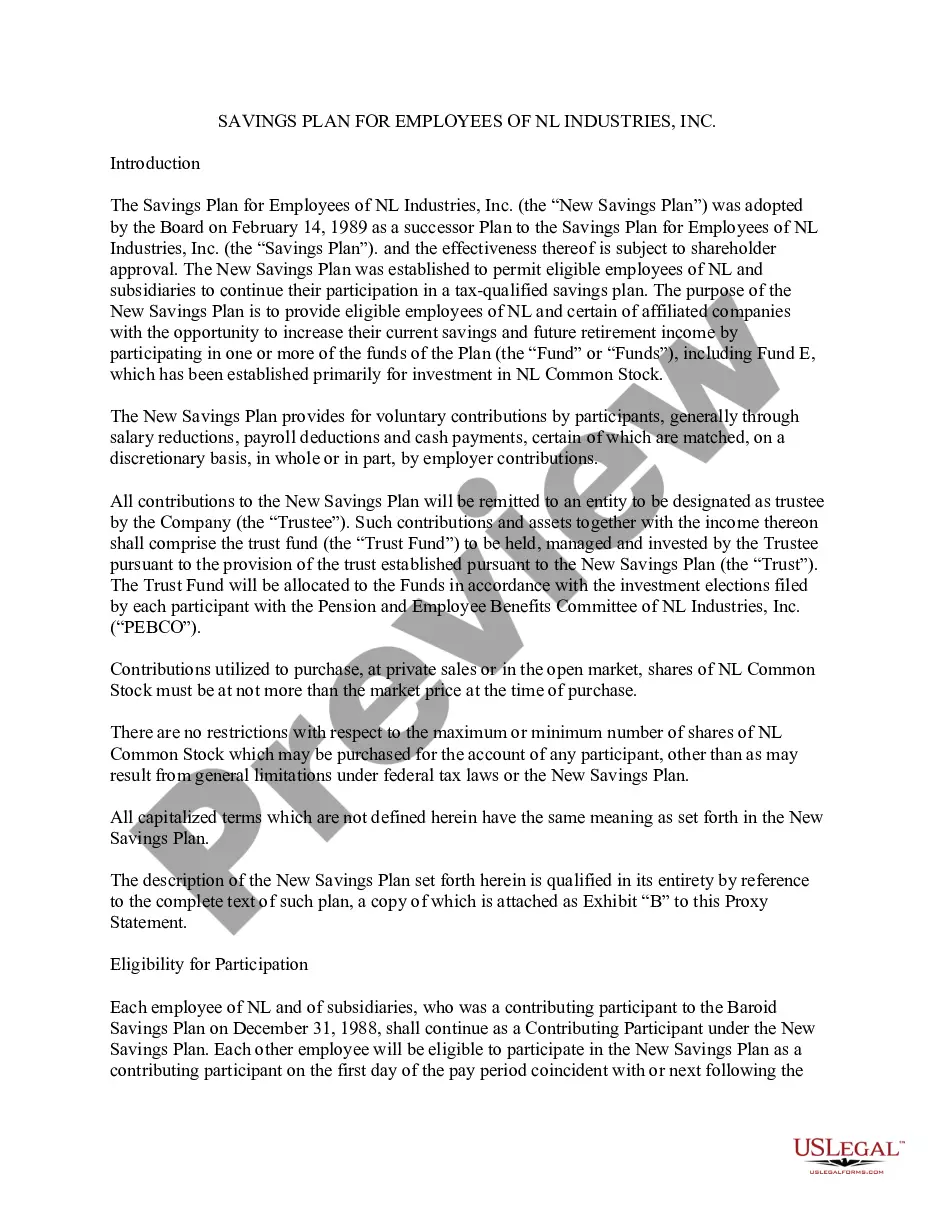

22-109E 22-109E . . . Employee Savings Plan (401(k) Plan) under which (a) participants make voluntary contributions through salary reductions, payroll deductions and/or cash payments, certain of which are matched in whole or in part by employer contributions and (b) such contributions are allocated to one or more investment funds in accordance with investment elections of each participant

Nebraska Savings Plan for Employees

Category:

State:

Multi-State

Control #:

US-CC-22-109E

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Savings Plan For Employees?

Discovering the right legitimate file template could be a battle. Naturally, there are a lot of layouts available on the Internet, but how can you discover the legitimate form you will need? Utilize the US Legal Forms internet site. The service delivers a large number of layouts, for example the Nebraska Savings Plan for Employees, that can be used for company and private requirements. Every one of the kinds are inspected by experts and satisfy federal and state requirements.

If you are already authorized, log in to the profile and click on the Download key to have the Nebraska Savings Plan for Employees. Utilize your profile to check through the legitimate kinds you may have acquired previously. Visit the My Forms tab of the profile and get yet another version of your file you will need.

If you are a brand new end user of US Legal Forms, listed below are simple guidelines for you to comply with:

- Very first, ensure you have chosen the right form to your area/county. You are able to look over the shape utilizing the Review key and browse the shape information to make certain this is the right one for you.

- If the form will not satisfy your expectations, utilize the Seach discipline to get the right form.

- When you are certain the shape would work, click the Get now key to have the form.

- Select the pricing plan you desire and type in the essential information and facts. Create your profile and pay money for your order with your PayPal profile or charge card.

- Opt for the submit structure and down load the legitimate file template to the device.

- Complete, modify and printing and indicator the acquired Nebraska Savings Plan for Employees.

US Legal Forms is definitely the biggest library of legitimate kinds where you can see different file layouts. Utilize the service to down load professionally-created paperwork that comply with condition requirements.

Form popularity

FAQ

Plan Overview. In 1976, the board implemented the State of Nebraska Deferred Compensation Plan (DCP). DCP, as authorized by IRS Code §457, is a voluntary retirement savings plan which allows state employees the ability to defer and invest a portion of their compensation for retirement.

The two plans are also different in that 401(k) plans do not offer a three-year Pre-Retirement Catch-Up; and 457(b) plans do. Another difference is that a 401(k) distribution prior to age 59½ may be subject to a 10% early withdrawal penalty and 457(b) plans generally do not have the same early withdrawal penalty.

Cons of 457(b) plans: Fewer investing options than 401(k)s (Not as common today) Only available to certain employees employed by state or local governments or qualifying nonprofits. Employer contributions count toward the annual limit. Non-governmental 457(b) plans are riskier.

Employer-sponsored savings plans such as 401(k) and Roth 401(k) plans provide employees with an automatic way to save for their retirement while benefiting from tax breaks. The reward to employees who participate in these programs is they essentially receive free money when their employers offer matching contributions.

Since most government employees already have a pension, a defined contribution plan such as a 457(b) is considered a supplemental savings plan, and so an employer match is uncommon.

Cash Balance Benefit The assets are held in a trust fund which is managed by the Nebraska Investment Council. Cash Balance Benefit participants are guaranteed an annual interest credit rate which is defined in statute as the greater of 5% or the federal mid-term rate plus 1.5%.

A 401(k) Plan is a defined contribution plan that is a cash or deferred arrangement. Employees can elect to defer receiving a portion of their salary which is instead contributed on their behalf, before taxes, to the 401(k) plan. Sometimes the employer may match these contributions.

Plans eligible under 457(b) allow employees of sponsoring organizations to defer income taxation on retirement savings into future years.