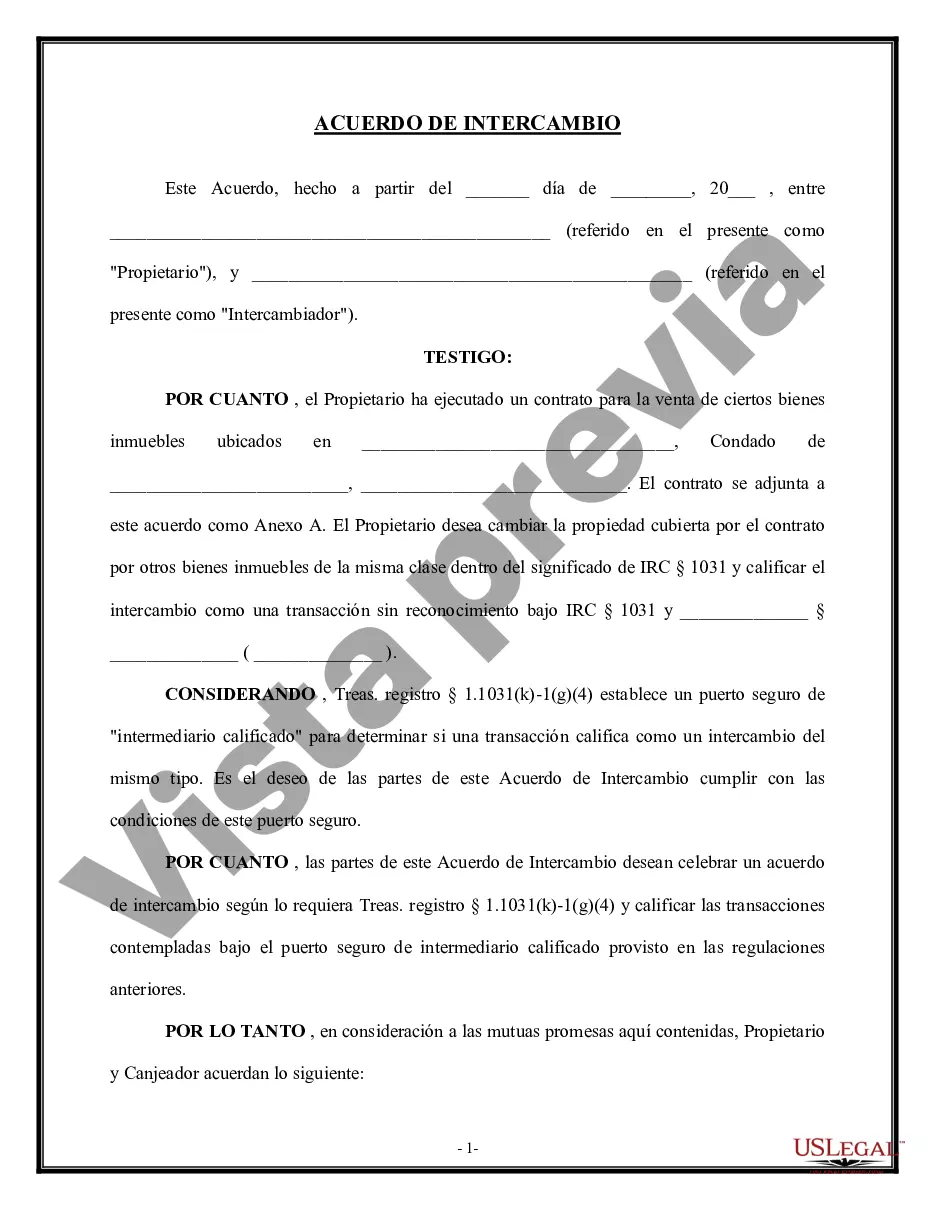

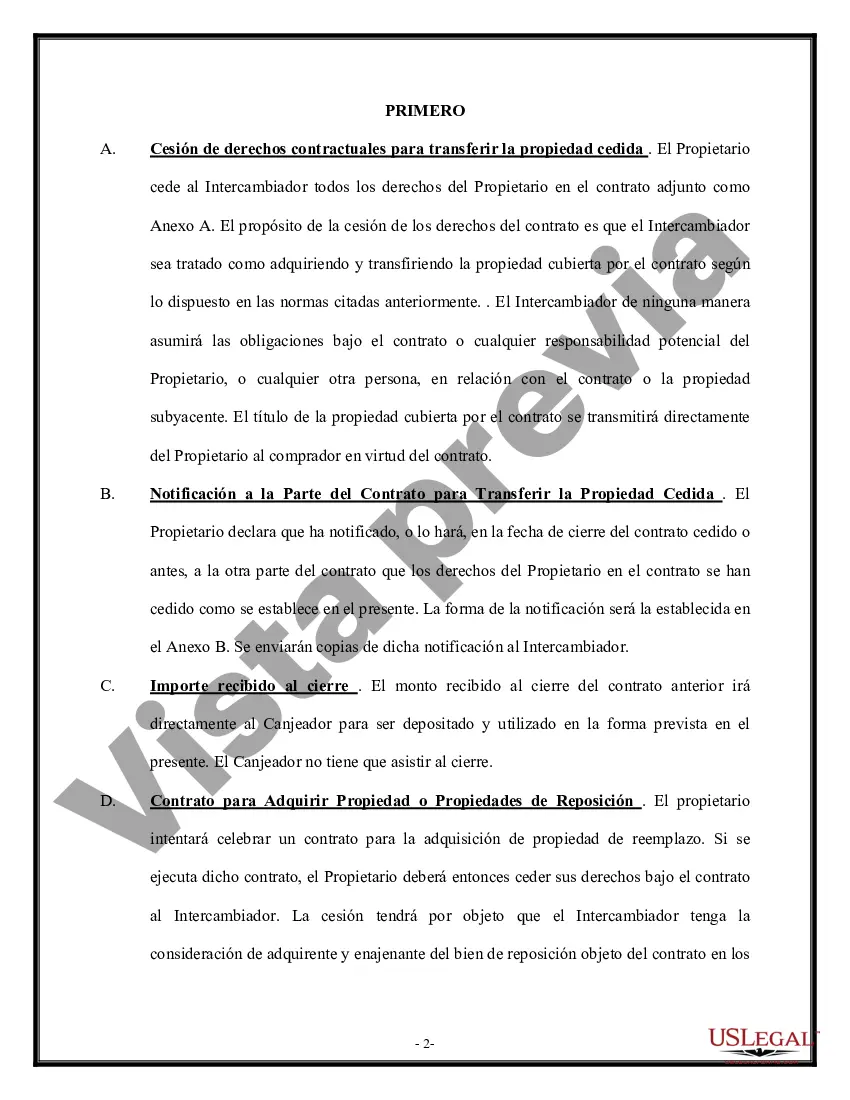

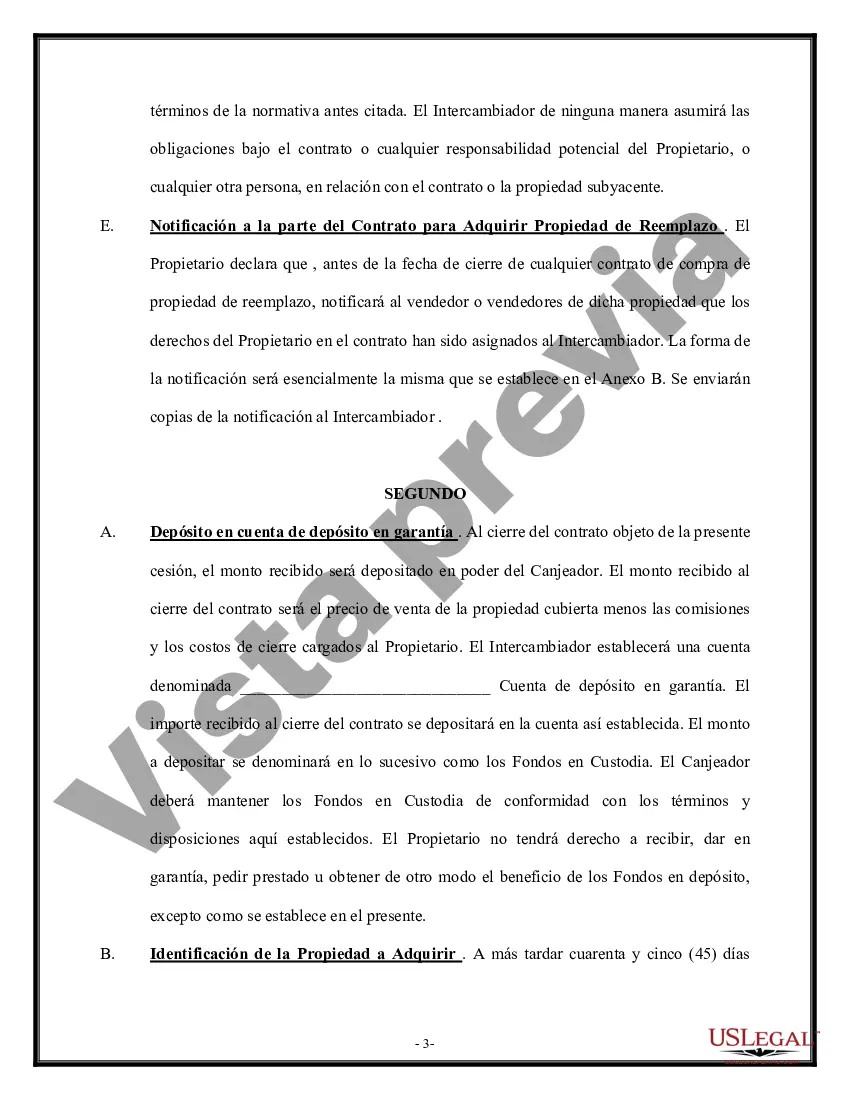

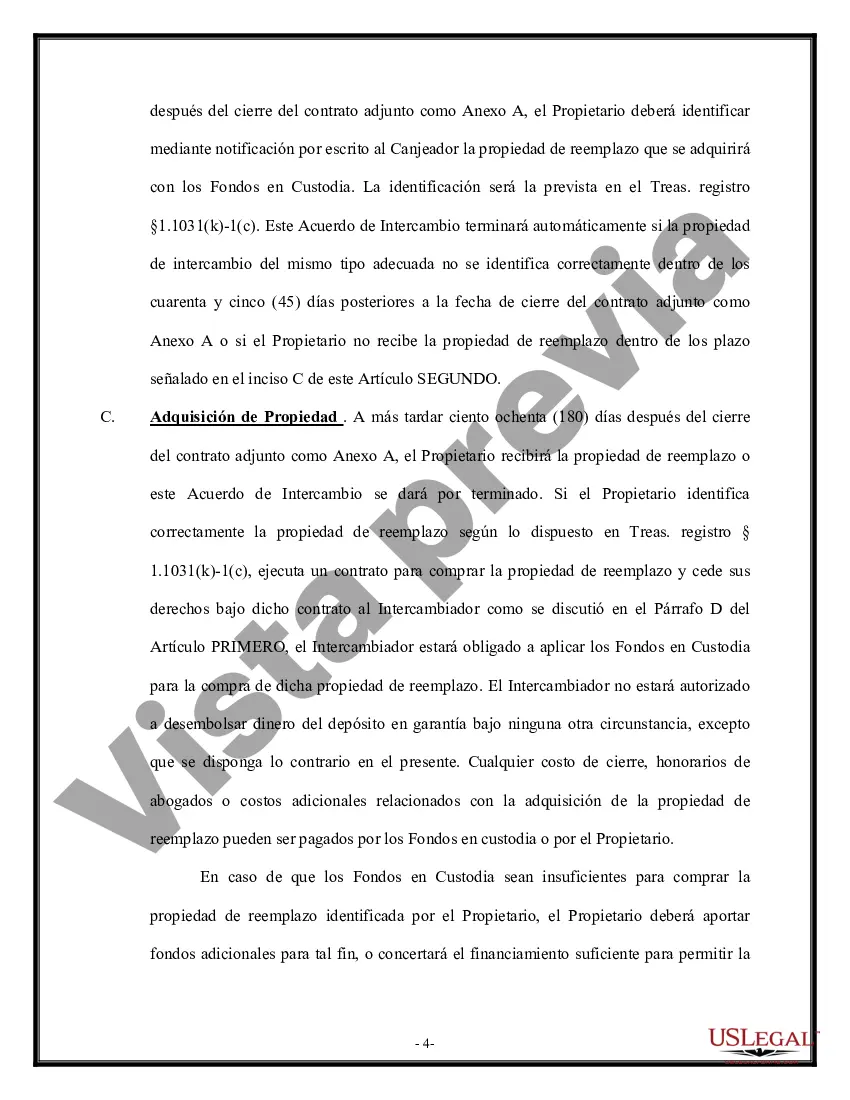

The New Jersey Tax Free Exchange Agreement, also known as Section 1031, is a provision in the state tax law that allows taxpayers to defer the payment of capital gains taxes on certain real property transactions. This beneficial agreement is designed to encourage and stimulate investment in the state's real estate market. Under the New Jersey Tax Free Exchange Agreement Section 1031, individuals or businesses who sell appreciated property can reinvest the proceeds into qualifying replacement properties, without incurring immediate tax liabilities. By doing so, taxpayers can effectively defer capital gains taxes that would otherwise be due upon the sale of the original property. One of the key benefits of the New Jersey Tax Free Exchange Agreement Section 1031 is the ability to defer taxes while facilitating portfolio diversification and consolidation. This allows taxpayers to divest their interests from low-performing or high-maintenance properties and redirect their investments into more lucrative or less demanding real estate assets. To meet the criteria for a tax-free exchange under Section 1031, the properties involved must be held for productive use in a trade or business or for investment purposes. Additionally, both the relinquished property (the property being sold) and the replacement property must be of like-kind, meaning