This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

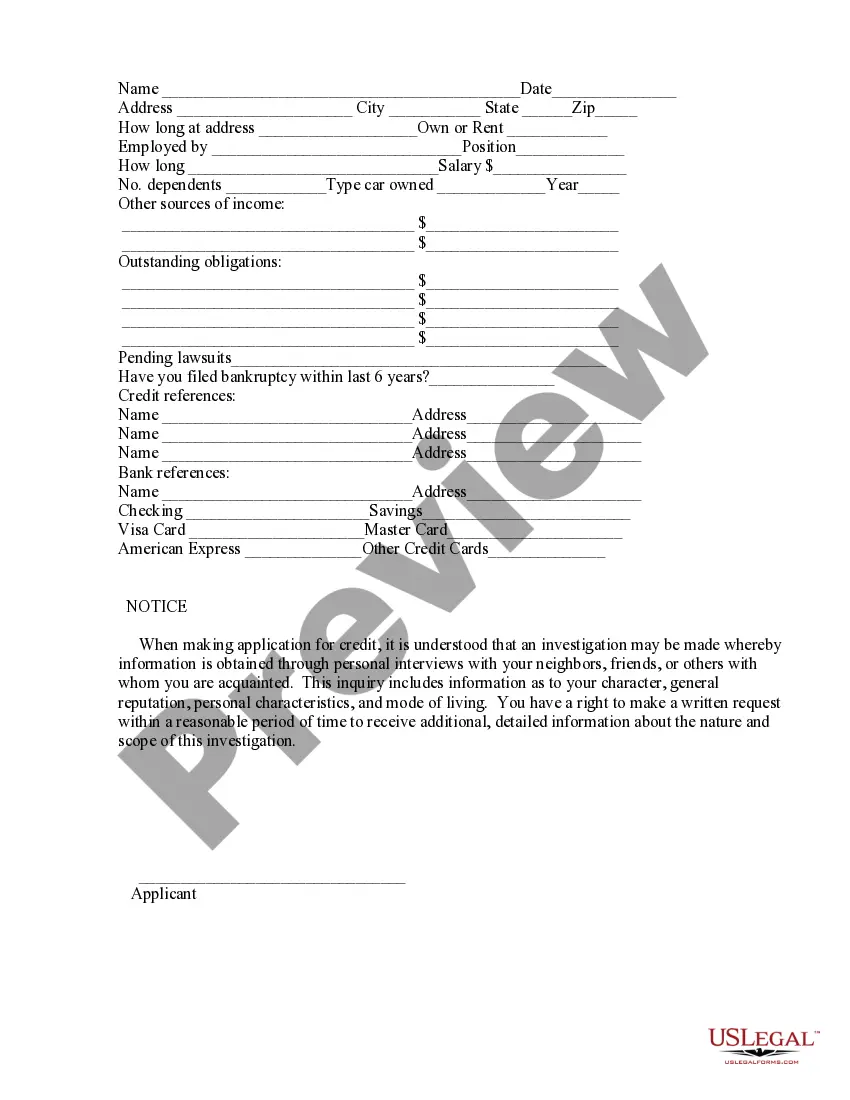

New Jersey Credit Inquiry

Category:

State:

Multi-State

Control #:

US-135-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Credit Inquiry?

You can allocate time on the web looking for the sanctioned document template that meets the federal and state requirements you need.

US Legal Forms provides numerous legal forms that are reviewed by experts.

It is easy to obtain or print the New Jersey Credit Inquiry from our service.

First, ensure that you have selected the correct document template for the region/area of your choice. Review the form description to confirm that you have chosen the right form. If available, use the Preview option to view the document template as well.

- If you already have a US Legal Forms account, you can Log In and select the Download option.

- Afterward, you can fill out, modify, print, or sign the New Jersey Credit Inquiry.

- Every legal document template you receive is yours permanently.

- To get an additional copy of any obtained form, go to the My documents tab and click on the appropriate option.

- If you are using the US Legal Forms website for the first time, follow the straightforward instructions provided below.

Form popularity

FAQ

If you find an unauthorized or inaccurate hard inquiry, you can file a dispute letter and request that the bureau remove it from your report. The consumer credit bureaus must investigate dispute requests unless they determine your dispute is frivolous. Still, not all disputes are accepted after investigation.

No, requesting your credit report will not hurt your credit score. Checking your own credit report is not an inquiry about new credit, so it has no effect on your score.

Credit inquiries are requests lenders make to check your credit when you apply for something like a loan or a mortgage. Hard credit inquiries will show up on your credit report for three years, after which they will disappear if your report has more than five inquiries.

According to FICO, a hard inquiry from a lender will decrease your credit score five points or less. If you have a strong credit history and no other credit issues, you may find that your scores drop even less than that. The drop is temporary.

Though prospective employers don't see your credit score in a credit check, they do see your open lines of credit (such as mortgages), outstanding balances, auto or student loans, foreclosures, late or missed payments, any bankruptcies and collection accounts.

Can I get my credit score for free too? Free credit reports provided by the nationwide credit reporting agencies currently do not include free credit scores. However, your credit card company may provide a free score.

No, requesting your credit report will not hurt your credit score. Checking your own credit report is not an inquiry about new credit, so it has no effect on your score.

All new auto or mortgage loan or utility inquiries will show on your credit report; however, only one of the inquiries within a specified window of time will impact your credit score. This exception generally does not apply to other types of loans, such as credit cards.

According to FICO, a hard inquiry from a lender will decrease your credit score five points or less. If you have a strong credit history and no other credit issues, you may find that your scores drop even less than that.

This information is reported to Equifax by your lenders and creditors and includes the types of accounts (for example, a credit card, mortgage, student loan, or vehicle loan), the date those accounts were opened, your credit limit or loan amount, account balances, and your payment history.