they must be of the same nature, character, or class. However, the term "like-kind" is rather broad in the context of real estate, allowing for considerable flexibility in selecting replacement properties. It's worth noting that the New Jersey Tax Free Exchange Agreement Section 1031 applies solely to the deferment of capital gains taxes at the state level. Taxpayers must still consider the federal tax implications of a 1031 exchange, as federal rules might differ from those of the state. Different types of New Jersey Tax Free Exchange Agreement Section 1031 include: 1. Simultaneous Exchange: This type of exchange occurs when the relinquished property is sold, and the replacement property is acquired on the same day. Both transactions are completed simultaneously, ensuring a seamless transition of properties. 2. Delayed Exchange: In a delayed exchange, the taxpayer sells the relinquished property before acquiring a replacement property. The taxpayer then has a specific time frame to identify and acquire a suitable replacement property. 3. Reverse Exchange: A reverse exchange involves the acquisition of the replacement property before the sale of the relinquished property. This type of exchange is feasible but requires adherence to certain guidelines and restrictions outlined under Section 1031. 4. Improvement Exchange: An improvement exchange allows the taxpayer to use some proceeds from the sale of the relinquished property to make improvements on the replacement property. This ensures that the replacement property meets the like-kind requirement while enhancing its value. Overall, the New Jersey Tax Free Exchange Agreement Section 1031 is a valuable tool for taxpayers looking to defer capital gains taxes, promote property investment, and ultimately optimize their real estate portfolio. It offers flexibility in property selection, diversifies investments, and stimulates economic growth in the state.

Para su conveniencia, debajo del texto en español le brindamos la versión completa de este formulario en inglés. For your convenience, the complete English version of this form is attached below the Spanish version.New Jersey Acuerdo de Intercambio Libre de Impuestos Sección 1031 - Tax Free Exchange Agreement Section 1031

Description

How to fill out New Jersey Acuerdo De Intercambio Libre De Impuestos Sección 1031?

US Legal Forms - one of the most significant libraries of lawful varieties in America - provides an array of lawful file layouts you may down load or produce. Utilizing the website, you can get a huge number of varieties for business and personal uses, sorted by categories, states, or keywords.You will discover the newest versions of varieties much like the New Jersey Tax Free Exchange Agreement Section 1031 in seconds.

If you already possess a registration, log in and down load New Jersey Tax Free Exchange Agreement Section 1031 from the US Legal Forms collection. The Acquire switch will appear on each type you view. You gain access to all previously downloaded varieties in the My Forms tab of your respective profile.

If you wish to use US Legal Forms the very first time, listed here are simple instructions to help you started:

- Ensure you have chosen the best type for your metropolis/county. Click on the Preview switch to analyze the form`s information. Look at the type description to ensure that you have selected the proper type.

- If the type doesn`t match your requirements, take advantage of the Look for area on top of the display to obtain the one which does.

- In case you are happy with the form, verify your decision by simply clicking the Get now switch. Then, opt for the rates prepare you prefer and give your references to sign up for an profile.

- Procedure the transaction. Use your charge card or PayPal profile to perform the transaction.

- Find the format and down load the form in your gadget.

- Make modifications. Fill out, change and produce and sign the downloaded New Jersey Tax Free Exchange Agreement Section 1031.

Every single web template you put into your account lacks an expiry day and is your own property permanently. So, if you want to down load or produce one more backup, just go to the My Forms segment and click on in the type you require.

Get access to the New Jersey Tax Free Exchange Agreement Section 1031 with US Legal Forms, one of the most substantial collection of lawful file layouts. Use a huge number of professional and condition-particular layouts that fulfill your business or personal requirements and requirements.